Exam 7: Intercompany Transfers of Services and Noncurrent Assets

Exam 1: Intercorporate Acquisitions and Investments in Other Entities47 Questions

Exam 2: Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No Differential39 Questions

Exam 3: The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries With No Differential39 Questions

Exam 4: Consolidation of Wholly Owned Subsidiaries Acquired at More Than Book Value47 Questions

Exam 5: Consolidation of Less-Than-Wholly-Owned Subsidiaries Acquired at More Than Book Value41 Questions

Exam 6: Intercompany Inventory Transactions51 Questions

Exam 7: Intercompany Transfers of Services and Noncurrent Assets46 Questions

Exam 8: Multinational Accounting: Foreign Currency Transactions and Financial Instruments56 Questions

Exam 9: Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements60 Questions

Exam 10: Partnerships: Formation, Operation, and Changes in Membership56 Questions

Exam 11: Partnerships: Liquidation49 Questions

Exam 12: Governmental Entities: Introduction and General Fund Accounting69 Questions

Exam 13: Governmental Entities: Special Funds and Government-Wide Financial Statements68 Questions

Select questions type

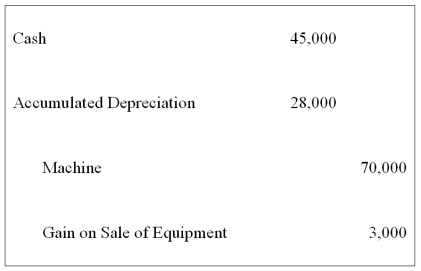

On January 1, 20X7, Servant Company purchased a machine with an expected economic life of five years. On January 1, 20X9, Servant sold the machine to Master Corporation and recorded the following entry:  Master Corporation holds 75 percent of Servant's voting shares. Servant reported net income of $50,000, and Master reported income from its own operations of $100,000 for 20X9. There is no change in the estimated economic life of the equipment as a result of the intercorporate transfer.

-Based on the preceding information, consolidated net income for 20X9 will be:

Master Corporation holds 75 percent of Servant's voting shares. Servant reported net income of $50,000, and Master reported income from its own operations of $100,000 for 20X9. There is no change in the estimated economic life of the equipment as a result of the intercorporate transfer.

-Based on the preceding information, consolidated net income for 20X9 will be:

Free

(Multiple Choice)

4.8/5  (43)

(43)

Correct Answer: Verified

Verified

C

A parent and its 80 percent owned subsidiary have made several intercompany sales of noncurrent assets during the past two years. The amount of income assigned to the noncontrolling interest for the second year should include the noncontrolling interest's share of gains:

Free

(Multiple Choice)

4.9/5 (39)

Correct Answer:Verified

C

A parent sold land to its partially owned subsidiary during the year at a loss. The subsidiary continues to hold the land at the end of the year. The amount to be reported as consolidated net income for the year should equal:

Free

(Multiple Choice)

4.7/5 (36)

Correct Answer:Verified

B

Which worksheet eliminating entry will be made on December 31, 20X9, if XYZ Corporation had initially purchased the land for $50,000 and then sold it to ABC on July 15, 20X8, for $70,000?

(Multiple Choice)

4.7/5 (28)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipment on a straight-line basis.

-Based on the preceding information, in the preparation of the 20X9 consolidated income statement, depreciation expense will be:

(Multiple Choice)

4.8/5 (34)

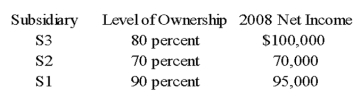

Parent Corporation purchased land from S1 Corporation for $220,000 on December 26, 20X8. This purchase followed a series of transactions between P-controlled subsidiaries. On February 15, 20X8, S3 Corporation purchased the land from a nonaffiliate for $160,000. It sold the land to S2 Company for $145,000 on October 19, 20X8, and S2 sold the land to S1 for $197,000 on November 27, 20X8. Parent has control of the following companies:  Parent reported income from its separate operations of $200,000 for 20X8.

-Based on the preceding information, what amount of gain or loss on sale of land should be reported in the consolidated income statement for 20X8?

Parent reported income from its separate operations of $200,000 for 20X8.

-Based on the preceding information, what amount of gain or loss on sale of land should be reported in the consolidated income statement for 20X8?

(Multiple Choice)

4.9/5 (43)

Blue Company owns 70 percent of Black Company's outstanding common stock. On December 31, 20X8, Black sold equipment to Blue at a price in excess of Black's carrying amount, but less than its original cost. On a consolidated balance sheet at December 31, 20X8, the carrying amount of the equipment should be reported at:

(Multiple Choice)

4.9/5 (28)

Big Corporation receives management consulting services from its 92 percent owned subsidiary, Small Inc. During 20X7, Big paid Small $125,432 for its services. For the year 20X8, Small billed Big $140,000 for such services and collected all but $7,900 by year-end. Small's labor cost and other associated costs for the employees providing services to Big totaled $86,000 in 20X7 and $121,000 in 20X8. Big reported $2,567,000 of income from its own separate operations for 20X8, and Small reported net income of $695,000.

-Based on the preceding information, what amount of receivable/payable should be eliminated in the 20X8 consolidated financial statements?

(Multiple Choice)

5.0/5 (32)

Blue Corporation holds 70 percent of Black Company's voting common stock. On January 1, 20X3, Black paid $500,000 to acquire a building with a 10-year expected economic life. Black uses straight-line depreciation for all depreciable assets. On December 31, 20X8, Blue purchased the building from Black for $180,000. Blue reported income, excluding investment income from Black, of $140,000 and $162,000 for 20X8 and 20X9, respectively. Black reported net income of $30,000 and $45,000 for 20X8 and 20X9, respectively.

-Based on the preceding information, the amount to be reported as consolidated net income for 20X8 will be:

(Multiple Choice)

4.9/5 (36)

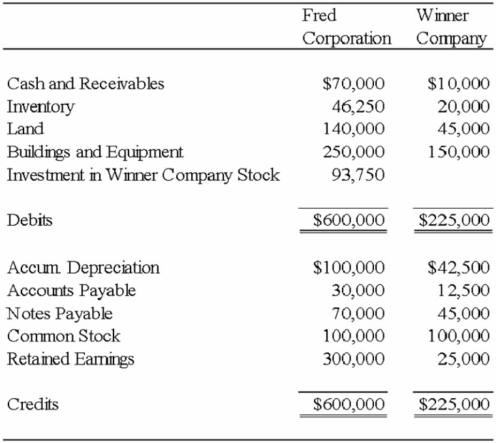

Fred Corporation owns 75 percent of Winner Company's voting shares, acquired on March 21, 20X5, at book value. At that date, the fair value of the noncontrolling interest was equal to 25 percent of the book value of Winner Company.  On January 1, 20X4, Fred paid $150,000 for equipment with a 10-year expected total economic life. The equipment was depreciated on a straight-line basis with no residual value. Winner purchased the equipment from Fred on December 31, 20X6, for $140,000. Winner sold land it had purchased for $75,000 on February 18, 20X4, to Fred for $60,000 on October 10, 20X7.

Required:

Prepare the elimination entries for 20X8 related to the sale of depreciable assets and land.

On January 1, 20X4, Fred paid $150,000 for equipment with a 10-year expected total economic life. The equipment was depreciated on a straight-line basis with no residual value. Winner purchased the equipment from Fred on December 31, 20X6, for $140,000. Winner sold land it had purchased for $75,000 on February 18, 20X4, to Fred for $60,000 on October 10, 20X7.

Required:

Prepare the elimination entries for 20X8 related to the sale of depreciable assets and land.

(Essay)

5.0/5 (32)

Pie Company acquired 75 percent of Strawberry Company's stock at the underlying book value on January 1, 20X8. At that date, the fair value of the noncontrolling interest was equal to 25 percent of the book value of Strawberry Company. Strawberry Company reported shares outstanding of $350,000 and retained earnings of $100,000. During 20X8, Strawberry Company reported net income of $60,000 and paid dividends of $3,000. In 20X9, Strawberry Company reported net income of $90,000 and paid dividends of $15,000. The following transactions occurred between Pie Company and Strawberry Company in 20X8 and 20X9:

Strawberry Co. sold equipment to Pie Co. for a $42,000 gain on December 31, 20X8. Strawberry Co. had originally purchased the equipment for $140,000 and it had a carrying value of $28,000 on December 31, 20X8. At the time of the purchase, Pie Co. estimated that the equipment still had a seven-year remaining useful life.

Pie Co. sold land costing $90,000 to Strawberry Co. on June 28, 20X9, for $110,000.

Required:

Give all eliminating entries needed to prepare a consolidation worksheet for 20X9 assuming that Pie Co. uses the fully adjusted equity method to account for its investment in Strawberry Company.

(Essay)

4.8/5 (41)

On January 1, 20X7, Servant Company purchased a machine with an expected economic life of five years. On January 1, 20X9, Servant sold the machine to Master Corporation and recorded the following entry: Master Corporation holds 75 percent of Servant's voting shares. Servant reported net income of $50,000, and Master reported income from its own operations of $100,000 for 20X9. There is no change in the estimated economic life of the equipment as a result of the intercorporate transfer.

-Based on the preceding information, in the preparation of the 20X9 consolidated income statement, depreciation expense will be:

(Multiple Choice)

4.7/5 (39)

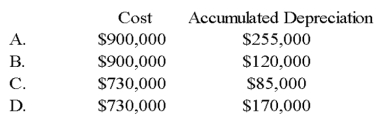

On January 1, 20X9, Light Corporation sold equipment for $400,000 to Star Corporation, its wholly owned subsidiary. Light had paid $900,000 for this equipment, which had accumulated depreciation of $170,000. Light estimated a $50,000 salvage value and depreciated the tractor using the straight-line method over 10 years, a policy that Star continued. In Light's December 31, 20X9, consolidated balance sheet, this tractor should be included in fixed-asset cost and accumulated depreciation as:

(Multiple Choice)

4.9/5 (27)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipments on a straight-line basis.

-Based on the preceding information, in the preparation of the 20X9 consolidated financial statements, equipment will be:

(Multiple Choice)

4.8/5 (34)

Blue Corporation holds 70 percent of Black Company's voting common stock. On January 1, 20X3, Black paid $500,000 to acquire a building with a 10-year expected economic life. Black uses straight-line depreciation for all depreciable assets. On December 31, 20X8, Blue purchased the building from Black for $180,000. Blue reported income, excluding investment income from Black, of $140,000 and $162,000 for 20X8 and 20X9, respectively. Black reported net income of $30,000 and $45,000 for 20X8 and 20X9, respectively.

-Based on the preceding information, the amount of income assigned to the controlling shareholders in the consolidated income statement for 20X8 will be:

(Multiple Choice)

4.8/5 (35)

Parent Corporation purchased land from S1 Corporation for $220,000 on December 26, 20X8. This purchase followed a series of transactions between P-controlled subsidiaries. On February 15, 20X8, S3 Corporation purchased the land from a nonaffiliate for $160,000. It sold the land to S2 Company for $145,000 on October 19, 20X8, and S2 sold the land to S1 for $197,000 on November 27, 20X8. Parent has control of the following companies: Parent reported income from its separate operations of $200,000 for 20X8.

-Based on the preceding information, what should be the amount of income assigned to the controlling shareholders in the consolidated income statement for 20X8?

(Multiple Choice)

4.8/5 (44)

Blue Corporation holds 70 percent of Black Company's voting common stock. On January 1, 20X3, Black paid $500,000 to acquire a building with a 10-year expected economic life. Black uses straight-line depreciation for all depreciable assets. On December 31, 20X8, Blue purchased the building from Black for $180,000. Blue reported income, excluding investment income from Black, of $140,000 and $162,000 for 20X8 and 20X9, respectively. Black reported net income of $30,000 and $45,000 for 20X8 and 20X9, respectively.

-Based on the preceding information, the amount to be reported as consolidated net income for 20X9 will be:

(Multiple Choice)

4.8/5 (32)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipments on a straight-line basis.

-Based on the preceding information, the gain on sale of the equipment recorded by Mortar for 20X8 is:

(Multiple Choice)

4.7/5 (36)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipments on a straight-line basis.

-Based on the preceding information, in the preparation of the 20X8 consolidated financial statements, equipment will be:

(Multiple Choice)

4.8/5 (40)

Parent Company owns 70% of Son Company's outstanding stock. During 20X1 Son Company sold land to Parent Company for a gain of $25,000. Parent company held the land all of 20X1. The gain on the sale to Parent should be:

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)