Multiple Choice

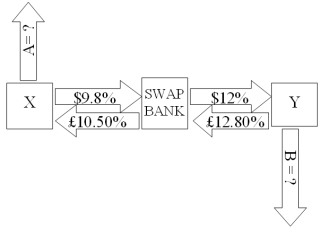

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow £5,000,000 fixed for 5 years.The exchange rate is $2 = £1 and is not expected to change over the next 5 years.Their external borrowing opportunities are:  A swap bank proposes the following interest-only swap: Company X will pay the swap bank annual payments on $10,000,000 at an interest rate of $9.80%; in exchange the swap bank will pay to company X interest payments on £5,000,000 at a fixed rate of 10.5%.Y will pay the swap bank interest payments on £5,000,000 at a fixed rate of 12.80% and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of 12%.

A swap bank proposes the following interest-only swap: Company X will pay the swap bank annual payments on $10,000,000 at an interest rate of $9.80%; in exchange the swap bank will pay to company X interest payments on £5,000,000 at a fixed rate of 10.5%.Y will pay the swap bank interest payments on £5,000,000 at a fixed rate of 12.80% and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of 12%.  If company X takes on the swap,what external actions should they engage in?

If company X takes on the swap,what external actions should they engage in?

A) They should borrow $10,000,000 at $10%

B) They should borrow £5,000,000 at 10.50% interest-only for five years; translate pounds to dollars at the spot rate.

C) They should borrow £5,000,000 at £10.50% interest-only for five years; translate pounds to dollars at the spot rate; enter long position in a forward contract to buy £5,000,000 in five years.

D) None of the above

Correct Answer:

Verified

Correct Answer:

Verified

Q2: What would be the interest rate?

Q2: What would be the interest rate?

Q40: Explain how firm A could use two

Q47: Examples of "single-currency interest rate swap" and

Q51: The term interest rate swap<br>A)refers to a

Q56: FOR YOUR SWAP (the one you have

Q65: Compute the payments due in the second

Q71: A is a U.S.-based MNC with AAA

Q97: Consider a fixed for fixed currency swap.

Q98: In the problem just previous, company X<br>A)is