Exam 9: Aggregate Demand

Exam 1: Economics: the Core Issues143 Questions

Exam 2: The Us Economy: a Global View151 Questions

Exam 3: Supply and Demand164 Questions

Exam 4: The Role of Government152 Questions

Exam 5: National Income Accounting126 Questions

Exam 6: Unemployment134 Questions

Exam 7: Inflation150 Questions

Exam 8: The Business Cycle147 Questions

Exam 9: Aggregate Demand149 Questions

Exam 10: Self-Adjustment or Instability151 Questions

Exam 11: Fiscal Policy152 Questions

Exam 12: Deficits and Debt149 Questions

Exam 13: Money and Banks150 Questions

Exam 14: The Federal Reserve System148 Questions

Exam 15: Monetary Policy148 Questions

Exam 16: Supply-Side Policy: Short-Run Options141 Questions

Exam 17: Growth and Productivity: Long-Run Possibilities145 Questions

Exam 18: Theory Versus Reality142 Questions

Exam 19: International Trade139 Questions

Exam 20: International Finance144 Questions

Exam 21: Global Poverty Glossary Index Reference Tables155 Questions

Exam 22: International Economics150 Questions

Exam 23: International Economics150 Questions

Select questions type

In a perfectly competitive market, when price is equal to the

(Multiple Choice)

4.9/5  (37)

(37)

Which of the following is consistent with long-run equilibrium for a perfectly competitive market?

(Multiple Choice)

4.8/5 (36)

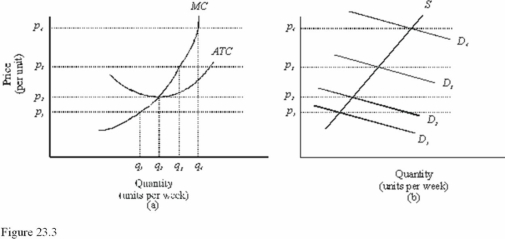

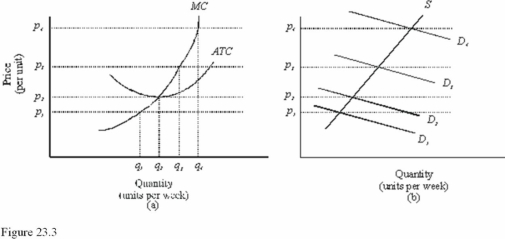

In Figure 23.3, diagram "a" presents the cost curves that are relevant to a firm's production decision, and diagram "b" shows the market demand and supply curves for the market. Use both diagrams to answer the following question: If the market demand curve is D2 in Figure 23.3, then in the long run,

In Figure 23.3, diagram "a" presents the cost curves that are relevant to a firm's production decision, and diagram "b" shows the market demand and supply curves for the market. Use both diagrams to answer the following question: If the market demand curve is D2 in Figure 23.3, then in the long run,

(Multiple Choice)

4.8/5 (38)

If catfish farmers expect catfish prices to fall in the future, then right now

(Multiple Choice)

4.7/5 (33)

Which of the following characterizes a firm that is in long-run perfectly competitive equilibrium where profits are maximized?

(Multiple Choice)

4.8/5 (32)

In Figure 23.3, diagram "a" presents the cost curves that are relevant to a firm's production decision, and diagram "b" shows the market demand and supply curves for the market. Use both diagrams to answer the following question: In the long run, at prices below p2 in Figure 23.3,

In Figure 23.3, diagram "a" presents the cost curves that are relevant to a firm's production decision, and diagram "b" shows the market demand and supply curves for the market. Use both diagrams to answer the following question: In the long run, at prices below p2 in Figure 23.3,

(Multiple Choice)

4.7/5 (37)

Which of the following is true about a competitive market supply curve?

(Multiple Choice)

4.9/5 (37)

In a competitive market where firms are earning economic losses, which of the following should be expected as the industry moves to long-run equilibrium, ceteris paribus?

(Multiple Choice)

4.8/5 (36)

Explain how a perfectly competitive market promotes productive efficiency (minimum average costs).

(Essay)

4.8/5 (33)

Competitive market pressures were a driving force in the spectacular growth of the computer industry.

(True/False)

4.9/5 (36)

Perfectly competitive firms always earn economic profits in the short run.

(True/False)

4.8/5 (27)

For a perfectly competitive market, long-run equilibrium is characterized by all of the following but which one?

(Multiple Choice)

4.8/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)