Exam 9: Aggregate Demand

Exam 1: Economics: the Core Issues143 Questions

Exam 2: The Us Economy: a Global View151 Questions

Exam 3: Supply and Demand164 Questions

Exam 4: The Role of Government152 Questions

Exam 5: National Income Accounting126 Questions

Exam 6: Unemployment134 Questions

Exam 7: Inflation150 Questions

Exam 8: The Business Cycle147 Questions

Exam 9: Aggregate Demand149 Questions

Exam 10: Self-Adjustment or Instability151 Questions

Exam 11: Fiscal Policy152 Questions

Exam 12: Deficits and Debt149 Questions

Exam 13: Money and Banks150 Questions

Exam 14: The Federal Reserve System148 Questions

Exam 15: Monetary Policy148 Questions

Exam 16: Supply-Side Policy: Short-Run Options141 Questions

Exam 17: Growth and Productivity: Long-Run Possibilities145 Questions

Exam 18: Theory Versus Reality142 Questions

Exam 19: International Trade139 Questions

Exam 20: International Finance144 Questions

Exam 21: Global Poverty Glossary Index Reference Tables155 Questions

Exam 22: International Economics150 Questions

Exam 23: International Economics150 Questions

Select questions type

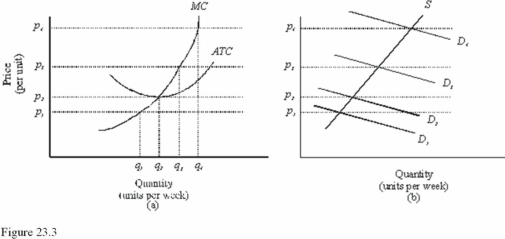

In Figure 23.3, diagram "a" presents the cost curves that are relevant to a firm's production decision, and diagram "b" shows the market demand and supply curves for the market. Use both diagrams to answer the following question: In Figure 23.3, at a price of p3 in the long run

In Figure 23.3, diagram "a" presents the cost curves that are relevant to a firm's production decision, and diagram "b" shows the market demand and supply curves for the market. Use both diagrams to answer the following question: In Figure 23.3, at a price of p3 in the long run

(Multiple Choice)

4.8/5  (26)

(26)

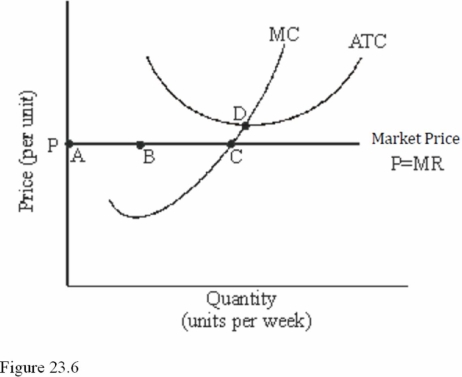

Refer to Figure 23.6 for a perfectly competitive firm. If this firm produces the level of output corresponding to point B in the short run, it will earn

Refer to Figure 23.6 for a perfectly competitive firm. If this firm produces the level of output corresponding to point B in the short run, it will earn

(Multiple Choice)

4.9/5 (40)

In a perfectly competitive market, firms will earn zero economic profits in the long run.

(True/False)

4.8/5 (36)

In the short run, a perfectly competitive firm's production decision aims to maximize profits at the production rate where P = MR = MC.

(True/False)

4.8/5 (31)

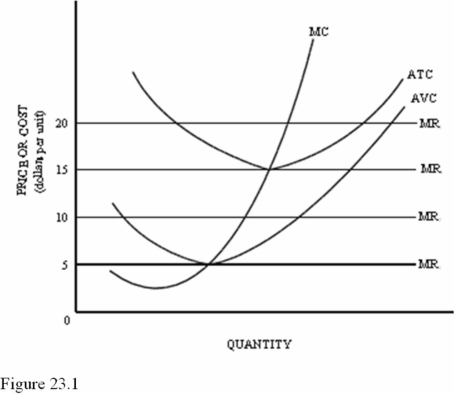

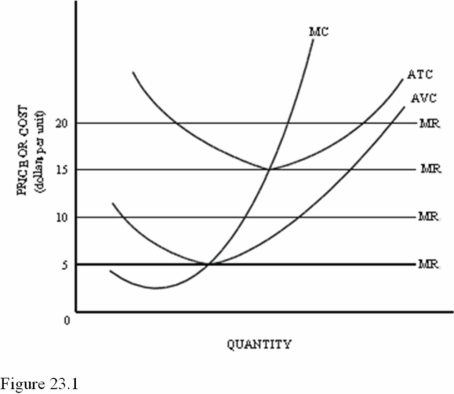

Refer to Figure 23.1 for a perfectly competitive firm. In the long run, this firm would stay in this market only if the market price was equal to or higher than

Refer to Figure 23.1 for a perfectly competitive firm. In the long run, this firm would stay in this market only if the market price was equal to or higher than

(Multiple Choice)

4.7/5 (31)

If someone invents a better way to produce frozen pizzas, then

(Multiple Choice)

4.7/5 (34)

Refer to Figure 23.1. If the market price equaled $10, in the short run this firm should

Refer to Figure 23.1. If the market price equaled $10, in the short run this firm should

(Multiple Choice)

4.9/5 (33)

The equilibrium price of a good or service in a competitive market is

(Multiple Choice)

4.8/5 (43)

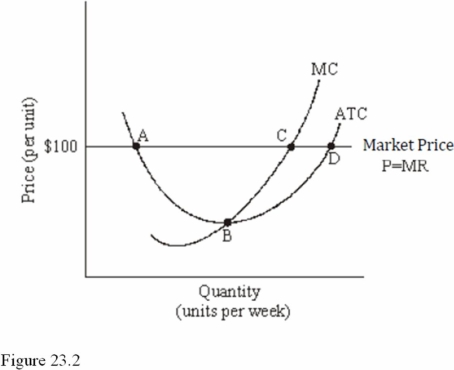

Refer to Figure 23.2 for a perfectly competitive firm. Given the current market price of $100, we expect to see

Refer to Figure 23.2 for a perfectly competitive firm. Given the current market price of $100, we expect to see

(Multiple Choice)

4.7/5 (43)

In a perfectly competitive market economy, business failures can benefit society by causing

(Multiple Choice)

4.7/5 (40)

When entrepreneurs decide to build a plant, they are making a production decision.

(True/False)

4.9/5 (33)

When economic losses exist in the cereal market, for example, this is an indication that

(Multiple Choice)

4.9/5 (24)

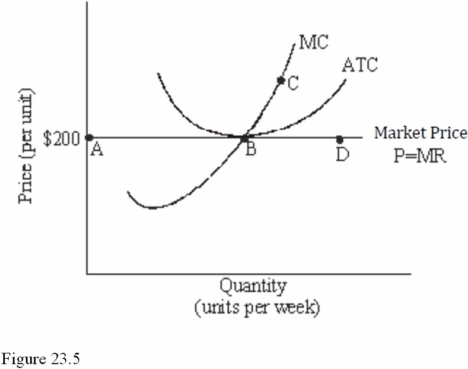

Refer to Figure 23.5 for a perfectly competitive firm. Which of the following is not true for this firm at a price of $200?

Refer to Figure 23.5 for a perfectly competitive firm. Which of the following is not true for this firm at a price of $200?

(Multiple Choice)

4.8/5 (35)

If price is above the long-run competitive equilibrium level,

(Multiple Choice)

4.7/5 (35)

Perfect information is a necessary condition of perfect competition.

(True/False)

4.8/5 (35)

If economic profits are earned in a competitive market, then over time

(Multiple Choice)

4.8/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)