Multiple Choice

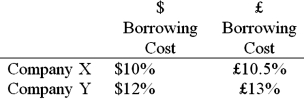

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow £5,000,000 fixed for 5 years. The exchange rate is $2 = £1 and is not expected to change over the next 5 years. Their external borrowing opportunities are:  A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap. In order for X and Y to be interested, they can face no exchange rate risk

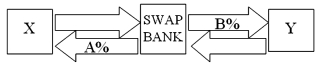

A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap. In order for X and Y to be interested, they can face no exchange rate risk  What must the values of A and B in the graph shown above be in order for the swap to be of interest to firms X and Y?

What must the values of A and B in the graph shown above be in order for the swap to be of interest to firms X and Y?

A) A = $10.50%; B = £12%.

B) A = $10%; B = £13%.

C) A = $12%; B = £13%.

D) A = £10.50%; B = $12%.

Correct Answer:

Verified

Correct Answer:

Verified

Q59: Pricing an interest-only single currency swap after

Q60: Explain how this opportunity affects which swap

Q61: A major risk faced by a swap

Q62: In a currency swap<br>A)it may be the

Q63: An interest-only currency swap has a remaining

Q66: Suppose that you are a swap bank

Q67: A major risk faced by a swap

Q68: Suppose the quote for a five-year swap

Q69: Company X wants to borrow $10,000,000 floating

Q90: Explain how this opportunity affects which swap