Exam 9: Long-Run Costs and Output Decisions

Exam 1: The Scope and Method of Economics241 Questions

Exam 2: The Economic Problem: Scarcity and Choice218 Questions

Exam 3: Demand, Supply, and Market Equilibrium309 Questions

Exam 4: Demand and Supply Applications173 Questions

Exam 5: Elasticity188 Questions

Exam 6: Household Behavior and Consumer Choice272 Questions

Exam 7: The Production Process: the Behavior of Profit-Maximizing Firms287 Questions

Exam 8: Short-Run Costs and Output Decisions386 Questions

Exam 9: Long-Run Costs and Output Decisions363 Questions

Exam 10: Input Demand: the Labor and Land Markets200 Questions

Exam 11: Input Demand: the Capital Market and the Investment Decision218 Questions

Exam 12: General Equilibrium and the Efficiency of Perfect Competition202 Questions

Exam 13: Monopoly and Antitrust Policy394 Questions

Exam 14: Oligopoly219 Questions

Exam 15: Monopolistic Competition235 Questions

Exam 16: Externalities, Public Goods, and Common Resources275 Questions

Exam 17: Uncertainty and Asymmetric Information134 Questions

Exam 18: Income Distribution and Poverty197 Questions

Exam 19: Public Finance: the Economics of Taxation281 Questions

Exam 20: International Trade, Comparative Advantage, and Protectionism287 Questions

Exam 21: Economic Growth in Developing Economies133 Questions

Exam 22: Critical Thinking About Research104 Questions

Select questions type

Refer to Scenario 9.4 below to answer the question(s) that follow.

SCENARIO 9.4: Sponsors invest $100,000 in a new deli on the promise that they will earn a return of 10% per year on their investment. The deli sells 52,000 sandwiches per year. The deli's fixed costs include the return to investors and $42,000 in other fixed costs. Variable costs consist of wages ($1,000 per week) plus materials, electricity, etc. ($2,000 per week). The deli is open 52 weeks per year.

-Refer to Scenario 9.4. What must the average price per sandwich be for the deli to earn a normal return?

(Multiple Choice)

4.7/5  (30)

(30)

The best explanation for ________ is a fixed factor causes diminishing returns to other factors.

(Multiple Choice)

4.8/5 (36)

An industry with a positive-sloping long-run supply curve is called a(n) ________ industry.

(Multiple Choice)

4.8/5 (34)

When a decrease in the scale of production leads to higher average costs, the industry exhibits

(Multiple Choice)

4.8/5 (38)

The Speedy Typesetting Company, a perfectly competitive firm, is currently producing where P = MC and is earning a normal profit. The yearly licensing fee that this firm must pay for the use of a statistical software program was just increased from $1,000 to $1,200. In the short run, this firm will most likely

(Multiple Choice)

4.9/5 (35)

Economies of scale are also referred to as increasing returns to scale.

(True/False)

4.8/5 (33)

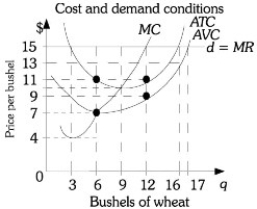

Refer to the information provided in Figure 9.1 below to answer the question(s) that follow.  Figure 9.1

-Refer to Figure 9.1. This farmer's fixed costs are

Figure 9.1

-Refer to Figure 9.1. This farmer's fixed costs are

(Multiple Choice)

4.8/5 (36)

Engineers for the Off Road Skateboard Company determine that a 12% increase in all inputs will cause a smaller percentage increase in output. Assuming that input prices remain constant, you correctly deduce that such a change in inputs will cause ________ as output increases.

(Multiple Choice)

4.8/5 (33)

Refer to Scenario 9.2 below to answer the question(s) that follow.

SCENARIO 9.2: Tom borrowed $40,000 from his parents to open a donut stand. He agrees to pay his parents a 5% yearly return on the money they lent him. His other yearly fixed costs equal $10,000. His variable costs equal $25,000. He sold 40,000 dozen donuts during the year at a price of $2.00 per dozen.

-Refer to Scenario 9.2. Tom's profit is

(Multiple Choice)

4.9/5 (36)

Refer to Scenario 9.6 below to answer the question(s) that follow.

SCENARIO 9.6: Celeste borrowed $40,000 from her brother to open a car wash. She pays her brother a 5% yearly return on the money he lent her. Her other yearly fixed costs equal $18,000. Her variable costs equal $40,000. In her first year, Amy sold 40,000 car washes at a price of $2.50 per car wash.

-Refer to Scenario 9.6. Celeste's total fixed costs equal

(Multiple Choice)

4.8/5 (36)

Which of the following is an example of diseconomies of scale?

(Multiple Choice)

4.7/5 (32)

Refer to Scenario 9.9 below to answer the question(s) that follow.

SCENARIO 9.9: Sponsors invest $250,000 in a new greeting card business on the promise that they will earn a return of 10% per year on their investment. The business sells 52,000 greeting cards per year. The fixed costs for the business include the return to investors and $79,000 in other fixed costs. Variable costs consist of wages ($1,000 per week) plus materials, electricity, etc. ($3,000 per week). The business is open 52 weeks per year.

-Refer to Scenario 9.9. The annual total costs for the business sum to

(Multiple Choice)

4.8/5 (32)

If price is above average total cost at the output where marginal revenue equals marginal cost, a firm will earn positive economic profits.

(True/False)

4.8/5 (35)

Assume a perfectly competitive industry is in long-run equilibrium at a price of $30. If this industry is an increasing-cost industry and the demand for the product increases, long-run equilibrium will be reestablished at a price

(Multiple Choice)

4.9/5 (29)

A firm must earn an economic profit in order to receive a normal rate of return.

(True/False)

4.8/5 (28)

When ________ scale of production leads to ________ average costs, an industry exhibits decreasing returns to scale.

(Multiple Choice)

4.7/5 (36)

If a perfectly competitive firm shuts down in the short run and exits the industry in the long run, the firm's short run condition is

(Multiple Choice)

4.7/5 (32)

The ________ for a perfectly competitive industry is the horizontal sum of the individual firmsʹ marginal cost curves above AVC.

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)