Exam 17: Audit Sampling for Tests of Details and Balances

Exam 1: The Demand for Audit and Other Assurance Services47 Questions

Exam 2: The CPA Profession67 Questions

Exam 3: Audit Reports139 Questions

Exam 4: Professional Ethics114 Questions

Exam 5: Legal Liability113 Questions

Exam 6: The CPA Profession114 Questions

Exam 7: Audit Evidence94 Questions

Exam 8: Audit Planning and Analytical Procedures95 Questions

Exam 9: Materiality and Risk102 Questions

Exam 10: Section 404 Audits of Internal Control and Control Risk116 Questions

Exam 11: Fraud Auditing83 Questions

Exam 12: The Impact of Information Technology on the Audit Process106 Questions

Exam 13: Overall Audit Plan and Audit Program94 Questions

Exam 14: Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions108 Questions

Exam 15: Audit Sampling for Tests of Controls and Substantive Tests of Transactions117 Questions

Exam 16: Completing the Tests in the Sales and Collection Cycle: Accounts Receivable96 Questions

Exam 17: Audit Sampling for Tests of Details and Balances114 Questions

Exam 18: Audit of the Acquisition and Payment Cycle: Tests of Controls and Substantive Tests of Transactions, and Accounts Payable114 Questions

Exam 19: Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts101 Questions

Exam 20: Audit of the Payroll and Personnel Cycle113 Questions

Exam 21: Audit of the Inventory and Warehousing Cycle115 Questions

Exam 22: Audit of the Capital Acquisition and Repayment Cycle91 Questions

Exam 23: Audit of Cash Balances92 Questions

Exam 24: Completing the Audit116 Questions

Exam 25: Other Assurance Services100 Questions

Exam 26: Internal and Governmental Financial Auditing and Operational Auditing73 Questions

Select questions type

If an auditor concludes that internal controls are likely to be effective, the preliminary assessment of control risk can be reduced, leading to which of the following impacts on the acceptable risk of incorrect acceptance?

(Multiple Choice)

4.8/5  (34)

(34)

If an auditor desires a greater level of assurance in auditing a balance, the acceptable risk of incorrect acceptance:

(Multiple Choice)

4.8/5 (42)

The most important difference among tests of controls, substantive tests of transactions, and tests of details of balances lies in what the auditor wants to measure. Explain what each type of test attempts to measure.

(Essay)

4.9/5 (39)

The auditor is concerned with the audited value rather than the error amount of each item in the sample when using:

(Multiple Choice)

4.8/5 (36)

The statistical results when Monetary-Unit Sampling (MUS) is used are called exception bounds.

(True/False)

4.7/5 (34)

Your audit sampling program states: the upper misstatement limit is $13,200 and the risk of incorrect acceptance is at the 95% confidence level. This means:

(Multiple Choice)

4.9/5 (34)

In monetary-unit sampling, the relationship between tolerable misstatement size and required sample size is:

(Multiple Choice)

4.9/5 (45)

Discuss the advantages and disadvantages of monetary-unit sampling over other sampling methods.

(Essay)

4.9/5 (34)

The purpose of stratification is to permit auditors to emphasize certain aspects of a population and deemphasize others.

(True/False)

4.7/5 (40)

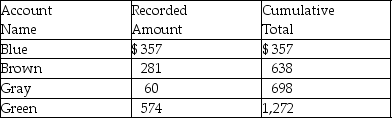

An accounts receivable population contains a total of four customers. The accounts, the amounts, and the cumulative total are shown below. Monetary-unit sampling is to be used.

Based on the information above, the population size is:

Based on the information above, the population size is:

(Multiple Choice)

4.8/5 (38)

The nine steps in planning the sample are almost identical for nonstatistical sampling and difference estimation. However, there are three important differences. Discuss each of the three differences.

(Essay)

4.9/5 (26)

Stratified sampling is applicable to difference, mean-per-unit, and ratio estimation, but it is most commonly used with:

(Multiple Choice)

4.8/5 (35)

The acceptable risk of incorrect acceptance is most related to:

(Multiple Choice)

4.9/5 (31)

The client's trial balance has a balance of $410,000 for merchandise inventory. As the auditor you are willing to accept a balance that is within $20,000 of either side of the recorded balance. You compute a 95% confidence interval of $395,000 to $425,000. You could therefore:

(Multiple Choice)

4.9/5 (49)

The final step in the evaluation of the audit results is the decision to:

(Multiple Choice)

5.0/5 (39)

As the amount of misstatements expected in the population approaches tolerable misstatement, the planned sample size will:

(Multiple Choice)

4.7/5 (36)

The confidence limits in variables sampling are similar to the monetary-unit sampling's:

(Multiple Choice)

4.8/5 (42)

The word below that best explains the relationship between required sample size and the acceptable risk of incorrect acceptance is:

(Multiple Choice)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)