Exam 9: Aggregate Demand

Exam 1: Economics: the Core Issues143 Questions

Exam 2: The Us Economy: a Global View151 Questions

Exam 3: Supply and Demand164 Questions

Exam 4: The Role of Government152 Questions

Exam 5: National Income Accounting126 Questions

Exam 6: Unemployment134 Questions

Exam 7: Inflation150 Questions

Exam 8: The Business Cycle147 Questions

Exam 9: Aggregate Demand149 Questions

Exam 10: Self-Adjustment or Instability151 Questions

Exam 11: Fiscal Policy152 Questions

Exam 12: Deficits and Debt149 Questions

Exam 13: Money and Banks150 Questions

Exam 14: The Federal Reserve System148 Questions

Exam 15: Monetary Policy148 Questions

Exam 16: Supply-Side Policy: Short-Run Options141 Questions

Exam 17: Growth and Productivity: Long-Run Possibilities145 Questions

Exam 18: Theory Versus Reality142 Questions

Exam 19: International Trade139 Questions

Exam 20: International Finance144 Questions

Exam 21: Global Poverty Glossary Index Reference Tables155 Questions

Exam 22: International Economics150 Questions

Exam 23: International Economics150 Questions

Select questions type

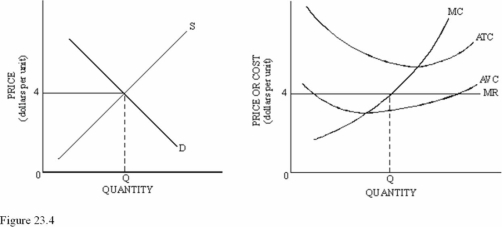

Refer to Figure 23.4. In the long run, which of the following would not be expected?

Refer to Figure 23.4. In the long run, which of the following would not be expected?

(Multiple Choice)

4.8/5  (35)

(35)

Minimizing average total cost always leads to the maximization of total profit.

(True/False)

4.8/5 (33)

Technological improvements shift the average total cost curve and the marginal cost curve downward.

(True/False)

4.7/5 (39)

The market supply curve in a perfectly competitive market is usually

(Multiple Choice)

4.9/5 (36)

The marginal cost pricing characteristic of competitive markets permits society to efficiently answer the WHAT to produce question.

(True/False)

4.8/5 (38)

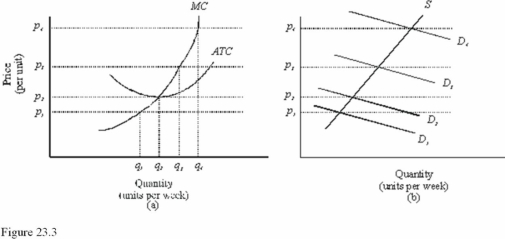

In Figure 23.3, diagram "a" presents the cost curves that are relevant to a firm's production decision, and diagram "b" shows the market demand and supply curves for the market. Use both diagrams to answer the following question: In Figure 23.3, at a price of p2 in the long run

In Figure 23.3, diagram "a" presents the cost curves that are relevant to a firm's production decision, and diagram "b" shows the market demand and supply curves for the market. Use both diagrams to answer the following question: In Figure 23.3, at a price of p2 in the long run

(Multiple Choice)

4.8/5 (38)

When economic profits exist in the market for a particular product, this is a signal to producers that

(Multiple Choice)

4.8/5 (42)

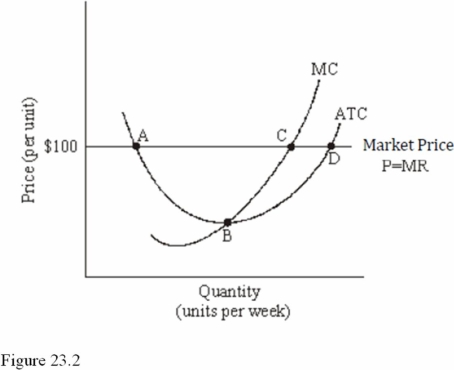

Refer to Figure 23.2 for a perfectly competitive firm. If this firm produces the level of output corresponding to point C in the short run, it will earn

Refer to Figure 23.2 for a perfectly competitive firm. If this firm produces the level of output corresponding to point C in the short run, it will earn

(Multiple Choice)

4.9/5 (37)

Economic losses mean that firms will exit from a market in the short run.

(True/False)

4.9/5 (35)

Investment decisions are made on the basis of the relationship of price to

(Multiple Choice)

4.9/5 (37)

Maximizing profits per unit always leads to the maximization of total profit.

(True/False)

4.7/5 (52)

Marginal cost pricing results in the most desirable mix of goods and services from the consumer's standpoint because

(Multiple Choice)

4.9/5 (36)

One World View article is titled "Flat Panels, Thin Margins." New firms continue to enter the industry even though prices are falling because

(Multiple Choice)

4.8/5 (39)

To maximize profits, a competitive firm will seek to expand output until

(Multiple Choice)

4.9/5 (36)

Market supply is the horizontal sum of the individual MC curves above the AVC in a perfectly competitive market.

(True/False)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)