Exam 7: Corporate Nonliquidating Distributions

Exam 1: Tax Research111 Questions

Exam 2: an Introduction to Taxation106 Questions

Exam 3: Corporate Formations and Capital Structure122 Questions

Exam 4: Determination of Tax144 Questions

Exam 5: The Corporate Income Tax126 Questions

Exam 6: Gross Income: Inclusions139 Questions

Exam 7: Corporate Nonliquidating Distributions112 Questions

Exam 8: Gross Income: Exclusions112 Questions

Exam 9: Other Corporate Tax Levies103 Questions

Exam 10: Property Transactions: Capital Gains and Losses141 Questions

Exam 11: Corporate Liquidating Distributions102 Questions

Exam 12: Deductions and Losses138 Questions

Exam 13: Corporate Acquisitions and Reorganizations100 Questions

Exam 14: Itemized Deductions122 Questions

Exam 15 Consolidated Tax Returns99 Questions

Exam 16: Losses and Bad Debts117 Questions

Exam 17: Partnership Formation and Operation115 Questions

Exam 18: Employee Expenses and Deferred Compensation147 Questions

Exam 19: Special Partnership Issues107 Questions

Exam 20: Depreciation,cost Recovery,amortization,and Depletion99 Questions

Exam 21: Corporations103 Questions

Exam 22: Accounting Periods and Methods114 Questions

Exam 23: The Gift Tax103 Questions

Exam 24: Property Transactions: Nontaxable Exchanges118 Questions

Exam 25: The Estate Tax107 Questions

Exam 26: Property Transactions: Section 1231 and Recapture109 Questions

Exam 27: Income Taxation of Trusts and Estates105 Questions

Exam 28: Special Tax Computation Methods,tax Credits,and Payment of Tax130 Questions

Exam 29: Administrative Procedures102 Questions

Select questions type

Strong Corporation is owned by a group of 20 shareholders.During the current year,Strong Corporation pays $225,000 in salary and bonuses to Stedman,its president and controlling shareholder.The IRS audits Strong's tax return and determines that reasonable compensation for Stedman would be $125,000.Strong Corporation agrees to the adjustment.

a)What effect does the disallowance of part of the deduction for Stedman's salary and bonuses have on Strong Corporation and Stedman?

b)What tax savings could have been obtained by Strong Corporation and Stedman if an agreement had been in effect that required Stedman to repay Strong Corporation any amounts determined by the IRS to be unreasonable?

(Essay)

5.0/5  (39)

(39)

Corporations may always use retained earnings as a substitute for earnings and profits.

(True/False)

4.9/5 (45)

Bruce receives 20 stock rights in a nontaxable distribution.The stock rights have an FMV of $5,000.The common stock with respect to which the rights are issued has a basis of $4,000 and an FMV of $120,000.Bruce allows the stock rights to lapse.He can deduct a loss of

(Multiple Choice)

4.9/5 (40)

Maple Corporation distributes land to a noncorporate shareholder.Explain how the following items are computed:

a)The amount of the distribution.

b)The amount of the dividend.

c)The basis of the land to the shareholder.

d)The start of the holding period for the land.

How would your answers change if the distribution was made to a corporate shareholder?

(Essay)

4.9/5 (39)

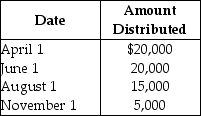

Payment Corporation has accumulated E&P of $19,000 and current E&P of $28,000.During the year,the corporation makes the following distributions to its sole shareholder:  The sole shareholder's basis in her stock is $45,000.What are the tax consequences of the June 1 distribution?

The sole shareholder's basis in her stock is $45,000.What are the tax consequences of the June 1 distribution?

(Essay)

4.8/5 (36)

An individual shareholder owns 3,000 shares of Baxter Corporation common stock with a basis of $10 per share.She receives a nontaxable 5% stock dividend.The basis per share of the common stock after the stock dividend is

(Multiple Choice)

4.9/5 (38)

Two corporations are considered to be brother-sister corporations for purposes of the Sec.304 redemption rules if one shareholder owns more than 50% of each corporation.

(True/False)

4.8/5 (48)

Circle Corporation has 1,000 shares of common stock outstanding.Circle redeems 450 shares owned by Dennis for $75,000 in complete redemption of Dennis's interest.The redemption qualifies as a sale.When the redemption is made,Circle Corporation has $150,000 of current and accumulated E&P and paid-in capital of $50,000.The distribution reduces paid-in capital by

(Multiple Choice)

4.8/5 (28)

Gould Corporation distributes land (a capital asset)worth $90,000 to Gerry,a shareholder.The land has a $30,000 basis to Gould.What is the amount and character of the gain or loss recognized by Gould?

(Essay)

4.8/5 (38)

Green Corporation is a calendar-year taxpayer.All of the stock is owned by Evan.His basis for the stock is $35,000.On March 1 (of a non-leap year),Green Corporation distributes $120,000 to Evan.Determine the tax consequences of the cash distribution to Evan in each of the following independent situations:

(Essay)

4.9/5 (30)

Digger Corporation has $50,000 of current and accumulated E&P.On March 1,Digger distributes land with a $30,000 FMV and a $17,500 adjusted basis to Dave,its sole shareholder.The land is subject to a $5,000 liability which Dave assumes.

a)What are the amount and character of the distribution?

b)What is Dave's basis in the property?

c)When does his holding period for the property begin?

(Essay)

4.9/5 (32)

Peter owns all 100 shares of Parker Corporation's stock.His basis in the stock is $30,000.Parker Corporation has $300,000 of E&P.Parker Corporation redeems 25 of Peter's shares for $90,000.What are the consequences to Peter and to Parker Corporation?

(Essay)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)