Exam 6: The Supply Curve and the Behavior of Firms

Exam 1: The Central Idea155 Questions

Exam 2: Observing and Explaining the Economy108 Questions

Exam 3: The Supply and Demand Model170 Questions

Exam 4: Subtleties of the Supply and Demand Model: Price Floors, Price Ceilings, and Elasticity179 Questions

Exam 5: The Demand Curve and the Behavior of Consumers136 Questions

Exam 6: The Supply Curve and the Behavior of Firms182 Questions

Exam 7: The Interaction of People in Markets158 Questions

Exam 8: Costs and the Changes at Firms Over Time172 Questions

Exam 9: The Rise and Fall of Industries139 Questions

Exam 10: Monopoly182 Questions

Exam 11: Product Differentiation, Monopolistic Competition, and Oligopoly169 Questions

Exam 12: Antitrust Policy and Regulation152 Questions

Exam 13: Labor Markets179 Questions

Exam 14: Taxes, Transfers, and Income Distribution180 Questions

Exam 15: Public Goods, Externalities, and Government Behavior201 Questions

Exam 16: Capital and Financial Markets174 Questions

Exam 17: Reading, Understanding, and Creating Graphs35 Questions

Exam 18: Consumer Theory With Indifference Curves39 Questions

Exam 19: Producer Theory With Isoquants19 Questions

Select questions type

In a market diagram, producer surplus is shaped like a triangle bounded by the vertical axis, the demand curve, and the supply curve.

(True/False)

4.8/5  (39)

(39)

How much a firm changes its output in response to a price change is captured by the firm's

(Multiple Choice)

4.7/5 (28)

A competitive market is one in which many firms compete for customers and end up charging a common market price.

(True/False)

4.8/5 (34)

The market supply curve tends to get steeper as output increases.

(True/False)

4.9/5 (32)

An increase in market demand has no effect on producer surplus because producer surplus is related to supply.

(True/False)

4.7/5 (30)

For a single competitive firm, marginal revenue is equivalent to

(Multiple Choice)

4.7/5 (32)

Name one industry in which firms are price-takers. Name one industry in which firms are not price-takers. Suppose you set up a business where you sell lemonade on a street. Would you be a price-taker or a price-maker?

(Essay)

4.7/5 (37)

Which of the following statements is true for any profit-maximizing firm?

(Multiple Choice)

4.9/5 (40)

Refer to Exhibit 6-1. Diminishing returns to labor is illustrated by

(Multiple Choice)

4.9/5 (29)

Profit maximization is the basic assumption for all types of corporations, but not for sole proprietorships.

(True/False)

4.9/5 (30)

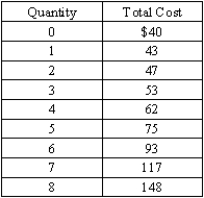

Exhibit 6-3  -Refer to Exhibit 6-3. What is the profit-maximizing output level if output price is $16?

-Refer to Exhibit 6-3. What is the profit-maximizing output level if output price is $16?

(Essay)

4.8/5 (36)

The added revenue that comes from producing and selling another unit of a good is called

(Multiple Choice)

4.7/5 (33)

A production function is a straight line because of diminishing returns to labor.

(True/False)

4.8/5 (36)

The market supply curve is obtained by summing the total costs of all firms in the market.

(True/False)

4.8/5 (28)

The slope of the production function turns from positive to negative when the marginal product of labor turns from positive to negative.

(True/False)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)