Exam 8: Profit Maximization and Competitive Supply

Exam 1: Preliminaries64 Questions

Exam 2: The Basics of Supply and Demand106 Questions

Exam 3: Consumer Behavior132 Questions

Exam 4: Individual and Market Demand123 Questions

Exam 5: Uncertainty and Consumer Behavior144 Questions

Exam 6: Production92 Questions

Exam 7: The Cost of Production149 Questions

Exam 8: Profit Maximization and Competitive Supply130 Questions

Exam 9: The Analysis of Competitive Markets155 Questions

Exam 10: Market Power: Monopoly and Monopsony92 Questions

Exam 11: Pricing With Market Power108 Questions

Exam 12: Monopolistic Competition and Oligopoly91 Questions

Exam 13: Game Theory and Competitive Strategy130 Questions

Exam 14: Markets for Factor Inputs98 Questions

Exam 15: Investment,time and Capital Markets111 Questions

Exam 16: General Equilibrium and Economic Efficiency 1-8392 Questions

Exam 17: Markets With Asymmetric Information78 Questions

Exam 18: Externalities and Public Goods106 Questions

Select questions type

At the profit-maximizing level of output,what is true of the total revenue (TR)and total cost (TC)curves?

Free

(Multiple Choice)

4.9/5  (35)

(35)

Correct Answer: Verified

Verified

E

A firm's producer surplus equals its economic profit when

Free

(Multiple Choice)

4.9/5 (38)

Correct Answer:Verified

D

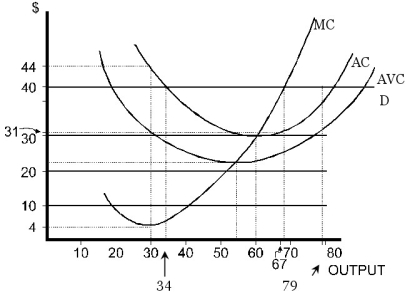

Consider the following diagram where a perfectly competitive firm faces a price of $40.  Figure 8.1

-Refer to Figure 8.1.At the profit-maximizing level of output,AVC is

Figure 8.1

-Refer to Figure 8.1.At the profit-maximizing level of output,AVC is

Free

(Multiple Choice)

4.7/5 (44)

Correct Answer:Verified

B

The textbook for your class was not produced in a perfectly competitive industry because

(Multiple Choice)

4.8/5 (34)

The "perfect information" assumption of perfect competition includes all of the following except one.Which one?

(Multiple Choice)

4.9/5 (42)

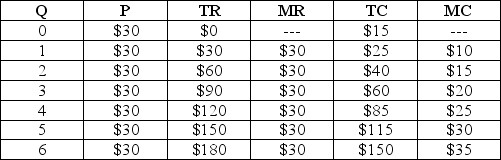

Table 8.1  -Refer to Table 8.1.That the firm is perfectly competitive is evident from its

-Refer to Table 8.1.That the firm is perfectly competitive is evident from its

(Multiple Choice)

4.8/5 (30)

If current output is less than the profit-maximizing output,which must be true?

(Multiple Choice)

4.8/5 (36)

If managers do not choose to maximize profit,but pursue some other goal such as revenue maximization or growth,

(Multiple Choice)

5.0/5 (30)

If price is between AVC and ATC,the best and most practical thing for a perfectly competitive firm to do is

(Multiple Choice)

4.9/5 (27)

Which of the following cases are examples of industries that have potentially increasing costs due to scarce inputs?

(Multiple Choice)

4.8/5 (32)

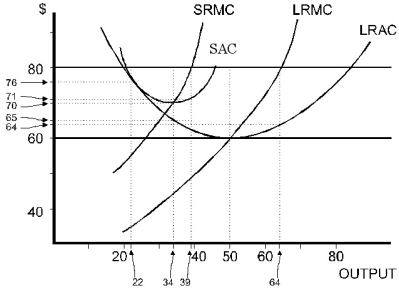

Figure 8.2

-Refer to Figure 8.2.As the competitive industry,not just the firm in question,moves toward long-run equilibrium,the firm will be forced to operate at what level of output?

Figure 8.2

-Refer to Figure 8.2.As the competitive industry,not just the firm in question,moves toward long-run equilibrium,the firm will be forced to operate at what level of output?

(Multiple Choice)

4.8/5 (41)

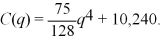

Homer's Boat Manufacturing cost function is:  The marginal cost function is:

The marginal cost function is:  If Homer can sell all the boats he produces for $1,200,what is his optimal output? Calculate Homer's profit or loss.

If Homer can sell all the boats he produces for $1,200,what is his optimal output? Calculate Homer's profit or loss.

(Essay)

4.9/5 (37)

Consider the following statements when answering this question I.In the long-run equilibrium of a perfectly competitive market,a firm's producer surplus equals the sum of the economic rents earned on its inputs to production.

II.In the long-run equilibrium of a perfectly competitive market,the amount of economic profit earned can differ across firms,but not the amount of producer surplus.

(Multiple Choice)

4.8/5 (35)

Figure 8.2

-Refer to Figure 8.2.At P = $80,the profit-maximizing output in the short run is

(Multiple Choice)

4.8/5 (40)

Assume the market for tortillas is perfectly competitive.The market supply and demand curves for tortillas are given as follows:

supply curve:

P = .000002Q demand curve: P = 11 - .00002Q

The short run marginal cost curve for a typical tortilla factory is:

MC = .1 + .0009Q

a.Determine the equilibrium price for tortillas.

b.Determine the profit maximizing short run equilibrium level of output for a tortilla factory.

c.At the level of output determined above,is the factory making a profit,breaking-even,or making a loss? Explain your answer.

d.Assuming that all of the tortilla factories are identical,how many tortilla factories are producing tortillas?

(Essay)

4.8/5 (36)

Figure 8.2

-Refer to Figure 8.2.At P = $80,how much is profit in the short run?

(Multiple Choice)

4.8/5 (37)

When the price faced by a competitive firm was $5,the firm produced nothing in the short run.However,when the price rose to $10,the firm produced 100 tons of output.From this we can infer that

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)