Exam 23: State and Local Taxes

Exam 1: An Introduction to Tax110 Questions

Exam 2: Tax Compliance, the Irs, and Tax Authorities111 Questions

Exam 3: Tax Planning Strategies and Related Limitations115 Questions

Exam 4: Individual Income Tax Overview, Exemptions, and Filing Status126 Questions

Exam 5: Gross Income and Exclusions131 Questions

Exam 6: Individual Deductions114 Questions

Exam 7: Investments76 Questions

Exam 8: Individual Income Tax Computation and Tax Credits157 Questions

Exam 9: Business Income, Deductions, and Accounting Methods99 Questions

Exam 10: Property Acquisition and Cost Recovery107 Questions

Exam 11: Property Dispositions110 Questions

Exam 12: Compensation102 Questions

Exam 13: Retirement Savings and Deferred Compensation115 Questions

Exam 14: Tax Consequences of Home Ownership112 Questions

Exam 15: Entities Overview70 Questions

Exam 16: Corporate Operations138 Questions

Exam 17: Accounting for Income Taxes100 Questions

Exam 18: Corporate Taxation: Nonliquidating Distributions100 Questions

Exam 19: Corporate Formation, Reorganization, and Liquidation100 Questions

Exam 20: Forming and Operating Partnerships100 Questions

Exam 21: Dispositions of Partnership Interests and Partnership Distributions100 Questions

Exam 22: S Corporations134 Questions

Exam 23: State and Local Taxes117 Questions

Exam 24: The Us Taxation of Multinational Transactions100 Questions

Exam 25: Transfer Taxes and Wealth Planning123 Questions

Select questions type

All states employ some combination of sales and use tax, income or franchise tax, or property tax to fund their government operations.

(True/False)

4.8/5  (32)

(32)

Which of the following law types is not a primary source type?

(Multiple Choice)

4.8/5 (36)

Tennis Pro, a Virginia Corporation domiciled in Virginia, has the following items of income: $5,000 of dividend income, $15,000 of interest income, $10,000 of rental income from Georgia property, $30,000 of royalty income for an intangible used in Maryland (where nexus exists). Determine how much income is allocated to Virginia.

(Short Answer)

4.7/5 (43)

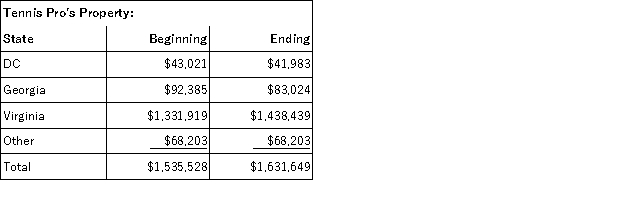

Gordon operates the Tennis Pro Shop in Blacksburg, Virginia. Tennis Pro has property as follows:  What is Tennis Pro's Virginia property numerator and property factor?

What is Tennis Pro's Virginia property numerator and property factor?

(Short Answer)

4.9/5 (37)

Public Law 86-272 protects only companies selling tangible personal property.

(True/False)

4.8/5 (35)

Bethesda Corporation is unprotected from income tax by Public Law 86-272. Which of the following characteristics creates a problem for Bethesda in states other than Maryland?

(Multiple Choice)

4.7/5 (30)

Public Law 86-272 protects solicitation from income taxation. Which of the following activities exceeds the solicitation threshold?

(Multiple Choice)

4.7/5 (31)

Which of the following is not a general rule for calculating the payroll factor?

(Multiple Choice)

4.8/5 (29)

The throwback rule includes inventory in transit in the numerator of the state from where it was shipped.

(True/False)

4.8/5 (29)

Which of the following isn't a typical federal/state adjustment?

(Multiple Choice)

4.9/5 (34)

Physical presence does not always create sales and use tax nexus.

(True/False)

4.9/5 (38)

Della Corporation is headquartered in Carlisle, Pennsylvania. Della has a Pennsylvania state income tax base of $425,000. Of this amount, $75,000 was nonbusiness income. Della's Pennsylvania apportionment factor is 28.52 percent. The nonbusiness income allocated to Pennsylvania was $61,000. Assuming a Pennsylvania corporate tax rate of 7.75 percent, what is Della's Pennsylvania state tax liability? (Round your answer to the nearest whole number)

(Multiple Choice)

4.9/5 (40)

Failure to collect and remit sales taxes often results in a larger tax liability than failure to pay income taxes.

(True/False)

4.7/5 (28)

Assume Tennis Pro discovered that one salesman has gone into Arkansas once each year of the past 4 years and performed activities creating both sales and use tax nexus and income tax nexus. Assume that Arkansas sales were $25,000 each year. Assume that Arkansas business income would be 200,000 each year and that Tennis Pro's Arkansas apportionment percentage would be 1 percent. Assume there would be no Arkansas nonbusiness income. Assume that Arkansas sales and use tax rate was 6.5 percent and corporate income tax rate was 5 percent. What would Tennis Pro's Arkansas sales and use tax and income tax liability be ignoring any possible penalties and interest?

(Short Answer)

4.8/5 (26)

Businesses must collect sales tax only in states where it has sales and use tax nexus.

(True/False)

4.7/5 (36)

Which of the following is not a primary revenue source for most states?

(Multiple Choice)

4.8/5 (37)

The property factor is generally the average of beginning and ending property values.

(True/False)

4.8/5 (41)

Which of the following is true regarding state and local taxes?

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)