Exam 8: Profit Maximization and Competitive Supply

Exam 1: Preliminaries64 Questions

Exam 2: The Basics of Supply and Demand106 Questions

Exam 3: Consumer Behavior132 Questions

Exam 4: Individual and Market Demand123 Questions

Exam 5: Uncertainty and Consumer Behavior144 Questions

Exam 6: Production92 Questions

Exam 7: The Cost of Production149 Questions

Exam 8: Profit Maximization and Competitive Supply130 Questions

Exam 9: The Analysis of Competitive Markets155 Questions

Exam 10: Market Power: Monopoly and Monopsony92 Questions

Exam 11: Pricing With Market Power108 Questions

Exam 12: Monopolistic Competition and Oligopoly91 Questions

Exam 13: Game Theory and Competitive Strategy130 Questions

Exam 14: Markets for Factor Inputs98 Questions

Exam 15: Investment,time and Capital Markets111 Questions

Exam 16: General Equilibrium and Economic Efficiency 1-8392 Questions

Exam 17: Markets With Asymmetric Information78 Questions

Exam 18: Externalities and Public Goods106 Questions

Select questions type

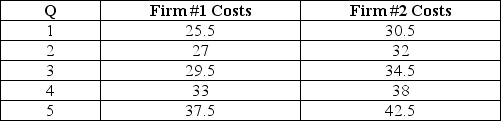

The table below provides cost information for two firms in a competitive industry.Graph the supply curves of the firms individually and jointly.For these two firms,at any positive output level,marginal cost exceeds average variable cost.

(Essay)

4.8/5  (39)

(39)

Although the long-run equilibrium price of oil is $80 per barrel,some producers have much lower costs because their oil reserves are relatively close to the surface and are easier to extract.If the low-cost producers have a minimum LAC equal to $20 per barrel,then the difference ($60 per barrel)is:

(Multiple Choice)

4.8/5 (43)

A few sellers may behave if they operate in a perfectly competitive market is the market demand is:

(Multiple Choice)

4.8/5 (33)

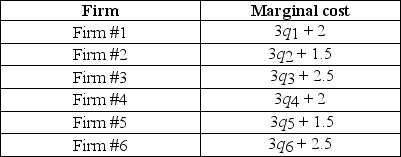

The marginal cost curves of six firms in an industry appear in the table below.If these firms behave competitively,determine the market supply curve.Calculate the elasticity of market supply at $5.

(Essay)

4.8/5 (38)

The amount of output that a firm decides to sell has no effect on the market price in a competitive industry because

(Multiple Choice)

4.9/5 (31)

A competitive market is made up of 100 identical firms.Each firm has a short-run marginal cost function as follows:

MC = 5 + 0.5Q,

where Q represents units of output per unit of time.The firm's average variable cost curve intersects the marginal cost at a vertical distance of 10 above the horizontal axis.Determine the market short-run supply curve.Calculate the price that would make 2,000 units forthcoming per time period.Note the minimum price at which any quantity would be placed on the market.

(Essay)

4.8/5 (30)

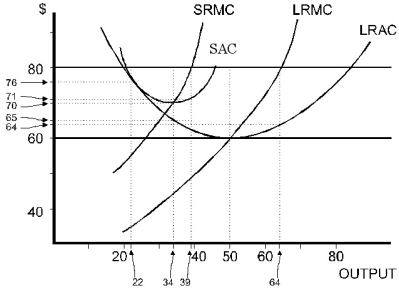

Figure 8.2

-Refer to Figure 8.2.As the firm makes its long-run adjustment,which must be true?

Figure 8.2

-Refer to Figure 8.2.As the firm makes its long-run adjustment,which must be true?

(Multiple Choice)

4.9/5 (30)

Which of the following is NOT a necessary condition for long-run equilibrium under perfect competition?

(Multiple Choice)

4.9/5 (40)

The following table contains information for a price taking competitive firm.Complete the table and determine the profit maximizing level of output (round your answer to the nearest whole number).

Total Marginal Fixed Average Total Average Marginal

Output Cost Cost Cost Cost Revenue Revenue Revenue

0 25

1 35

2 30

3 45

4 185

5 57

6 120 240

(Essay)

4.8/5 (29)

Figure 8.2

-Refer to Figure 8.2.If the firm expects $80 to be the long-run price,how many units of output will it plan to produce in the long run?

(Multiple Choice)

5.0/5 (37)

Scenario 8.2:

Yachts are produced by a perfectly competitive industry in Dystopia.Industry output (Q)is currently 30,000 yachts per year.The government,in an attempt to raise revenue,places a $20,000 tax on each yacht.Demand is highly,but not perfectly,elastic.

-Refer to Scenario 8.2.The more elastic is demand for yachts,

(Multiple Choice)

4.8/5 (44)

A competitive firm sells its product at a price of $0.10 per unit.Its total and marginal cost functions are:

TC = 5 - 0.5Q + 0.001Q2

MC = -0.5 + 0.002Q,

where TC is total cost ($)and Q is output rate (units per time period).

a.Determine the output rate that maximizes profit or minimizes losses in the shortterm.

b.If input prices increase and cause the cost functions to become

TC = 5 - 0.10Q + 0.002Q2

MC = -0.10 + 0.004Q,

what will the new equilibrium output rate be? Explain what happened to the profit maximizing output rate when input prices were increased.

(Essay)

4.9/5 (34)

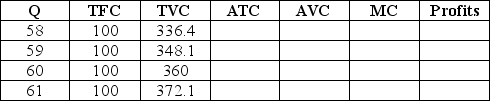

The table below lists the short-run costs for One Guy's Pizza.If One Guy's can sell all the output they produce for $12 per unit,how much should One Guy's produce to maximize profits? Does One Guy's Pizza earn an economic profit in the short-run?

(Essay)

4.8/5 (43)

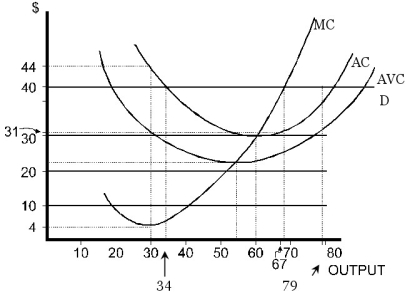

Consider the following diagram where a perfectly competitive firm faces a price of $40.  Figure 8.1

-Refer to Figure 8.1.At the profit-maximizing level of output,

Figure 8.1

-Refer to Figure 8.1.At the profit-maximizing level of output,

(Multiple Choice)

4.8/5 (43)

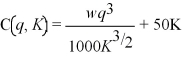

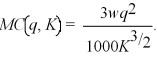

Sarah's Pretzel plant has the following short-run cost function:  where q is Sarah's output level,w is the cost of a labor hour,and K is the number of pretzel machines Sarah leases.Sarah's short-run marginal cost curve is

where q is Sarah's output level,w is the cost of a labor hour,and K is the number of pretzel machines Sarah leases.Sarah's short-run marginal cost curve is  At the moment,Sarah leases 10 pretzel machines,the cost of a labor hour is $6.85,and she can sell all the output she produces at $35 per unit.If the cost per labor hour rises to $7.50,what happens to Sarah's optimal level of output and profits?

At the moment,Sarah leases 10 pretzel machines,the cost of a labor hour is $6.85,and she can sell all the output she produces at $35 per unit.If the cost per labor hour rises to $7.50,what happens to Sarah's optimal level of output and profits?

(Essay)

4.9/5 (40)

In the short run,a perfectly competitive firm earning negative economic profit

(Multiple Choice)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)