Exam 3: Principles of Option Pricing

Exam 1: Introduction40 Questions

Exam 2: Structure of Options Markets63 Questions

Exam 3: Principles of Option Pricing56 Questions

Exam 4: Option Pricing Models: the Binomial Model60 Questions

Exam 5: Option Pricing Models: the Black-Scholes-Merton Model60 Questions

Exam 6: Basic Option Strategies60 Questions

Exam 7: Advanced Option Strategies60 Questions

Exam 8: Principles of Pricing Forwards,futures and Options on Futures59 Questions

Exam 9: Futures Arbitrage Strategies59 Questions

Exam 10: Forward and Futures Hedging,spread,and Target Strategies60 Questions

Exam 11: Swaps60 Questions

Exam 12: Interest Rate Forwards and Options60 Questions

Exam 13: Advanced Derivatives and Strategies60 Questions

Exam 14: Financial Risk Management Techniques and Appplications62 Questions

Exam 15: Managing Risk in an Organization58 Questions

Select questions type

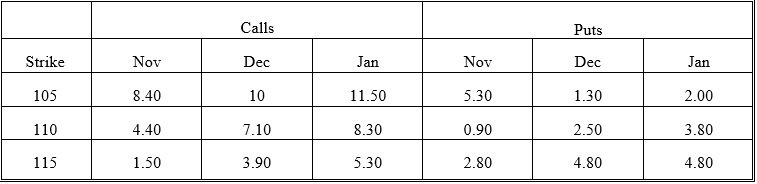

The following quotes were observed for options on a given stock on November 1 of a given year. These are American calls except where indicated. Use the information to answer questions 7 through 20.

The stock price was 113.25. The risk-free rates were 7.30 percent (November), 7.50 percent (December) and 7.62 percent (January). The times to expiration were 0.0384 (November), 0.1342 (December), and 0.211 (January). Assume no dividends unless indicated.

-Suppose the stock is about to go ex-dividend in one day.The dividend will be $4.00.Which of the following calls will you consider for exercise?

The stock price was 113.25. The risk-free rates were 7.30 percent (November), 7.50 percent (December) and 7.62 percent (January). The times to expiration were 0.0384 (November), 0.1342 (December), and 0.211 (January). Assume no dividends unless indicated.

-Suppose the stock is about to go ex-dividend in one day.The dividend will be $4.00.Which of the following calls will you consider for exercise?

(Multiple Choice)

4.9/5  (30)

(30)

The following quotes were observed for options on a given stock on November 1 of a given year. These are American calls except where indicated. Use the information to answer questions 7 through 20.

The stock price was 113.25. The risk-free rates were 7.30 percent (November), 7.50 percent (December) and 7.62 percent (January). The times to expiration were 0.0384 (November), 0.1342 (December), and 0.211 (January). Assume no dividends unless indicated.

-What is the time value of the November 115 put?

(Multiple Choice)

4.8/5 (29)

The put-call parity rule for American options is stated as equalities.

(True/False)

4.8/5 (38)

The following quotes were observed for options on a given stock on November 1 of a given year. These are American calls except where indicated. Use the information to answer questions 7 through 20.

The stock price was 113.25. The risk-free rates were 7.30 percent (November), 7.50 percent (December) and 7.62 percent (January). The times to expiration were 0.0384 (November), 0.1342 (December), and 0.211 (January). Assume no dividends unless indicated.

-What is the time value of the December 105 put?

(Multiple Choice)

5.0/5 (44)

The spread between the prices of two European puts,alike in all respects except exercise price,cannot exceed the difference in their exercise prices.

(True/False)

4.9/5 (36)

Transactions to exploit pricing errors in the put-call parity relationship are called conversions and reversals.

(True/False)

4.9/5 (34)

Which of the following statements about an American call is not true?

(Multiple Choice)

4.8/5 (35)

The following quotes were observed for options on a given stock on November 1 of a given year. These are American calls except where indicated. Use the information to answer questions 7 through 20.

The stock price was 113.25. The risk-free rates were 7.30 percent (November), 7.50 percent (December) and 7.62 percent (January). The times to expiration were 0.0384 (November), 0.1342 (December), and 0.211 (January). Assume no dividends unless indicated.

-From American put-call parity,what are the minimum and maximum values that the sum of the stock price and December 110 put price can be?

(Multiple Choice)

4.8/5 (33)

Holding everything else constant,put options are more expensive in periods of high interest rates.

(True/False)

4.8/5 (45)

A situation in which early exercise of an American put can be justified is

(Multiple Choice)

4.8/5 (34)

The price of a call option is directly related to interest rates.

(True/False)

4.8/5 (36)

The following quotes were observed for options on a given stock on November 1 of a given year. These are American calls except where indicated. Use the information to answer questions 7 through 20.

The stock price was 113.25. The risk-free rates were 7.30 percent (November), 7.50 percent (December) and 7.62 percent (January). The times to expiration were 0.0384 (November), 0.1342 (December), and 0.211 (January). Assume no dividends unless indicated.

-What is the time value of the November 110 call?

(Multiple Choice)

4.8/5 (38)

The difference between a Treasury bill's face value and its price is called the

(Multiple Choice)

4.8/5 (36)

A stock is equivalent to a long call,short put and long risk-free bond.

(True/False)

4.7/5 (51)

An American put might be exercised early even when there are no dividends on the underlying stock.

(True/False)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)