Short Answer

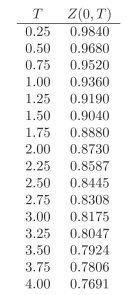

Use the following discount factors when needed.

-Calculate the convexity of the following security: a 5-year zero coupon bond.

Correct Answer:

Verified

The convex...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

The convex...

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Related Questions

Q4: Use the following discount factors when needed.

Q5: Suppose you hold a bond and interest

Q6: If you need three securities to hedge

Q7: Compute the Term Spread and the Butter?y

Q8: Suppose you hold a bond and interest

Q10: Compute the Term Spread and the Butterfly

Q11: Use the following discount factors when needed.

Q12: Use the following discount factors when needed.

Q13: Use the following discount factors when needed.

Q14: You currently hold a 7-year fixed rate