Exam 20: Forming and Operating Partnerships

Exam 1: An Introduction to Tax110 Questions

Exam 2: Tax Compliance, the Irs, and Tax Authorities111 Questions

Exam 3: Tax Planning Strategies and Related Limitations115 Questions

Exam 4: Individual Income Tax Overview, Exemptions, and Filing Status126 Questions

Exam 5: Gross Income and Exclusions131 Questions

Exam 6: Individual Deductions114 Questions

Exam 7: Investments76 Questions

Exam 8: Individual Income Tax Computation and Tax Credits157 Questions

Exam 9: Business Income, Deductions, and Accounting Methods99 Questions

Exam 10: Property Acquisition and Cost Recovery107 Questions

Exam 11: Property Dispositions110 Questions

Exam 12: Compensation102 Questions

Exam 13: Retirement Savings and Deferred Compensation115 Questions

Exam 14: Tax Consequences of Home Ownership112 Questions

Exam 15: Entities Overview70 Questions

Exam 16: Corporate Operations138 Questions

Exam 17: Accounting for Income Taxes100 Questions

Exam 18: Corporate Taxation: Nonliquidating Distributions100 Questions

Exam 19: Corporate Formation, Reorganization, and Liquidation100 Questions

Exam 20: Forming and Operating Partnerships100 Questions

Exam 21: Dispositions of Partnership Interests and Partnership Distributions100 Questions

Exam 22: S Corporations134 Questions

Exam 23: State and Local Taxes117 Questions

Exam 24: The Us Taxation of Multinational Transactions100 Questions

Exam 25: Transfer Taxes and Wealth Planning123 Questions

Select questions type

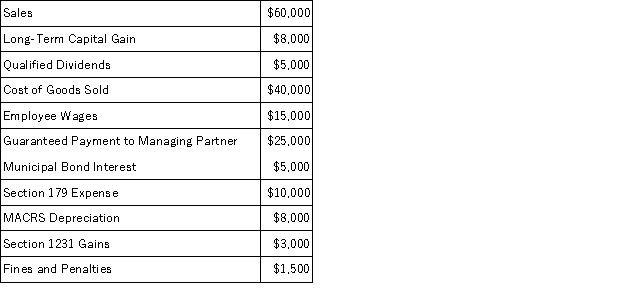

Illuminating Light Partnership had the following revenues, expenses, gains, losses, and distributions:  Given these items, what is Illuminating Light's ordinary business income (loss) for the year?

Given these items, what is Illuminating Light's ordinary business income (loss) for the year?

(Short Answer)

4.9/5  (41)

(41)

A partnership may use the cash method despite having a corporate partner when the partnership's average gross receipts for the prior three taxable years don't exceed _________.

(Multiple Choice)

4.8/5 (34)

Which requirement must be satisfied in order to specially allocate partnership income or losses to partners?

(Multiple Choice)

4.8/5 (31)

Zinc, LP was formed on August 1, 20X9. When the partnership was formed, Al contributed $10,000 in cash and inventory with a FMV and tax basis of $40,000. In addition, Bill contributed equipment with a FMV of $30,000 and adjusted basis of $25,000 along with accounts receivable with a FMV and tax basis of $20,000. Also, Chad contributed land with a FMV of $50,000 and tax basis of $35,000. Finally, Dave contributed a machine, secured by $35,000 of debt, with a FMV of $15,000 and a tax basis of $10,000. What is the total inside basis of all the assets contributed to Zinc, LP?

(Multiple Choice)

4.8/5 (32)

Partnerships can use special allocations to shift built-in gains and built-in losses on contributed property from a partner who contributed the property to other partners.

(True/False)

4.9/5 (39)

Which of the following items are subject to the Net Investment Income tax when an individual partner is a material participant in the partnership?

(Multiple Choice)

4.8/5 (39)

On March 15, 20X9, Troy, Peter, and Sarah formed Picture Perfect General Partnership. This partnership was created to sell a variety of cameras, picture frames, and other photography accessories. The following items were contributed by each partner in exchange for a 1/3 capital and profits interest:

• Troy - cash of $3,000, inventory with a FMV and tax basis $5,000, and a building with a FMV of $8,000 and adjusted basis of $10,000. Additionally, the building is secured by a $10,000 mortgage.

• Peter - cash of $5,000, accounts payable with a FMV and tax basis of $19,000, and land with a FMV and tax basis of $20,000.

• Sarah - cash of $2,000, accounts receivable with a FMV and tax basis of $1,000, and equipment with a FMV of $26,000 and adjusted basis of 4,000. Also, the equipment is secured by a $23,000 note payable.

What is the partnership's inside basis in each asset? How much gain or loss must Picture Perfect recognize? Prepare Picture Perfect's balance sheet reflecting the partners' capital accounts on both a tax basis and 704(b)/FMV basis.

(Essay)

4.8/5 (40)

What is the rationale for the specific rules partnerships must follow in determining a partnership's taxable year-end?

(Multiple Choice)

4.8/5 (43)

For partnership tax years ending after December 31, 2015, when must a partnership file its return?

(Multiple Choice)

4.8/5 (36)

The term "outside basis" refers to the partnership's basis in its assets; whereas, the term "inside basis" refers an individual partner's basis in her partnership interest.

(True/False)

4.8/5 (36)

Peter, Matt, Priscilla, and Mary began the year in the PMPM General Partnership sharing profits, losses, and capital equally. They each had a tax basis at the beginning of the year of $3,000, $10,000, $8,000, and $11,000 respectively. Early in the year, Mary provided general consulting services to the partnership and received an additional 15 percent profits, losses, and capital interest in the partnership. The liquidation value of her additional interest was $45,000. Later the same year, the partnership received cash contributions of $25,000 from Peter and Matt that it used to repay the partnership's $35,000 recourse debt. According to state law, the partners shared responsibility for this debt in accordance with their loss sharing ratios. What is each partner's tax basis after adjustment for these transactions?

(Essay)

4.7/5 (40)

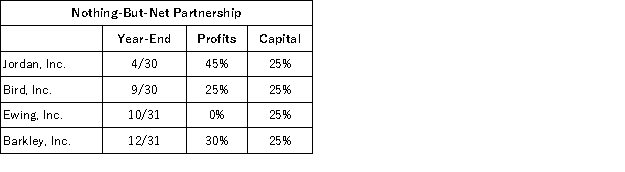

Jordan, Inc., Bird, Inc., Ewing, Inc., and Barkley, Inc. formed Nothing-But-Net Partnership on June 1st, 20X9. Now, Nothing-But-Net must adopt its required tax year-end. The partners' year-ends, profits interests, and capital interests are reflected in the table below. Given this information, what tax year-end must Nothing-But-Net use and what rule requires this year-end?

(Essay)

4.8/5 (30)

If partnership debt is reduced and a partner is deemed to receive a cash distribution, what impact does the deemed distribution have on the partner if it is in excess of her tax basis?

(Multiple Choice)

4.8/5 (35)

What general accounting methods may be used by a partnership and how and by whom are they selected?

(Essay)

4.9/5 (35)

In each of the independent scenarios below, how does the partner or partnership determine its holding period in the property received?

a. A partner contributes property in exchange for a partnership interest

b. The partnership receives contributed property

c. A partner contributes services in exchange for a partnership interest

d. A partner purchases a partnership interest from an existing partner

(Essay)

4.9/5 (41)

Jerry, a partner with 30% capital and profit interest, received his Schedule K-1 from Plush Pillows, LP. At the beginning of the year, Jerry's tax basis in his partnership interest was $50,000. His current year Schedule K-1 reported an ordinary loss of $15,000, long-term capital gain of $3,000, qualified dividends of $2,000, $500 of non-deductible expenses, a $10,000 cash contribution, and a reduction of $4,000 in his share of partnership debt. What is Jerry's adjusted basis in his partnership interest at the end of the year?

(Multiple Choice)

4.9/5 (35)

Which of the following statements regarding capital and profit interests received for services contributed to a partnership is false?

(Multiple Choice)

5.0/5 (30)

Which of the following would not be classified as a material participant in an activity?

(Multiple Choice)

4.7/5 (39)

XYZ, LLC has several individual and corporate members. Abe and Joe, individuals with 4/30 year-ends, each have a 23% profits and capital interest. RST, Inc., a corporation with a 6/30 year end, owns a 4% profits and capital interest while DEF, Inc., a corporation with an 8/30 year end, owns a 4.9% profits and capital interest. Finally, thirty other calendar year-end individual partners (each with less than a 2% profits and capital interest) own the remaining 45% of the profits and capital interests in XYZ. What tax year-end should XYZ use and which test or rule requires this year-end?

(Multiple Choice)

4.8/5 (35)

A partnership can elect to amortize organization and startup costs; however, syndication costs are not deductible.

(True/False)

4.8/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)