Exam 8: Subsidiary Equity Transactions; Indirect and Mutual Holdings

Exam 1: Business Combinations: New Rules for a Long-Standing Business Practice32 Questions

Exam 2: Consolidated Statements: Date of Acquisition29 Questions

Exam 3: Consolidated Statements: Subsequent to Acquisition30 Questions

Exam 4: Intercompany Transactions: Merchandise, Plant Assets, and Notes29 Questions

Exam 5: Intercompany Transactions: Bonds and Leases54 Questions

Exam 6: Cash Flow, Eps, and Taxation44 Questions

Exam 7: Special Issues in Accounting for an Investment in a Subsidiary35 Questions

Exam 8: Subsidiary Equity Transactions; Indirect and Mutual Holdings36 Questions

Exam 9: The International Accounting Environment28 Questions

Exam 10: Foreign Currency Transactions61 Questions

Exam 11: Translation of Foreign Financial Statements62 Questions

Exam 12: Interim Reporting and Disclosures About Segments of an Enterprise50 Questions

Exam 13: Partnerships: Characteristics, Formation, and Accounting for Activities32 Questions

Exam 14: Partnerships: Ownership Changes and Liquidations48 Questions

Exam 15: Governmental Accounting: the General Fund and the Account Groups53 Questions

Exam 16: Governmental Accounting: Other Governmental Funds, Proprietary Funds, and Fiduciary Funds43 Questions

Exam 17: Financial Reporting Issues29 Questions

Exam 18: Accounting for Private Not-For-Profit Organizations45 Questions

Exam 19: Accounting for Not-For-Profit Colleges and Universities and Health Care Organizations64 Questions

Exam 20: Estates and Trusts: Their Nature and the Accountants Role46 Questions

Exam 21: Debt Restructuring, Corporate Reorganizations, and Liquidations44 Questions

Select questions type

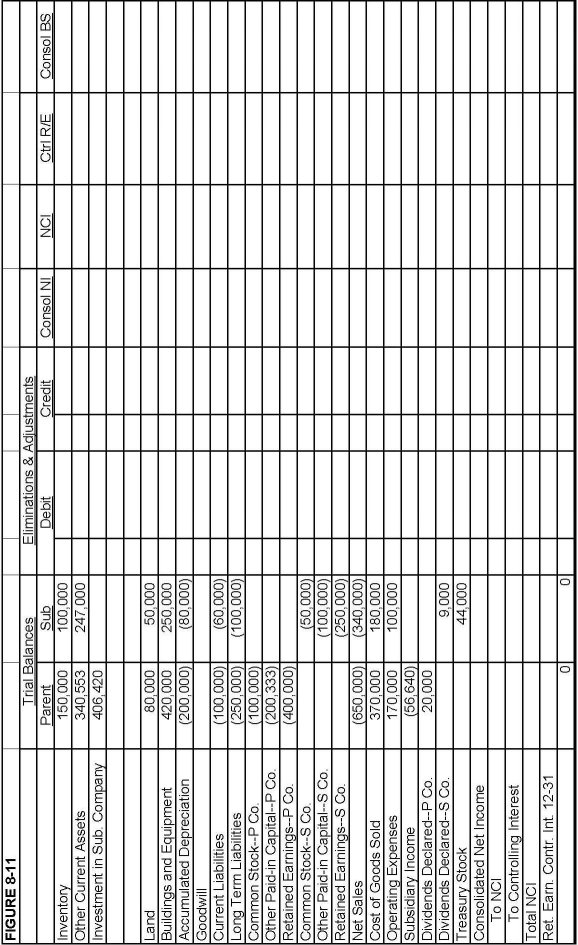

On January 1, 20X1, Parent Company purchased 85% of the common stock, 8,500 shares, of Subsidiary Company for $317,500. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill.

On January 1, 20X2, Subsidiary purchased, from its noncontrolling shareholders, 1,000 shares of its common stock, 10% of the stock outstanding on that date. The price paid was $44,000.

Required (round all amounts to whole dollars; round percentages to one decimal: XX.X%)

a.

Prepare an analysis to determine Parent's revised ownership interest following Sub's treasury stock transaction.

b.

Complete the Figure 8-11 worksheet for consolidated financial statements for 20X2

(Essay)

4.8/5  (36)

(36)

When a parent purchases a portion of the newly issued stock of its subsidiary in a private offering and the ownership interest decreases,

(Multiple Choice)

4.7/5 (41)

Porter & Solheim: On January 1, 20X1, Porter, Inc. paid $600,000 for its 75% interest in Solheim Company when Solheim had total equity of $550,000. Any excess of cost over book value was attributable to equipment with a 10-year life. Porter's investment in Solheim Company is recorded under the cost method.

Solheim had the following stockholders' equity on the dates shown:

1/1/1 1/1/3 1/1/4 Common stock \ 10 par \ 100,000 \ 100,000 \ 125,000 Other paid-in capital 200,000 200,000 375,000 Retained earnings 250,000 350,000 400,000

-Refer to Porter & Solheim. On January 2, 20X3, Solheim sold 2,500 additional shares of stock for $100 each in a private offering to noncontrolling shareholders. As a result of this issuance, the Porter's "Investment in Solheim" account should be adjusted by ____.

(Multiple Choice)

4.9/5 (38)

Paul & Stephan: On January 1, 20X1, Paul, Inc. acquired a 90% interest in Stephan Company. The $45,000 excess of purchase price (parent's share only) was attributable to goodwill. On January 1, 20X3, Stephan Company had the following stockholders' equity:

Common stock, \ 10 par \ 100,000 Other paid-in capital 200,000 Retained earnings 300,000 On January 2, 20X3, Stephan sold 2,000 additional shares in a private offering.

-Refer to Paul and Stephan. Stephan issued the new shares for $70 per share; Paul, Inc. purchased 600 of the shares. As a result of this sale, there is a(n)

(Multiple Choice)

4.7/5 (41)

Paris & Scott: On January 1, 20X1, Paris Ltd. paid $600,000 for its 75% interest in the Scott Company when Scott had total equity of $550,000. Any excess of cost over book value was attributed to equipment with a 10-year life. On January 1, 20X3, Scott Company had the following stockholders' equity:

Common stock, \ 10 par \ 100,000 Other paid-in capital 200,000 Retained earnings 350,000

-Refer to Paris & Scott. On January 2, 20X3, Scott Company sold 2,500 additional shares of stock for $60 each in a private offering to noncontrolling shareholders. As a result of this sale, which of the following changes would appear in the 20X3 consolidated statements?

(Multiple Choice)

4.9/5 (27)

Company P had 300,000 shares of common stock outstanding. It owned 80% of the outstanding common stock of S. S owned 20,000 shares of P common stock. In the consolidated balance sheet, Company P's outstanding common stock may be shown as

(Multiple Choice)

4.8/5 (39)

On January 1, 20X1, Parent Company purchased 85% of the common stock, 8,500 shares, of Subsidiary Company for $317,500. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill.

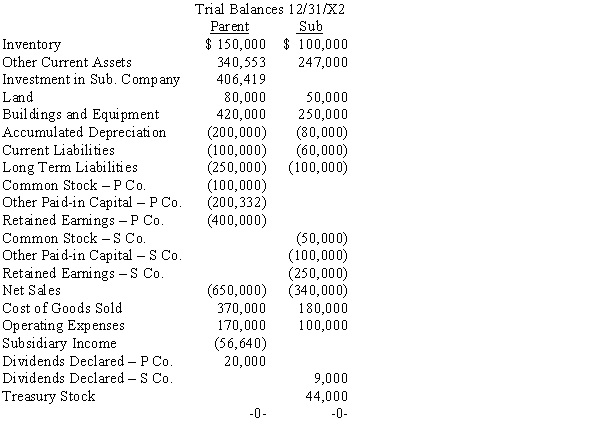

On January 1, 20X2, Subsidiary purchased, from its noncontrolling shareholders, 1,000 shares of its common stock, 10% of the stock outstanding on that date. The price paid was $44,000. The trial balances of Parent and Sub as of 12/31/X2 are given below:

Required (round all amounts to whole dollars; round percentages to one decimal: XX.X%)

a.

Prepare the D&D schedule for the 1/1/X1 acquisition.

b.

Prepare a schedule to determine the change in Parent's interest in Sub.

c.

Prepare all journal entries for Parent for the year ended 12/31/X2

d.

Prepare, in journal form, all elimination entries necessary for the 12/31/X2 consolidation worksheet.

Required (round all amounts to whole dollars; round percentages to one decimal: XX.X%)

a.

Prepare the D&D schedule for the 1/1/X1 acquisition.

b.

Prepare a schedule to determine the change in Parent's interest in Sub.

c.

Prepare all journal entries for Parent for the year ended 12/31/X2

d.

Prepare, in journal form, all elimination entries necessary for the 12/31/X2 consolidation worksheet.

(Essay)

5.0/5 (34)

On January 1, 20X1, Parent Company purchased 9,000 shares of the common stock of Subsidiary Company for $405,000. On this date, Subsidiary had 20,000 shares of $5 par common stock authorized, 10,000 shares issued and outstanding. Other paid-in capital and retained earnings were $150,000 and $200,000 respectively. On January 1, 20X1, any excess of cost over book value is due to a patent, to be amortized over 10 years.

Subsidiary's net income and dividends for two years were:

20X1 20X2 Net income \ 50,000 \ 80,000 Dividends 10,000 20,000 On January 1, 20X2, Subsidiary Company sold an additional 2,000 shares of common stock for $50 per share. Parent purchased 1,200 shares of the new issue, and noncontrolling shareholders purchased the other 800.

For both 20X1 and 20X2, Parent Company has applied the simple equity method.

Required:

a.

Prepare a schedule that measures Parent's change in interest ownership effective with Sub's issuance of the 2,000 shares and Parent's acquisition of 1,200 of those shares.

b.

Prepare Parent's journal entry to record its purchase of the 1,200 shares on 1/1/X2

c.

Prepare a schedule showing the 12/31/X2 balance of Parent's Investment in Sub account

(Essay)

5.0/5 (33)

Plum & Sterling: Plum Inc. acquired 90% of the capital stock of Sterling Co. on 1/1/X1 at a cost of $540,000. On this date Sterling had equipment (10-year life) carried at $200,000 under market and total equity amounting to $350,000.

On 1/1/X1 Sterling acquired 5% (10,000 shares) of Plum's outstanding common stock for $3 per share. Internally generated net income was $50,000 for Plum and $40,000 for Sterling.

-Refer to Plum and Sterling. The noncontrolling interest in consolidated net income is

(Multiple Choice)

4.8/5 (35)

When a parent purchases a portion of the newly issued stock of its subsidiary and the parent's percentage of ownership interest remains the same,

(Multiple Choice)

4.7/5 (40)

When a parent purchases a portion of the newly issued stock of its subsidiary and the ownership interest increases,

(Multiple Choice)

4.9/5 (41)

When the parent purchases some newly issued shares of a subsidiary, any adjustments resulting from the subsidiary stock sales should be made

(Multiple Choice)

4.7/5 (37)

Plum & Sterling: Plum Inc. acquired 90% of the capital stock of Sterling Co. on 1/1/X1 at a cost of $540,000. On this date Sterling had equipment (10-year life) carried at $200,000 under market and total equity amounting to $350,000.

On 1/1/X1 Sterling acquired 5% (10,000 shares) of Plum's outstanding common stock for $3 per share. Internally generated net income was $50,000 for Plum and $40,000 for Sterling.

-Refer to Plum and Sterling. Consolidated net income for 20X2 is

(Multiple Choice)

4.8/5 (31)

Paris & Scott: On January 1, 20X1, Paris Ltd. paid $600,000 for its 75% interest in the Scott Company when Scott had total equity of $550,000. Any excess of cost over book value was attributed to equipment with a 10-year life. On January 1, 20X3, Scott Company had the following stockholders' equity:

Common stock, \ 10 par \ 100,000 Other paid-in capital 200,000 Retained earnings 350,000

-Refer to Paris & Scott. On January 2, 20X3, Scott Company sold 2,500 additional shares of stock for $90 each in a private offering to noncontrolling shareholders. As a result of this sale, which of the following changes would appear in the 20X3 consolidated statements?

(Multiple Choice)

4.8/5 (30)

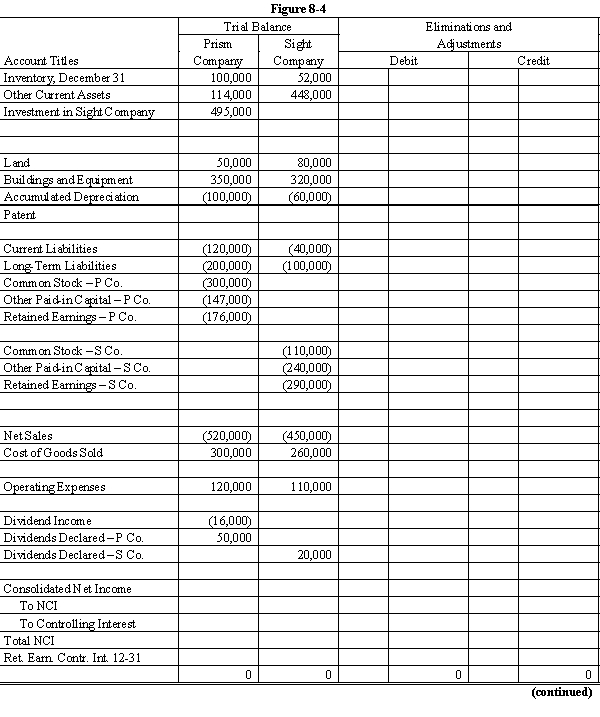

On January 1, 20X1, Prism Company purchased 7,500 shares of the common stock of Sight Company for $495,000. On this date, Sight had 20,000 shares of $10 par common stock authorized, 10,000 shares issued and outstanding. Other paid-in capital and retained earnings were $200,000 and $300,000 respectively. On January 1, 20X1, any excess of cost over book value is due to a patent, to be amortized over 15 years.

Sight's net income and dividends for two years were:

In November 20X1, Sight Company declared a 10% stock dividend at a time when the market price of its common stock was $50 per share. The stock dividend was distributed on December 31, 20X1.

For both 20X1 and 20X2, Prism Company has accounted for its investment in Sight using the cost method.

During 20X1, Sight Company sold goods to Prism Company for $40,000, of which $10,000 was on hand on December 31, 20X1. During 20X2, Sight sold goods to Prism for $60,000 of which $15,000 was on hand on December 31, 20X2. Sight's gross profit on intercompany sales is 40%.

Required:

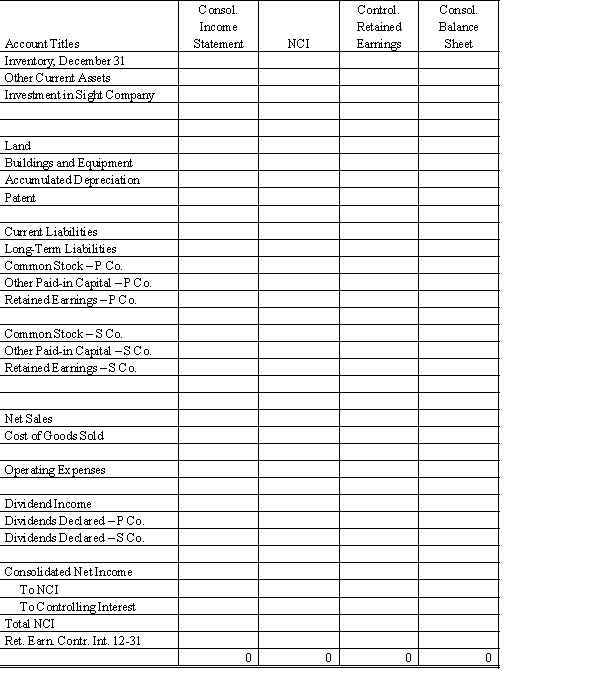

Complete the Figure 8-4 worksheet for consolidated financial statements for 20X2.

In November 20X1, Sight Company declared a 10% stock dividend at a time when the market price of its common stock was $50 per share. The stock dividend was distributed on December 31, 20X1.

For both 20X1 and 20X2, Prism Company has accounted for its investment in Sight using the cost method.

During 20X1, Sight Company sold goods to Prism Company for $40,000, of which $10,000 was on hand on December 31, 20X1. During 20X2, Sight sold goods to Prism for $60,000 of which $15,000 was on hand on December 31, 20X2. Sight's gross profit on intercompany sales is 40%.

Required:

Complete the Figure 8-4 worksheet for consolidated financial statements for 20X2.

(Essay)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)