Exam 5: Modern Portfolio Concepts

Exam 1: The Investment Environment82 Questions

Exam 2: Securities Markets and Transactions113 Questions

Exam 3: Investment Information and Securities Transactions134 Questions

Exam 4: Return and Risk130 Questions

Exam 5: Modern Portfolio Concepts110 Questions

Exam 6: Common Stocks136 Questions

Exam 7: Analyzing Common Stocks128 Questions

Exam 8: Stock Valuation122 Questions

Exam 9: Market Efficiency and Behavioral Finance114 Questions

Exam 10: Fixed-Income Securities128 Questions

Exam 11: Bond Valuation120 Questions

Exam 12: Mutual Funds and Exchange-Traded Funds121 Questions

Exam 13: Managing Your Own Portfolio121 Questions

Exam 14: Options: Puts and Calls128 Questions

Exam 15: Futures Markets and Securities110 Questions

Select questions type

Which of the following represent systematic risks?

I. the president of a company suddenly resigns

II. the economy goes into a recessionary period

III. a company's product is recalled for defects

IV. the Federal Reserve unexpectedly changes interest rates

(Multiple Choice)

4.9/5  (35)

(35)

Coefficients of correlation range from a maximum of +10 to a minimum of -10.

(True/False)

4.9/5 (41)

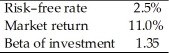

You have gathered the following information concerning a particular investment and conditions in the market.  According to the Capital Asset Pricing Model, the required return for this investment is

According to the Capital Asset Pricing Model, the required return for this investment is

(Multiple Choice)

4.9/5 (31)

By plotting the efficient frontier, investors can find the unique portfolio that is ideal for all investors.

(True/False)

4.9/5 (40)

Standard deviation is a measure that indicates how the price of an individual security responds to market forces.

(True/False)

4.9/5 (41)

In the real world, most of the assets available to investors

(Multiple Choice)

4.9/5 (40)

What is the expected return on a stock with a beta of 1.09, a market risk premium of 8%, and a risk-free rate of 4%?

(Multiple Choice)

4.8/5 (34)

Negatively correlated assets reduce risk more than positively correlated assets.

(True/False)

4.8/5 (28)

A portfolio consisting of four stocks is expected to produce returns of 9%, 11%, 3% and 17%, respectively, over the next four years. What is the standard deviation of these expected returns?

(Multiple Choice)

4.9/5 (41)

Dr. Zweibel's portfolio consists of four stocks: AZMN, 35%, beta 2.4; MKR, 20%, beta 1.6; ABDE, 25%, beta 1.8; and SBUK, 20%, beta 2.1. Compute Dr. Z's portfolio beta. Does he seem to be a conservative or aggressive investor?

(Essay)

4.8/5 (45)

The best stock to own when the stock market is at a peak and is expected to decline in value is one with a beta of

(Multiple Choice)

4.8/5 (32)

The risk of a portfolio consisting of two uncorrelated assets will be

(Multiple Choice)

4.7/5 (42)

For stocks with positive betas, higher risk stocks will have higher beta values.

(True/False)

4.9/5 (46)

Modern portfolio theory does not consider diversifiable risk relevant because

(Multiple Choice)

4.8/5 (44)

Both the efficient frontier and beta are important aspects of MPT.

(True/False)

5.0/5 (38)

Which one of the following will provide the greatest international diversification?

(Multiple Choice)

4.8/5 (37)

Beta is the slope of the best fit line for the points with coordinates representing the ________ and the ________ for each one of several years.

(Multiple Choice)

4.9/5 (46)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)