Exam 6: The Supply Curve and the Behavior of Firms

Exam 1: The Central Idea155 Questions

Exam 2: Observing and Explaining the Economy108 Questions

Exam 3: The Supply and Demand Model170 Questions

Exam 4: Subtleties of the Supply and Demand Model: Price Floors, Price Ceilings, and Elasticity179 Questions

Exam 5: The Demand Curve and the Behavior of Consumers136 Questions

Exam 6: The Supply Curve and the Behavior of Firms182 Questions

Exam 7: The Interaction of People in Markets158 Questions

Exam 8: Costs and the Changes at Firms Over Time172 Questions

Exam 9: The Rise and Fall of Industries139 Questions

Exam 10: Monopoly182 Questions

Exam 11: Product Differentiation, Monopolistic Competition, and Oligopoly169 Questions

Exam 12: Antitrust Policy and Regulation152 Questions

Exam 13: Labor Markets179 Questions

Exam 14: Taxes, Transfers, and Income Distribution180 Questions

Exam 15: Public Goods, Externalities, and Government Behavior201 Questions

Exam 16: Capital and Financial Markets174 Questions

Exam 17: Reading, Understanding, and Creating Graphs35 Questions

Exam 18: Consumer Theory With Indifference Curves39 Questions

Exam 19: Producer Theory With Isoquants19 Questions

Select questions type

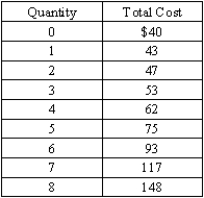

Exhibit 6-3  -Refer to Exhibit 6-3. Calculate the marginal cost for each of these units of output: third, fifth, and eighth.

-Refer to Exhibit 6-3. Calculate the marginal cost for each of these units of output: third, fifth, and eighth.

(Essay)

4.8/5  (34)

(34)

In contrast with a firm in a competitive market, a monopoly is able to control

(Multiple Choice)

4.8/5 (42)

When output changes, the profit-maximizing firm must consider

(Multiple Choice)

4.8/5 (33)

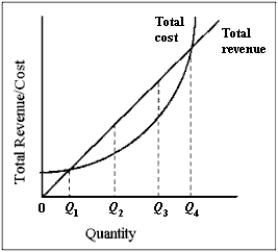

Exhibit 6-5  -Refer to Exhibit 6-5. Which of the following statements is not true?

-Refer to Exhibit 6-5. Which of the following statements is not true?

(Multiple Choice)

4.8/5 (47)

A firm that considers price as a given and chooses quantity of output accordingly is called a

(Multiple Choice)

4.8/5 (44)

Marginal product decreases as labor increases because marginal cost is rising.

(True/False)

4.8/5 (41)

When more producers enter a competitive market, the market supply curve

(Multiple Choice)

4.7/5 (32)

Define diminishing returns in production and illustrate it with the graph of a production function.

(Essay)

5.0/5 (42)

If marginal cost increases, then the market supply curve shifts to the left.

(True/False)

4.8/5 (39)

The curve that indicates how much output a profit-maximizing competitive firm will produce at any given price is the

(Multiple Choice)

4.8/5 (40)

Exhibit 6-4  -Refer to Exhibit 6-4. If output price is $14, the profit-maximizing output level is ____ units.

-Refer to Exhibit 6-4. If output price is $14, the profit-maximizing output level is ____ units.

(Multiple Choice)

4.9/5 (41)

The approach based on the relationship between price and marginal cost brings about the same supply curve as what is implied by the approach based on profit maximization.

(True/False)

4.9/5 (38)

Exhibit 6-4

-Refer to Exhibit 6-4. Assume that fixed costs equal $30. If the price is $20, the profit that results at the profit-maximizing output level is

(Multiple Choice)

4.8/5 (39)

What is the relationship between the slope of the total cost curve and marginal cost? Explain.

(Essay)

4.9/5 (38)

Which of the following is typically a variable factor of production?

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)