Exam 17: Audit Sampling for Tests of Details and Balances

Exam 1: The Demand for Audit and Other Assurance Services47 Questions

Exam 2: The CPA Profession67 Questions

Exam 3: Audit Reports139 Questions

Exam 4: Professional Ethics114 Questions

Exam 5: Legal Liability113 Questions

Exam 6: The CPA Profession114 Questions

Exam 7: Audit Evidence94 Questions

Exam 8: Audit Planning and Analytical Procedures95 Questions

Exam 9: Materiality and Risk102 Questions

Exam 10: Section 404 Audits of Internal Control and Control Risk116 Questions

Exam 11: Fraud Auditing83 Questions

Exam 12: The Impact of Information Technology on the Audit Process106 Questions

Exam 13: Overall Audit Plan and Audit Program94 Questions

Exam 14: Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions108 Questions

Exam 15: Audit Sampling for Tests of Controls and Substantive Tests of Transactions117 Questions

Exam 16: Completing the Tests in the Sales and Collection Cycle: Accounts Receivable96 Questions

Exam 17: Audit Sampling for Tests of Details and Balances114 Questions

Exam 18: Audit of the Acquisition and Payment Cycle: Tests of Controls and Substantive Tests of Transactions, and Accounts Payable114 Questions

Exam 19: Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts101 Questions

Exam 20: Audit of the Payroll and Personnel Cycle113 Questions

Exam 21: Audit of the Inventory and Warehousing Cycle115 Questions

Exam 22: Audit of the Capital Acquisition and Repayment Cycle91 Questions

Exam 23: Audit of Cash Balances92 Questions

Exam 24: Completing the Audit116 Questions

Exam 25: Other Assurance Services100 Questions

Exam 26: Internal and Governmental Financial Auditing and Operational Auditing73 Questions

Select questions type

What is the primary objective of using stratified sampling in auditing?

(Multiple Choice)

4.8/5  (43)

(43)

Tests for rates of occurrence are appropriately used in all but which of the following situations?

(Multiple Choice)

4.8/5 (31)

Based on the information presented above, you are to indicate for the specified case from the table the required sample size to be selected from population 1 relative to the sample from population 2. In case 1, the required sample from population 1 is:

(Multiple Choice)

4.9/5 (36)

In the application of statistical techniques to the estimation of dollar amounts, a preliminary sample is usually taken primarily for the purpose of estimating the population:

(Multiple Choice)

4.9/5 (36)

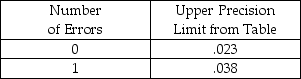

The auditor must deal with layers of the computed upper deviation rate from the attributes table because there are different error assumptions for each error. Assume a sample of 100 had found one error, and the computed upper deviation rate is shown in the following table:

The precision limit for the layer with one error is:

The precision limit for the layer with one error is:

(Multiple Choice)

4.7/5 (38)

Acceptable risk of incorrect acceptance (ARIA) is directly related to the computed precision interval in difference estimation; that is, as ARIA increases, the computed precision interval decreases.

(True/False)

4.8/5 (32)

While performing a substantive test of details during an audit, the auditor determined that the sample results supported the conclusion that the recorded account balance was materially misstated. Which of the following is the least likely auditor reaction to this discovery?

(Multiple Choice)

4.9/5 (28)

When using monetary-unit sampling, evaluating the likelihood of unrecorded items in the population is:

(Multiple Choice)

4.8/5 (29)

Acceptable risk of incorrect acceptance (ARIA) and sample size are inversely related; that is, as ARIA increases, sample size decreases.

(True/False)

4.8/5 (42)

Using statistical sampling to assist in verifying the year-end accounts payable balance, an auditor has accumulated the following data:

Projecting the misstatement to the population, the auditor's estimate of year-end accounts payable balance would be:

Projecting the misstatement to the population, the auditor's estimate of year-end accounts payable balance would be:

(Multiple Choice)

4.9/5 (36)

When using nonstatistical sampling, the larger the sample size, the greater the auditor's confidence that the point estimate is close to the true population value.

(True/False)

4.9/5 (33)

If acceptable audit risk is increased, acceptable risk of incorrect acceptance should be:

(Multiple Choice)

4.8/5 (48)

Identify each of the seven factors that influence sample size for nonstatistical tests of details of balances, and state whether each factor is directly or inversely related to sample size.

(Essay)

4.9/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)