Exam 7: The Efficiency of Markets

Exam 1: The Central Idea156 Questions

Exam 2: Observing and Explaining the Economy143 Questions

Exam 3: The Supply and Demand Model166 Questions

Exam 4: Subtleties of the Supply and Demand Model176 Questions

Exam 5: The Demand Curve and the Behavior of Consumers176 Questions

Exam 6: The Supply Curve and the Behavior of Firms179 Questions

Exam 7: The Efficiency of Markets163 Questions

Exam 8: Costs and the Changes at Firms Over Time191 Questions

Exam 9: The Rise and Fall of Industries139 Questions

Exam 10: Monopoly184 Questions

Exam 11: Product Differentiation, Monopolistic Competition, and Oligopoly169 Questions

Exam 12: Antitrust Policy and Regulation152 Questions

Exam 13: Labor Markets179 Questions

Exam 14: Taxes, Transfers, and Income Distribution179 Questions

Exam 15: Public Goods, Externalities, and Government Behavior197 Questions

Exam 16: Capital and Financial Markets188 Questions

Exam 17: Macroeconomics: the Big Picture159 Questions

Exam 18: Measuring the Production, Income, and Spending of Nations177 Questions

Exam 19: The Spending Allocation Model166 Questions

Exam 20: Unemployment and Employment212 Questions

Exam 21: Productivity and Economic Growth162 Questions

Exam 22: Money and Inflation153 Questions

Exam 23: The Nature and Causes of Economic Fluctuations185 Questions

Exam 24: The Economic Fluctuations Model205 Questions

Exam 25: Using the Economic Fluctuations Model176 Questions

Exam 26: Fiscal Policy138 Questions

Exam 27: Monetary Policy180 Questions

Exam 28: Economic Growth Around the World157 Questions

Exam 29: International Trade242 Questions

Exam 30: International Finance125 Questions

Select questions type

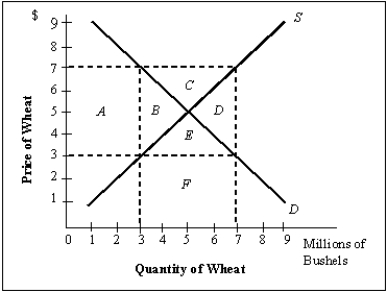

Market equilibrium is achieved when consumer surplus is equal to producer surplus.

Free

(True/False)

4.9/5  (33)

(33)

Correct Answer: Verified

Verified

False

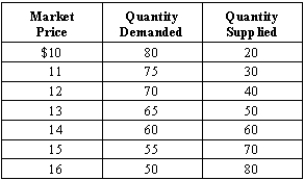

Exhibit 7-10  -Refer to Exhibit 7-10. What would the tax revenue be if the government imposed on producers a tax of $3 per unit sold?

-Refer to Exhibit 7-10. What would the tax revenue be if the government imposed on producers a tax of $3 per unit sold?

Free

(Multiple Choice)

4.8/5 (29)

Correct Answer:Verified

B

A tax on a good results in no deadweight loss if consumers and producers share the benefits of the tax revenues.

Free

(True/False)

4.9/5 (32)

Correct Answer:Verified

False

In a market, the sum of producer and consumer surplus is maximized when marginal benefit is greater than marginal cost.

(True/False)

4.9/5 (39)

Exhibit 7-10

-Refer to Exhibit 7-10. If the government imposed on consumers a tax of $3 per unit bought, the tax revenue would be

(Multiple Choice)

4.8/5 (33)

Exhibit 7-11  -A competitive equilibrium model does a good job of predicting the effects of the introduction of a new tax on a good or service.

-A competitive equilibrium model does a good job of predicting the effects of the introduction of a new tax on a good or service.

(True/False)

4.8/5 (41)

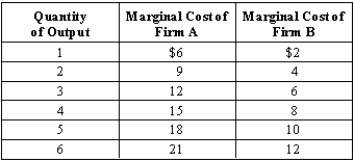

Exhibit 7-1  -Refer to Exhibit 7-1. Firm A has much higher costs of production, and under no circumstances should it produce when Firm B is already producing.

-Refer to Exhibit 7-1. Firm A has much higher costs of production, and under no circumstances should it produce when Firm B is already producing.

(True/False)

4.8/5 (43)

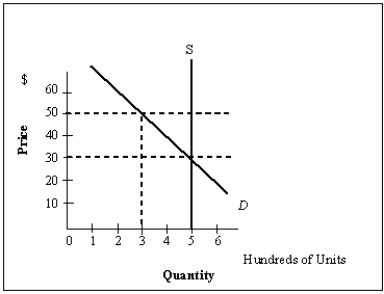

Exhibit 7-6  -Refer to Exhibit 7-6. The deadweight loss that results from a minimum price of $50 being established in the market is

-Refer to Exhibit 7-6. The deadweight loss that results from a minimum price of $50 being established in the market is

(Multiple Choice)

4.9/5 (39)

All of the following are conditions of Pareto efficiency except

(Multiple Choice)

5.0/5 (36)

Exhibit 7-10

-Refer to Exhibit 7-10. What would the new equilibrium quantity be if the government assessed on producers a tax of $3 per unit sold?

(Multiple Choice)

4.8/5 (34)

The equilibrium price in a competitive equilibrium model is determined by supply and demand.

(True/False)

4.7/5 (37)

A tax that is assessed on producers has no effect on a product's price if

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)