Exam 9: Forecasting Exchange Rates

Exam 1: Multinational Financial Management: an Overview79 Questions

Exam 2: International Flow of Funds75 Questions

Exam 3: International Financial Markets102 Questions

Exam 4: Exchange Rate Determination74 Questions

Exam 5: Currency Derivatives163 Questions

Exam 6: Government Influence on Exchange Rates117 Questions

Exam 7: International Arbitrage and Interest Rate Parity97 Questions

Exam 8: Relationships Among Inflation, Interest Rates, and Exchange Rates62 Questions

Exam 9: Forecasting Exchange Rates92 Questions

Exam 10: Measuring Exposure to Exchange Rate Fluctuations90 Questions

Exam 11: Managing Transaction Exposure92 Questions

Exam 12: Managing Economic Exposure and Translation Exposure63 Questions

Exam 13: Direct Foreign Investment62 Questions

Exam 14: Multinational Capital Budgeting63 Questions

Exam 15: International Corporate Governance and Control74 Questions

Exam 16: Country Risk Analysis57 Questions

Exam 17: Multinational Cost of Capital and Capital Structure71 Questions

Exam 18: Long-Term Debt Financing54 Questions

Exam 19: Financing International Trade73 Questions

Exam 20: Short-Term Financing55 Questions

Exam 21: International Cash Management49 Questions

Select questions type

When the value from the prior period of an influential factor affects the forecast in the future period, this is an example of a(n):

(Multiple Choice)

4.8/5  (32)

(32)

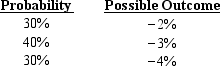

The following regression model was estimated to forecast the value of the Indian rupee (INR): INRt = a0 + a1INTt + a2INFt - 1 + t,

Where INR is the quarterly change in the rupee, INT is the real interest rate differential in period t between the U.S. and India, and INF is the inflation rate differential between the U.S. and India in the previous period. Regression results indicate coefficients of a0 = .003; a1 = -.5; and a2 = .8. Assume that INFt - 1 = 2%. However, the interest rate differential is not known at the beginning of period t and must be estimated. You have developed the following probability distribution:

The expected change in the Indian rupee in period t is:

The expected change in the Indian rupee in period t is:

(Multiple Choice)

4.8/5 (37)

Assume that U.S. interest rates are 6%, while British interest rates are 7%. If the international Fisher effect holds and is used to determine the future spot rate, the forecast would reflect an expectation of:

(Multiple Choice)

4.8/5 (40)

Huge Corporation has just initiated a market-based forecast system using the forward rate as an estimate of the future spot rate of the Japanese yen (¥) and the Australian dollar (A$). Listed below are the forecasted and realized values for the last period:  According to this information and using the absolute forecast error as a percentage of the realized value, the forecast of the yen by Huge Corp. is ____ the forecast of the Australian dollar.

According to this information and using the absolute forecast error as a percentage of the realized value, the forecast of the yen by Huge Corp. is ____ the forecast of the Australian dollar.

(Multiple Choice)

4.8/5 (40)

If the foreign exchange market is ____ efficient, then historical and current exchange rate information is not useful for forecasting exchange rate movements.

(Multiple Choice)

4.9/5 (31)

Research indicates that currency forecasting services almost always outperform forecasts based on the forward rate.

(True/False)

4.9/5 (30)

The following regression model was estimated to forecast the value of the Malaysian ringgit (MYR): MYRt = a0 + a1INCt - 1 + a2INFt - 1 + t,

Where MYR is the quarterly change in the ringgit, INF is the previous quarterly percentage change in the inflation differential, and INC is the previous quarterly percentage change in the income growth differential. Regression results indicate coefficients of a0 = 0.005; a1 = 0.4; and a2 = 0.7. The most recent quarterly percentage change in the inflation differential is -5%, while the most recent quarterly percentage change in the income differential is 3%. Using this information, the forecast for the percentage change in the ringgit is

(Multiple Choice)

4.9/5 (30)

Assume that the U.S. interest rate is 11 percent, while Australia's one-year interest rate is 12 percent. Assume interest rate parity holds. If the one-year forward rate of the Australian dollar was used to forecast the future spot rate, the forecast would reflect an expectation of:

(Multiple Choice)

4.8/5 (26)

If an MNC invests excess cash in a foreign county, it would like the foreign currency to ____; if an MNC issues bonds denominated in a foreign currency, it would like the foreign currency to ____.

(Multiple Choice)

4.9/5 (39)

A forecast of a currency one year in advance is typically more accurate than a forecast one week in advance since the currency reverts to equilibrium over a longer term period.

(True/False)

4.8/5 (37)

If a foreign currency is expected to ____ substantially against the parent's currency, the parent may prefer to ____ the remittance of subsidiary earnings.

(Multiple Choice)

5.0/5 (41)

Which of the following is not a method of forecasting exchange rate volatility?

(Multiple Choice)

4.9/5 (46)

Since the forward rate does not capture the nominal interest rate between two countries, it should provide a less accurate forecast for currencies in high-inflation countries than the spot rate.

(True/False)

4.9/5 (39)

Assume that interest rate parity holds. The U.S. five-year interest rate is 5% annualized, and the Mexican five-year interest rate is 8% annualized. Today's spot rate of the Mexican peso is $.20. What is the approximate five-year forecast of the peso's spot rate if the five-year forward rate is used as a forecast?

(Multiple Choice)

4.8/5 (38)

A regression model was applied to explain movements in the Canadian dollar's value over time. The coefficient for the inflation differential between the U.S. and Canada was -0.2. The coefficient of the interest rate differential between the U.S. and Canada produced a coefficient of 0.8. Thus, the Canadian dollar depreciates when the inflation differential ____ and the interest rate differential ____.

(Multiple Choice)

4.9/5 (35)

If speculators expect the spot rate of the Canadian dollar in 30 days to be ____ than the 30-day forward rate on Canadian dollars, they will ____ Canadian dollars forward and put ____ pressure on the Canadian dollar forward rate.

(Multiple Choice)

4.9/5 (43)

A forecasting technique based on fundamental relationships between economic variables and exchange rates, such as inflation, is referred to as technical forecasting.

(True/False)

4.8/5 (41)

Small Corporation would like to forecast the value of the Cyprus pound (CYP) five years from now using forward rates. Unfortunately, Small is unable to obtain quotes for five-year forward contracts. However, Small observes that the five-year interest rate in the U.S. is 11%, while the Cyprus five-year interest rate is 15%. Based on this information, the Cyprus pound should ____ by ____% over the next five years.

(Multiple Choice)

4.8/5 (34)

If the foreign exchange market is ____ efficient, then technical analysis is not useful in forecasting exchange rate movements.

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)