Exam 4: Adjustments, Financial Statements, and the Quality of Earnings

Exam 1: Financial Statements and Business Decisions130 Questions

Exam 2: Investing and Financing Decisions and the Accounting System139 Questions

Exam 3: Operating Decisions and the Accounting System128 Questions

Exam 4: Adjustments, Financial Statements, and the Quality of Earnings138 Questions

Exam 5: Communicating and Interpreting Accounting Information119 Questions

Exam 6: Reporting and Interpreting Sales Revenue, Receivables, and Cash130 Questions

Exam 7: Reporting and Interpreting Cost of Goods Sold and Inventory137 Questions

Exam 8: Reporting and Interpreting Property, Plant, and Equipment; Intangibles; and Natural Resources131 Questions

Exam 9: Reporting and Interpreting Liabilities129 Questions

Exam 10: Reporting and Interpreting Bond Securities128 Questions

Exam 11: Reporting and Interpreting Stockholders Equity133 Questions

Exam 12: Statement of Cash Flows121 Questions

Exam 13: Analyzing Financial Statements125 Questions

Exam 14: PPA: Reporting and Interpreting Investments in Other Corporations115 Questions

Select questions type

Which one of the following accounts would not be closed at the end of the accounting year?

(Multiple Choice)

4.8/5  (33)

(33)

What is the purpose of adjusting entries? Give two examples of accruals and deferrals.

(Essay)

4.7/5 (33)

Bridge Company keeps a small inventory of supplies used for cleaning and maintenance purposes. On January 1, 2016, the inventory of supplies on hand was $2,000. During the year, supplies purchased were debited to the supplies account in the amount of $6,500. On December 31, 2016, the amount of supplies in the storeroom was $1,750. The books are adjusted only at year-end.

Required:

Prepare the adjusting entry required at December 31, 2016.

(Essay)

4.8/5 (37)

A calendar-year reporting company preparing its annual financial statements should use the phrase "At December 31, 2016" in the heading of which of the following?

(Multiple Choice)

4.9/5 (49)

On December 1, 2016, Fleet Company paid $30,000 for three months rent and debited prepaid rent for $30,000; the payment was for rent beginning December 1, 2016.

Required:

Prepare Fleet's adjusting entry required on December 31, 2016.

(Essay)

4.8/5 (38)

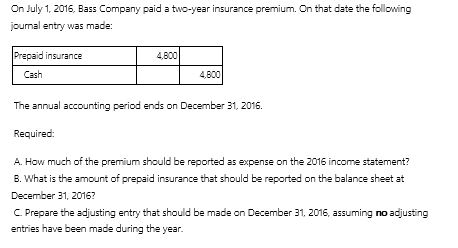

On July 1, 2016, Bass Company paid a two-year insurance premium. On that date the following journal entry was made:

A.How much of the premium should be reported as expense on the 2016 income statement?

B.What is the amount of prepaid insurance that should be reported on the balance sheet at December 31, 2016?

C.Prepare the adjusting entry that should be made on December 31, 2016, assuming no adjusting entries have been made during the year.

A.How much of the premium should be reported as expense on the 2016 income statement?

B.What is the amount of prepaid insurance that should be reported on the balance sheet at December 31, 2016?

C.Prepare the adjusting entry that should be made on December 31, 2016, assuming no adjusting entries have been made during the year.

(Essay)

4.8/5 (42)

Which of the following correctly describes the following adjusting journal entry?

(Multiple Choice)

4.9/5 (36)

Top Company's 2016 sales revenue was $200,000 and 2015 sales revenue was $180,000. Top's total assets as of December 31, 2016 were $150,000 and total assets as of January 1, 2016 were $130,000. What is Top's total asset turnover ratio?

(Multiple Choice)

4.8/5 (33)

Which of the following correctly describes the effects of initially recording deferred revenue when cash is received from a customer?

(Multiple Choice)

4.9/5 (46)

Which of the following journal entries is created as the result of an accrual?

(Multiple Choice)

4.9/5 (37)

The adjusting entry to record accrued revenues results in an increase in assets and an increase in stockholders' equity.

(True/False)

4.8/5 (35)

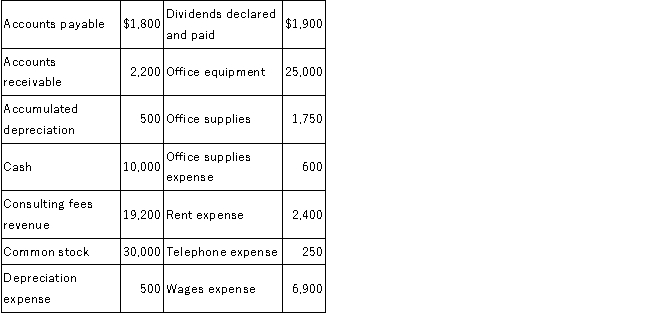

On September 1, 2016, Fast Track, Inc. was started with $30,000 invested by the owners as contributed capital. On September 30, 2016, the accounting records contained the following amounts:  Required:

Prepare a balance sheet for Fast Track, Inc. as of September 30, 2016.

Required:

Prepare a balance sheet for Fast Track, Inc. as of September 30, 2016.

(Essay)

4.9/5 (27)

Income statement accounts are temporary accounts because their balances are closed out at the end of the accounting year.

(True/False)

4.9/5 (32)

On December 31, 2016, the manager of Jordan Creek Apartments noticed that four tenants had not paid their December rent amounting to $500 each. What is the adjusting entry required on December 31, 2016?

(Essay)

4.8/5 (48)

Closing the revenue and gain accounts at year-end requires that these accounts be debited.

(True/False)

4.8/5 (37)

Which of the following adjusting journal entries is created as the result of an accrual?

(Multiple Choice)

4.7/5 (34)

Closing the expense and loss accounts at year-end requires that these accounts be debited.

(True/False)

4.7/5 (36)

On December 31, 2016, Krug Company prepared adjusting entries that included the following items: Depreciation expense: $31,000.

Accrued sales revenue: $29,000.

Accrued expenses: $12,000.

Used insurance: $9,000; the insurance was initially recorded as prepaid.

Rent revenue earned: $7,000; the rent was initially prepaid by the tenant and credited to unearned rent revenue.

If Krug Company reported pretax income of $120,000 prior to the adjusting entries, how much is Krug's pretax income after the adjusting entries?

(Multiple Choice)

4.9/5 (38)

Deferred expenses are initially recorded as assets and when they are later used, expenses will increase and assets will decrease.

(True/False)

4.7/5 (26)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)