Exam 9: The Rise and Fall of Industries

Exam 1: The Central Idea156 Questions

Exam 2: Observing and Explaining the Economy143 Questions

Exam 3: The Supply and Demand Model166 Questions

Exam 4: Subtleties of the Supply and Demand Model176 Questions

Exam 5: The Demand Curve and the Behavior of Consumers176 Questions

Exam 6: The Supply Curve and the Behavior of Firms179 Questions

Exam 7: The Efficiency of Markets163 Questions

Exam 8: Costs and the Changes at Firms Over Time191 Questions

Exam 9: The Rise and Fall of Industries139 Questions

Exam 10: Monopoly184 Questions

Exam 11: Product Differentiation, Monopolistic Competition, and Oligopoly169 Questions

Exam 12: Antitrust Policy and Regulation152 Questions

Exam 13: Labor Markets179 Questions

Exam 14: Taxes, Transfers, and Income Distribution179 Questions

Exam 15: Public Goods, Externalities, and Government Behavior197 Questions

Exam 16: Capital and Financial Markets188 Questions

Exam 17: Macroeconomics: the Big Picture159 Questions

Exam 18: Measuring the Production, Income, and Spending of Nations177 Questions

Exam 19: The Spending Allocation Model166 Questions

Exam 20: Unemployment and Employment212 Questions

Exam 21: Productivity and Economic Growth162 Questions

Exam 22: Money and Inflation153 Questions

Exam 23: The Nature and Causes of Economic Fluctuations185 Questions

Exam 24: The Economic Fluctuations Model205 Questions

Exam 25: Using the Economic Fluctuations Model176 Questions

Exam 26: Fiscal Policy138 Questions

Exam 27: Monetary Policy180 Questions

Exam 28: Economic Growth Around the World157 Questions

Exam 29: International Trade242 Questions

Exam 30: International Finance125 Questions

Select questions type

Which of the following is a condition for industry expansion through expansion of existing firms instead of entry of new firms?

Free

(Multiple Choice)

4.8/5  (43)

(43)

Correct Answer: Verified

Verified

C

When economic profit is equal to zero, we say that

Free

(Multiple Choice)

4.7/5 (27)

Correct Answer:Verified

B

In the long run, market supply increases as market demand increases.

Free

(True/False)

4.8/5 (30)

Correct Answer:Verified

True

In the long run, if price is greater than average total cost in an industry, then

(Multiple Choice)

4.8/5 (32)

In a competitive industry, which of the following cannot be true for a firm in the long run?

(Multiple Choice)

4.9/5 (32)

If losses are incurred in a competitive industry, then over the long run, we can expect a greater quantity supplied because market price will rise.

(True/False)

4.7/5 (37)

Explain what is wrong with the following statement: "It's not fair that firms profit so highly in an industry that benefits from new, cost saving technology; they should have to immediately pass cost savings directly on to the consumer."

(Essay)

4.7/5 (34)

External diseconomies of scale cause an industry's long-run supply curve to slope upward.

(True/False)

4.8/5 (34)

When the market price in long-run equilibrium remains unchanged after an industry expands, then the long-run industry supply curve

(Multiple Choice)

4.8/5 (36)

A group of firms, each of which produces similar products, is called a(n)

(Multiple Choice)

4.7/5 (31)

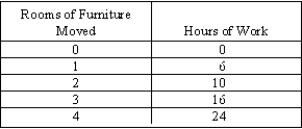

A moving company has $20 in fixed costs per day and pays an hourly wage of $10 per worker. The moving company is paid $80 for each room of furniture it moves. The daily production function of the firm is as follows:

(Essay)

4.8/5 (37)

Suppose a dentist has total revenue of $320,000, and his total costs are $250,000 for the year. Also suppose the dentist left a job paying $112,000 a year to start his own practice. What is the dentist's economic profit?

(Multiple Choice)

4.7/5 (42)

A firm earns normal profit if its total revenue is greater than its total cost.

(True/False)

4.8/5 (32)

An increase in market demand can be shown by shifting a firm's demand curve to the right.

(True/False)

4.9/5 (31)

If market demand decreases in a market previously in long-run equilibrium,

(Multiple Choice)

4.9/5 (42)

An increase in market price is likely to result in more firm entry in the long run.

(True/False)

4.7/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)