Exam 23: State and Local Taxes

Exam 1: An Introduction to Tax110 Questions

Exam 2: Tax Compliance, the Irs, and Tax Authorities111 Questions

Exam 3: Tax Planning Strategies and Related Limitations115 Questions

Exam 4: Individual Income Tax Overview, Exemptions, and Filing Status126 Questions

Exam 5: Gross Income and Exclusions131 Questions

Exam 6: Individual Deductions114 Questions

Exam 7: Investments76 Questions

Exam 8: Individual Income Tax Computation and Tax Credits157 Questions

Exam 9: Business Income, Deductions, and Accounting Methods99 Questions

Exam 10: Property Acquisition and Cost Recovery107 Questions

Exam 11: Property Dispositions110 Questions

Exam 12: Compensation102 Questions

Exam 13: Retirement Savings and Deferred Compensation115 Questions

Exam 14: Tax Consequences of Home Ownership112 Questions

Exam 15: Entities Overview70 Questions

Exam 16: Corporate Operations138 Questions

Exam 17: Accounting for Income Taxes100 Questions

Exam 18: Corporate Taxation: Nonliquidating Distributions100 Questions

Exam 19: Corporate Formation, Reorganization, and Liquidation100 Questions

Exam 20: Forming and Operating Partnerships100 Questions

Exam 21: Dispositions of Partnership Interests and Partnership Distributions100 Questions

Exam 22: S Corporations134 Questions

Exam 23: State and Local Taxes117 Questions

Exam 24: The Us Taxation of Multinational Transactions100 Questions

Exam 25: Transfer Taxes and Wealth Planning123 Questions

Select questions type

On which of the following transactions should sales tax be collected?

Free

(Multiple Choice)

4.9/5  (43)

(43)

Correct Answer: Verified

Verified

D

Discuss the steps necessary to determine whether a sales or use tax applies and how the tax is collected.

Free

(Essay)

4.8/5 (40)

Correct Answer:Verified

Determine whether the seller has sales tax nexus. If so, then sales tax will be collected and remitted by the seller. If not, then the buyer must pay the use tax on his or her individual income tax return or the business' sales tax return.

Explanation: See Figure 23-2.

The trade-show rule allows businesses to maintain a sample room for up to four weeks per year.

Free

(True/False)

4.9/5 (35)

Correct Answer:Verified

False

Which of the following businesses is likely to have taxable sales for purposes of sales and use tax?

(Multiple Choice)

4.8/5 (39)

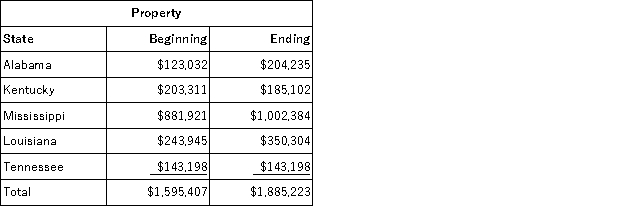

Lefty provides demolition services in several southern states. Lefty has property as follows:  Lefty is a Mississippi Corporation. Lefty also rents property in Mississippi and Tennessee with annual rents of $50,000 and $15,000, respectively. What is Lefty's Mississippi property numerator? (Round your answer to the nearest whole number)

Lefty is a Mississippi Corporation. Lefty also rents property in Mississippi and Tennessee with annual rents of $50,000 and $15,000, respectively. What is Lefty's Mississippi property numerator? (Round your answer to the nearest whole number)

(Multiple Choice)

4.7/5 (32)

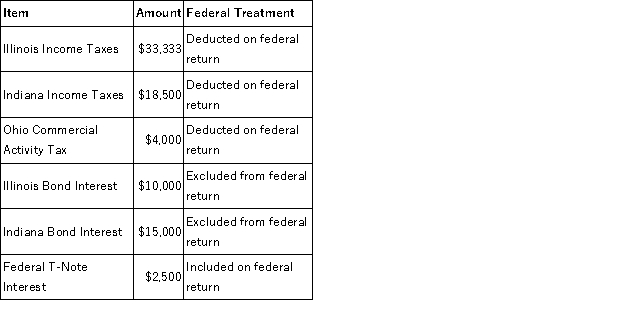

PWD Incorporated is an Illinois corporation. It properly included, deducted, or excluded the following items on its federal tax return in the current year:  PWD's Federal Taxable Income was $100,000. Calculate PWD's Illinois state tax base.

PWD's Federal Taxable Income was $100,000. Calculate PWD's Illinois state tax base.

(Multiple Choice)

4.9/5 (38)

Which of the following sales is always subject to sales and use tax?

(Multiple Choice)

4.8/5 (36)

Separate return states require each member of a consolidated group with nexus to file their own state tax return.

(True/False)

4.8/5 (43)

Assume Tennis Pro attends a sports equipment expo in Washington State. Assume this activity creates nexus of the Business and Occupation (B&O) tax. Assume the tax is .5% of gross receipts for retailers and 1.5% of gross receipts on services. If Tennis Pro has $20,000 of Washington retail sales and $2,000 of services performed, calculate Tennis Pro's B&O tax.

(Short Answer)

4.9/5 (33)

Use tax liability accrues in the state where purchased property will be used when the seller of the property is not required to collect sales tax.

(True/False)

4.8/5 (35)

Tennis Pro has the following sales, payroll and property factors:  What is Tennis Pro's Virginia and Maryland apportionment factors if both states use an equally-weighted three-factor formula?

What is Tennis Pro's Virginia and Maryland apportionment factors if both states use an equally-weighted three-factor formula?

(Short Answer)

4.8/5 (45)

Which of the following is incorrect regarding nondomiciliary businesses?

(Multiple Choice)

4.8/5 (39)

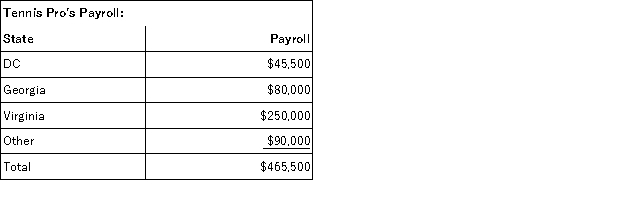

Gordon operates the Tennis Pro Shop in Blacksburg, Virginia. Tennis Pro has payroll as follows:  The other total includes $10,000 of salary of a Virginia employee that works part time in another state. What is Tennis Pro's Virginia payroll numerator and payroll factor?

The other total includes $10,000 of salary of a Virginia employee that works part time in another state. What is Tennis Pro's Virginia payroll numerator and payroll factor?

(Short Answer)

4.8/5 (34)

The state tax base is computed by making adjustments to federal taxable income.

(True/False)

5.0/5 (43)

Federal/state adjustments correct for differences between two states tax laws.

(True/False)

4.9/5 (36)

A state's apportionment formula divides nonbusiness income among the states where nexus exists.

(True/False)

4.8/5 (40)

Which of the following is not a general rule for calculating the property factor?

(Multiple Choice)

4.9/5 (43)

Gordon operates the Tennis Pro Shop in Blacksburg, Virginia. Tennis pro decides to expand into Pennsylvania during the current year and try some new sales techniques. Tennis pro advertises on local radio and television as well as national tennis magazines sent into PA. Salesmen give away promotional materials and occasionally sell demonstration models to local shop employees to build goodwill for Tennis Pro. It holds sales meetings at rented space in local hotels. Personnel occasionally fix minor problems such as tape and strings without charge. One employee performed a credit check for a major account who needed merchandise immediately. Each sales person is allowed an allowance for a car and office equipment to be maintained in an in-home office. Do any of Tennis Pro activities have the potential to create income tax nexus?

(Essay)

5.0/5 (33)

Which of the following regarding the state tax base is incorrect?

(Multiple Choice)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)