Exam 9: Long-Run Costs and Output Decisions

Exam 1: The Scope and Method of Economics241 Questions

Exam 2: The Economic Problem: Scarcity and Choice218 Questions

Exam 3: Demand, Supply, and Market Equilibrium309 Questions

Exam 4: Demand and Supply Applications173 Questions

Exam 5: Elasticity188 Questions

Exam 6: Household Behavior and Consumer Choice272 Questions

Exam 7: The Production Process: the Behavior of Profit-Maximizing Firms287 Questions

Exam 8: Short-Run Costs and Output Decisions386 Questions

Exam 9: Long-Run Costs and Output Decisions363 Questions

Exam 10: Input Demand: the Labor and Land Markets200 Questions

Exam 11: Input Demand: the Capital Market and the Investment Decision218 Questions

Exam 12: General Equilibrium and the Efficiency of Perfect Competition202 Questions

Exam 13: Monopoly and Antitrust Policy394 Questions

Exam 14: Oligopoly219 Questions

Exam 15: Monopolistic Competition235 Questions

Exam 16: Externalities, Public Goods, and Common Resources275 Questions

Exam 17: Uncertainty and Asymmetric Information134 Questions

Exam 18: Income Distribution and Poverty197 Questions

Exam 19: Public Finance: the Economics of Taxation281 Questions

Exam 20: International Trade, Comparative Advantage, and Protectionism287 Questions

Exam 21: Economic Growth in Developing Economies133 Questions

Exam 22: Critical Thinking About Research104 Questions

Select questions type

If a perfectly competitive firm operates in the short run but exits the industry in the long run, then the firm's short run condition is

(Multiple Choice)

4.8/5  (37)

(37)

Industries in which firms are enjoying positive profits are likely to ________ in the long run.

(Multiple Choice)

4.8/5 (34)

A firm's long-run average cost curve represents the minimum cost of producing each level of output when the scale of production can be adjusted.

(True/False)

4.8/5 (28)

A perfectly competitive firm is breaking even. In the short run it should ________. In the long run it should ________.

(Multiple Choice)

4.8/5 (29)

Over all levels of output, if a firm's long-run average cost curve declines as output increases, then

(Multiple Choice)

4.9/5 (36)

Refer to Scenario 9.9 below to answer the question(s) that follow.

SCENARIO 9.9: Sponsors invest $250,000 in a new greeting card business on the promise that they will earn a return of 10% per year on their investment. The business sells 52,000 greeting cards per year. The fixed costs for the business include the return to investors and $79,000 in other fixed costs. Variable costs consist of wages ($1,000 per week) plus materials, electricity, etc. ($3,000 per week). The business is open 52 weeks per year.

-Refer to Scenario 9.9. The annual fixed costs for the business sum to

(Multiple Choice)

4.8/5 (32)

An industry is in ________ if firms have an incentive to enter or exit in the ________ run.

(Multiple Choice)

4.7/5 (32)

Assume the tennis ball industry, a perfectly competitive, decreasing‐cost industry, is in long-run equilibrium with a market price of $5. If the demand for tennis balls decreases, long-run equilibrium will be reestablished at a price

(Multiple Choice)

4.9/5 (34)

In the short run average costs eventually ________ because of diminishing returns, and in the long run average costs eventually ________ because of diseconomies of scale.

(Multiple Choice)

4.7/5 (33)

The long-run industry supply curve is made up of the zero-profit equilibrium levels of output as the industry expands due to entry of new firms.

(True/False)

4.9/5 (37)

For constant returns to scale, a(n) ________ in a firm's scale of production leads to ________ average total cost.

(Multiple Choice)

4.9/5 (33)

Diseconomies of scale cannot be due only to the sheer size of a firmʹs operation.

(True/False)

4.7/5 (32)

Refer to Scenario 9.7 below to answer the question(s) that follow.

SCENARIO 9.7: Julio borrowed $80,000 from his great aunt to open a coffee stand at a local flea market. He agrees to pay his great aunt a 5% yearly return on the money she lent him. His other yearly fixed costs equal $16,000. His variable costs equal $60,000. He sold 50,000 cups of coffee during the year at a price of $3.00 per cup.

-Refer to Scenario 9.7. Julio's profit is

(Multiple Choice)

4.8/5 (33)

For a perfectly competitive industry, an improvement in technology will cause

(Multiple Choice)

4.8/5 (38)

If, at the output where marginal revenue equals marginal cost, price is between average total cost and average variable cost, a firm will continue to produce in the short run.

(True/False)

4.8/5 (32)

In long-run equilibrium for a perfectly competitive industry, firms earn ________ economic profits and produce ________.

(Multiple Choice)

4.8/5 (37)

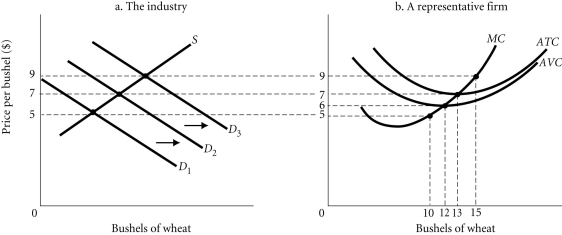

Refer to the information provided in Figure 9.2 below to answer the question(s) that follow.  Figure 9.2

-Refer to Figure 9.2. Suppose demand for wheat is initially D2. If the price of rice (a substitute for wheat) rises, then demand for wheat will shift to ________. This will ________ the equilibrium price of wheat and individual profit-maximizing firms will produce ________ bushels of wheat.

Figure 9.2

-Refer to Figure 9.2. Suppose demand for wheat is initially D2. If the price of rice (a substitute for wheat) rises, then demand for wheat will shift to ________. This will ________ the equilibrium price of wheat and individual profit-maximizing firms will produce ________ bushels of wheat.

(Multiple Choice)

4.8/5 (37)

In long-run equilibrium for a perfectly competitive industry, price equals

(Multiple Choice)

4.7/5 (31)

Refer to Scenario 9.6 below to answer the question(s) that follow.

SCENARIO 9.6: Celeste borrowed $40,000 from her brother to open a car wash. She pays her brother a 5% yearly return on the money he lent her. Her other yearly fixed costs equal $18,000. Her variable costs equal $40,000. In her first year, Amy sold 40,000 car washes at a price of $2.50 per car wash.

-Refer to Scenario 9.6. Celeste's total costs equal

(Multiple Choice)

4.7/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)