Short Answer

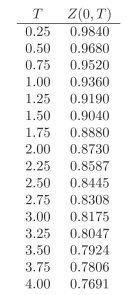

Use the following discount factors when needed.

-Calculate the convexity of the following portfolio:

i. 2 units of a 1.5-year ?xed rate bond paying 6% quarterly.

ii. 4 units of a 1.75-year ?oating rate bond paying ?oat + 80 bps semi- annually. You know that the reference rate was 7% three months ago. 13

iii. 6 units of a 2-year zero coupon bond.

iv. 1 units of a 1.5-year ?oating rate bond with no spread paid semian- nually.

Correct Answer:

Verified

The convex...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q7: Compute the Term Spread and the Butter?y

Q8: Suppose you hold a bond and interest

Q9: Use the following discount factors when needed.

Q10: Compute the Term Spread and the Butterfly

Q11: Use the following discount factors when needed.

Q13: Use the following discount factors when needed.

Q14: You currently hold a 7-year fixed rate

Q15: Compute the Term Spread and the Butterfly

Q16: You currently hold a 2-year fixed rate

Q17: How many securities do you need to