Multiple Choice

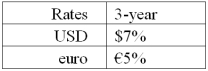

Suppose that you are a swap bank and you notice that interest rates on coupon bonds are as shown.Develop the 3-year bid price of a euro swap quoted against flat USD LIBOR.The current spot exchange rate is $1.50 per €1.00.The size of the swap is €40 million versus $60 million.  In other words,what will you be willing to pay in euro against receiving USD LIBOR?

In other words,what will you be willing to pay in euro against receiving USD LIBOR?

A) 7%

B) 6%

C) 5%

D) None of the above

Correct Answer:

Verified

Correct Answer:

Verified

Q12: A swap bank has identified two companies

Q28: Show how your proposed swap would work

Q30: A major risk faced by a swap

Q38: In the swap market, which position potentially

Q60: Explain how this opportunity affects which swap

Q90: Explain how this opportunity affects which swap

Q93: With regard to a swap bank acting

Q94: Company X wants to borrow $10,000,000 floating

Q95: Company X wants to borrow $10,000,000 floating

Q97: Company X wants to borrow $10,000,000 floating