Exam 9: Aggregate Demand

Exam 1: Economics: the Core Issues143 Questions

Exam 2: The Us Economy: a Global View151 Questions

Exam 3: Supply and Demand164 Questions

Exam 4: The Role of Government152 Questions

Exam 5: National Income Accounting126 Questions

Exam 6: Unemployment134 Questions

Exam 7: Inflation150 Questions

Exam 8: The Business Cycle147 Questions

Exam 9: Aggregate Demand149 Questions

Exam 10: Self-Adjustment or Instability151 Questions

Exam 11: Fiscal Policy152 Questions

Exam 12: Deficits and Debt149 Questions

Exam 13: Money and Banks150 Questions

Exam 14: The Federal Reserve System148 Questions

Exam 15: Monetary Policy148 Questions

Exam 16: Supply-Side Policy: Short-Run Options141 Questions

Exam 17: Growth and Productivity: Long-Run Possibilities145 Questions

Exam 18: Theory Versus Reality142 Questions

Exam 19: International Trade139 Questions

Exam 20: International Finance144 Questions

Exam 21: Global Poverty Glossary Index Reference Tables155 Questions

Exam 22: International Economics150 Questions

Exam 23: International Economics150 Questions

Select questions type

Suppose a perfectly competitive firm is experiencing zero economic profits. In an effort to increase profits, the firm decides to initiate an advertising campaign for its product. The most likely short-run result of this campaign, ceteris paribus, would be

(Multiple Choice)

4.8/5  (39)

(39)

As in other industries, the market structure of the computer industry has evolved over time. It began as a monopoly and then became perfectly competitive.

(True/False)

4.9/5 (41)

A perfectly competitive market results in efficiency because

(Multiple Choice)

4.7/5 (48)

Perfectly competitive firms are heavy advertisers because they produce differentiated products.

(True/False)

4.8/5 (35)

Because a perfectly competitive firm has no market power, its marginal cost curve is flat (i.e., horizontal).

(True/False)

4.9/5 (29)

Marginal cost pricing in competitive markets results in all but which one of the following?

(Multiple Choice)

4.7/5 (35)

A competitive market creates strong pressure for technological innovation that

(Multiple Choice)

4.9/5 (45)

Barriers to entry are obstacles that make it difficult or impossible for would-be producers to enter a particular market.

(True/False)

4.9/5 (40)

Explain how the market supply curve is derived in a perfectly competitive market. Identify five factors that would cause the market supply curve to shift.

(Essay)

4.8/5 (39)

The "Tablet Brigade" In the News article indicates that the success of the iPad

(Multiple Choice)

4.9/5 (30)

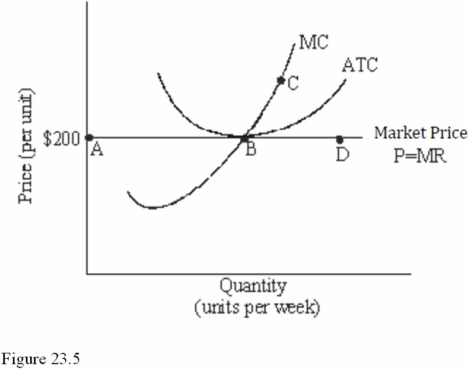

Refer to Figure 23.5 for a perfectly competitive firm. If more efficient production techniques were developed in this market, which of the following changes would we expect to occur, ceteris paribus?

Refer to Figure 23.5 for a perfectly competitive firm. If more efficient production techniques were developed in this market, which of the following changes would we expect to occur, ceteris paribus?

(Multiple Choice)

4.9/5 (35)

Other things being equal, as more firms enter a market, the market supply curve

(Multiple Choice)

4.7/5 (42)

Perfectly competitive firms cannot individually affect market price because

(Multiple Choice)

4.8/5 (34)

When a firm is earning positive economic profits, this is an indication that the firm

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)