Exam 14: Accounting Principles and Reporting Standards

Exam 1: Accounting: the Language of Business82 Questions

Exam 2: Analyzing Business Transactions93 Questions

Exam 3: Analyzing Business Transactions Using T Accounts107 Questions

Exam 4: The General Journal and the General Ledger85 Questions

Exam 5: Adjustments and the Worksheet76 Questions

Exam 6: Closing Entries and the Postclosing Trial Balance80 Questions

Exam 7: Accounting for Sales and Accounts Receivable76 Questions

Exam 8: Accounting for Purchases and Accounts Payable89 Questions

Exam 9: Cash Receipts, Cash Payments, and Banking Procedures88 Questions

Exam 10: Payroll Computations, Records, and Payment79 Questions

Exam 11: Payroll Taxes, Deposits, and Reports82 Questions

Exam 12: Accruals, Deferrals, and the Worksheet84 Questions

Exam 13: Financial Statements and Closing Procedures38 Questions

Exam 14: Accounting Principles and Reporting Standards67 Questions

Exam 15: Accounts Receivable and Uncollectible Accounts65 Questions

Exam 16: Notes Payable and Notes Receivable83 Questions

Exam 17: Merchandise Inventory91 Questions

Exam 18: Property, Plant, and Equipment118 Questions

Exam 19: Accounting for Partnerships106 Questions

Exam 20: Corporations: Formation and Capital Stock Transactions76 Questions

Exam 21: Corporate Earnings and Capital Transactions99 Questions

Exam 22: Long-Term Bonds105 Questions

Exam 23: Financial Statement Analyses107 Questions

Exam 24: The Statement of Cash Flows114 Questions

Exam 25: Departmentalized Profit and Cost Centers103 Questions

Exam 26: Accounting for Manufacturing Activities103 Questions

Exam 27: Job Order Cost Accounting102 Questions

Exam 28: Process Cost Accounting94 Questions

Exam 29: Controlling Manufacturing Costs: Standard Costs118 Questions

Exam 30: Cost-Revenue Analysis for Decision Making124 Questions

Select questions type

The basic financial reports of a business DO NOT provide users information about

(Multiple Choice)

4.8/5  (42)

(42)

Because financial statements must be objective and based on verifiable evidence,data obtained from estimates cannot be presented.

(True/False)

4.7/5 (46)

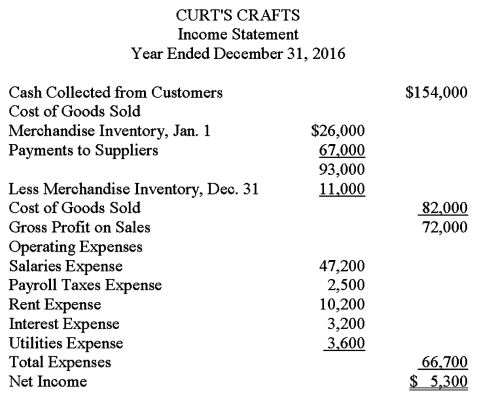

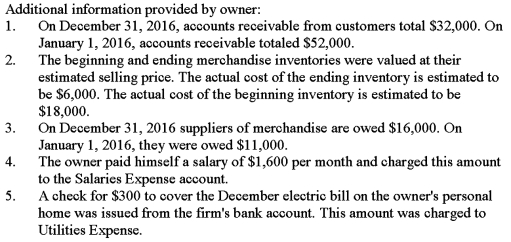

The income statement shown below was prepared and sent by Curtis Brown,the owner of Curt's Crafts,to several of his creditors.The business is a sole proprietorship that sells crafts and toys.An accountant for one of the creditors looked over the income statement and found that it did not conform to generally accepted accounting principles.Using the following additional information provided by the owner,prepare an income statement in accordance with generally accepted accounting principles.

(Essay)

4.9/5 (33)

The SEC's 2003 report to the Congress on "principles-based" accounting observed that the first characteristic of objectives-based standards,as dictated by the Sarbanes-Oxley Act,is that any standard must be based on

(Multiple Choice)

4.7/5 (42)

An accountant who records revenue when a credit sale is made rather than waiting for the receipt of cash from the customer is

(Multiple Choice)

4.7/5 (35)

When Tamar Snyder opened a shoe store,her accountant did not include the cash in her personal savings account as one of the assets of the business.This is an example of

(Multiple Choice)

4.7/5 (36)

Hour Place Clock Repair paid $2,400 cash in advance for a six month advertising contract with the local newspaper.According to the matching principle,if 2 months of the contract has expired by the end of the current fiscal year,how much should Hour Place Clock Repair report as Advertising Expense on the Income Statement?

(Multiple Choice)

4.8/5 (44)

Hour Place Clock Repair paid $1,800 cash in advance for a one year insurance policy.According to the matching principle,if 4 months of the policy has expired by the balance sheet date,how much should Hour Place Clock Repair report as Prepaid Insurance?

(Multiple Choice)

4.8/5 (37)

The matching principle is being applied when the cost of equipment is depreciated over its useful life.

(True/False)

4.8/5 (33)

Which of the following is allowed under generally accepted accounting principles?

(Multiple Choice)

4.8/5 (30)

The concept of realization permits a company to recognize income whenever there is an increase in the market value of the assets it holds.

(True/False)

4.8/5 (40)

The Statements of Financial Accounting Standards that automatically become generally accepted accounting principles are issued by

(Multiple Choice)

4.7/5 (38)

The ____________________ principle requires that if income is to be properly measured,all expired costs associated with the earning of revenue must be deducted from the revenue in the same accounting period.

(Essay)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)