Exam 6: The Supply Curve and the Behavior of Firms

Exam 1: The Central Idea155 Questions

Exam 2: Observing and Explaining the Economy108 Questions

Exam 3: The Supply and Demand Model170 Questions

Exam 4: Subtleties of the Supply and Demand Model: Price Floors, Price Ceilings, and Elasticity179 Questions

Exam 5: The Demand Curve and the Behavior of Consumers136 Questions

Exam 6: The Supply Curve and the Behavior of Firms182 Questions

Exam 7: The Interaction of People in Markets158 Questions

Exam 8: Costs and the Changes at Firms Over Time172 Questions

Exam 9: The Rise and Fall of Industries139 Questions

Exam 10: Monopoly182 Questions

Exam 11: Product Differentiation, Monopolistic Competition, and Oligopoly169 Questions

Exam 12: Antitrust Policy and Regulation152 Questions

Exam 13: Labor Markets179 Questions

Exam 14: Taxes, Transfers, and Income Distribution180 Questions

Exam 15: Public Goods, Externalities, and Government Behavior201 Questions

Exam 16: Capital and Financial Markets174 Questions

Exam 17: Reading, Understanding, and Creating Graphs35 Questions

Exam 18: Consumer Theory With Indifference Curves39 Questions

Exam 19: Producer Theory With Isoquants19 Questions

Select questions type

If supply is perfectly elastic,

Free

(Multiple Choice)

4.8/5  (39)

(39)

Correct Answer: Verified

Verified

A

All types of firms suffer from managerial conflicts.

Free

(True/False)

4.8/5 (37)

Correct Answer:Verified

False

What is the assumption of a competitive market and what are the implications of this assumption? Provide one example of this type of market.

Free

(Essay)

4.7/5 (36)

Correct Answer:Verified

In a competitive market, there are many firms such that individual firms have no ability to affect the price that prevails in the market. As a result, the firm becomes a price-taker, meaning it cannot charge a price far from the price that other firms are charging in the market without losing all its customers. A good example is the commodity market, such as wheat and corn, where the product is homogenous and there is a large number of sellers so that no one seller can control the market price.

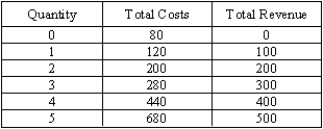

Refer to the table below. Find the fixed costs and the producer surplus when the firm produces the profit-maximizing quantity. What is the relationship between producer surplus and fixed costs?

(Essay)

4.7/5 (41)

Partnerships differ from sole proprietorships because partnerships

(Multiple Choice)

4.9/5 (36)

In the pumpkin-growing firm example in the text, land is a fixed factor because

(Multiple Choice)

4.8/5 (28)

Exhibit 6-6  -Refer to Exhibit 6-6. Let market price be $10 and fixed costs be $13. Calculate the difference between revenue and total costs at the output the profit-maximizing firm will produce.

-Refer to Exhibit 6-6. Let market price be $10 and fixed costs be $13. Calculate the difference between revenue and total costs at the output the profit-maximizing firm will produce.

(Essay)

4.9/5 (45)

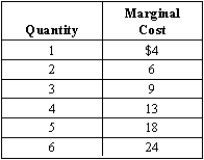

An improvement in production technology shifts marginal cost

(Multiple Choice)

4.7/5 (36)

Producer surplus is just an economist's technical name for profit.

(True/False)

4.7/5 (36)

Separation of ownership from control is most commonly found in a

(Multiple Choice)

4.8/5 (33)

Explain what happens to market supply when a new firm enters a market, holding everything else equal.

(Essay)

4.8/5 (33)

Why does it not make sense to sum individual firms' supply prices at every quantity rather than summing individual firms' supply quantities at every price?

(Essay)

4.8/5 (41)

Draw a graph of total revenue and total cost for a competitive firm that is maximizing profit but just breaking even. Mark the profit-maximizing output level.

(Essay)

4.9/5 (46)

If the market price of a good is $3, then a profit-maximizing competitive firm will produce

(Multiple Choice)

4.7/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)