Exam 13: Property Transactions: Section 1231 and Recapture

Exam 1: An Introduction to Taxation106 Questions

Exam 2: Determination of Tax144 Questions

Exam 3: Gross Income: Inclusions139 Questions

Exam 4: Gross Income: Exclusions112 Questions

Exam 5: Property Transactions: Capital Gains and Losses141 Questions

Exam 6: Deductions and Losses138 Questions

Exam 7: Itemized Deductions122 Questions

Exam 8: Losses and Bad Debts118 Questions

Exam 9: Employee Expenses and Deferred Compensation147 Questions

Exam 10: Depreciation, Cost Recovery, Amortization, and Depletion99 Questions

Exam 11: Accounting Periods and Methods114 Questions

Exam 12: Property Transactions: Nontaxable Exchanges119 Questions

Exam 13: Property Transactions: Section 1231 and Recapture109 Questions

Exam 14: Special Tax Computation Methods, Tax Credits, and Payment of Tax130 Questions

Select questions type

If no gain is recognized in a nontaxable like-kind exchange involving Sec. 1245 or Sec. 1250 property, the recapture potential carries over to the replacement property.

(True/False)

4.8/5  (36)

(36)

Sec. 1231 property must satisfy a holding period of more than one year.

(True/False)

4.9/5 (35)

In 1980, Artima Corporation purchased an office building for $400,000 for use in its business. The building is sold during the current year for $550,000. Total depreciation allowed for the building was $350,000; straight-line would have been $320,000. As result of the sale, how much section 1231 gain will Artima Corporation report?

(Multiple Choice)

5.0/5 (42)

Gains and losses from involuntary conversions of property used in a trade or business generally are classified as capital gains and losses.

(True/False)

4.9/5 (32)

A taxpayer purchased a factory building in 1985 for $800,000. After claiming ACRS-accelerated depreciation of $800,000, she sells the asset for $1,000,000 during the current year. No payment is received during the current year, and the $1,000,000 balance to be paid with interest at the interest rate in four annual payments beginning one year from date of sale. The installment sales method is adopted. How much ordinary income is recognized in the current year?

(Multiple Choice)

4.8/5 (33)

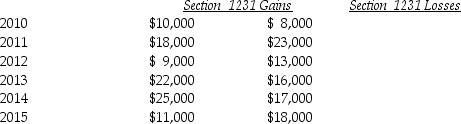

Lucy, a noncorporate taxpayer, experienced the following Section 1231 gains and losses during the years 2010 through 2015. Her first disposition of a Sec. 1231 asset occurred in 2010. Assuming Lucy had no capital gains and losses during that time period, what is the tax treatment in each of the years listed?

(Essay)

4.8/5 (33)

If the recognized losses resulting from involuntary conversions arising from casualty or theft exceed the recognized gains from such events (i.e. a net loss from the casualty), all of the involuntary conversions are treated as ordinary gains and losses.

(True/False)

4.9/5 (48)

Yelenis, whose tax rate is 28%, sells one Sec. 1231 asset this year, resulting in a $50,000 gain. Included in the $50,000 Sec. 1231 gain is $30,000 of unrecaptured Sec. 1250 gain. A review of Yelenis tax files for the past five years indicates one prior Sec. 1231 sale which resulted in a $14,000 loss. The gain will be taxed as

(Multiple Choice)

4.8/5 (41)

Sec. 1245 can increase the amount of gain recognized on an asset.

(True/False)

4.8/5 (41)

During the current year, George recognizes a $30,000 Section 1231 gain on sale of land and a $18,000 Section 1231 loss on the sale of land. Prior to this, George's only Section 1231 item was a $14,000 loss six years ago. George must report a

(Multiple Choice)

4.9/5 (42)

The following gains and losses pertain to Arnold's business assets that qualify as Sec. 1231 property. Arnold does not have any nonrecaptured net Sec. 1231 losses from previous years, and the portion of gain recaptured as ordinary income due to the depreciation recapture provisions has been eliminated.  Describe the specific tax treatment of each of these transactions.

Describe the specific tax treatment of each of these transactions.

(Essay)

4.9/5 (40)

Dinah owned land with a FMV of $130,000 (adjusted basis $120,000) which is investment property (a capital asset). Dinah owned a second tract of land, a 1231 asset, with a FMV of $46,000 (adjusted basis $50,000). Both tracts were acquired in 2001 and condemned by the state this year. The state paid an amount equal to FMV. If there are no other transactions involving capital assets or 1231 assets, Dinah must report on her current year return

(Multiple Choice)

4.9/5 (45)

Sarah owned land with a FMV of $150,000 (adjusted basis $135,000) which is investment property (a capital asset). Sarah owned a second tract of land, a 1231 asset, with a FMV of $38,000 (adjusted basis $55,000). Both tracts were acquired in 2000 and condemned by the state this year. The state paid an amount equal to FMV. If there are no other transactions involving capital assets or 1231 assets, what is the amount that Sarah must report on her current year return?

(Essay)

4.9/5 (40)

Gains and losses resulting from condemnations of Sec. 1231 property and capital assets held more than one year are classified as ordinary gains and losses.

(True/False)

4.9/5 (36)

Harry owns equipment ($50,000 basis and $38,000 FMV) and a building ($140,000 basis and $156,000 FMV), which are used in his business. Harry uses straight-line depreciation for both assets, which were acquired several years ago. Both the equipment and the building are destroyed in a fire, and Harry collects insurance proceeds equal to the assets' FMV. The tax result to Harry for this transaction is

(Multiple Choice)

4.7/5 (41)

Jaiyoun sells Sec. 1231 property this year, resulting in a $4,000 gain. This is the first time he has disposed of any Sec. 1231 property. Jaiyoun's tax rate is 10%. His tax on the Sec. 1231 gain will be

(Multiple Choice)

4.8/5 (45)

Trena LLC, a tax partnership owned equally by Trent and Nina, sells a building it had placed in service five years ago. Sec. 291 will require that part of the gain (up to 20% of accumulated depreciation) be treated as ordinary gain, with the balance treated as Sec. 1231 gain.

(True/False)

4.7/5 (38)

Unrecaptured 1250 gain is the amount of long-term capital gain which would be taxed as ordinary income if Sec. 1250 provided for the recapture of all depreciation and not just additional depreciation.

(True/False)

4.8/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)