Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives

Exam 1: The Investment Setting78 Questions

Exam 2: The Asset Allocation Decision80 Questions

Exam 3: Selecting Investments in a Global Market80 Questions

Exam 4: Organization and Functioning of Securities Markets91 Questions

Exam 5: Security-Market Indexes84 Questions

Exam 6: Efficient Capital Markets90 Questions

Exam 7: An Introduction to Portfolio Management97 Questions

Exam 8: An Introduction to Asset Pricing Models119 Questions

Exam 9: Multifactor Models of Risk and Return59 Questions

Exam 10: Analysis of Financial Statements89 Questions

Exam 11: Introduction to Security Valuation86 Questions

Exam 12: Macroanalysis and Microvaluation of the Stock Market119 Questions

Exam 13: Industry Analysis90 Questions

Exam 14: Company Analysis and Stock Valuation133 Questions

Exam 15: Technical Analysis83 Questions

Exam 16: Equity Portfolio Management Strategies58 Questions

Exam 17: Bond Fundamentals89 Questions

Exam 18: The Analysis and Valuation of Bonds108 Questions

Exam 19: Bond Portfolio Management Strategies87 Questions

Exam 20: An Introduction to Derivative Markets and Securities108 Questions

Exam 21: Forward and Futures Contracts99 Questions

Exam 22: Option Contracts106 Questions

Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives87 Questions

Exam 24: Professional Money Management, Alternative Assets, and Industry Ethics102 Questions

Exam 25: Evaluation of Portfolio Performance96 Questions

Select questions type

If interest rates fall, an interest rate cap would expire unexercised.

Free

(True/False)

4.7/5  (42)

(42)

Correct Answer: Verified

Verified

True

Exhibit 23.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Exclusive Industries has debentures outstanding (par value $1,000.00) convertible into exclusive's common stock at $30. The coupon rate is 11% payable semiannually and they mature in 10 years.

-Refer to Exhibit 23.5. Calculate the conversion value if the stock price is $24.00 per share.

Free

(Multiple Choice)

4.8/5 (44)

Correct Answer:Verified

C

The conversion price parity for a convertible bond is defined as:

Free

(Multiple Choice)

4.7/5 (35)

Correct Answer:Verified

A

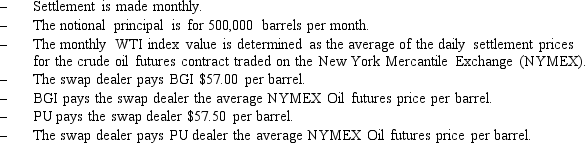

Exhibit 23.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Black Gold Industries (BGI) is an independent oil producer with production capacity of 500,000 barrels per month. Due to the cost structure of the business, BGI needs to receive $56.50 per barrel in order to remain solvent. On the other side of this situation is Petrochemicals Unlimited (PU) which uses an average of 500,000 barrels of West Texas crude oil in its normal production operations. The nature of PU's business is such that they will financially suffer if they have to pay more than an average of $57.80 per barrel for oil over the next six years. To hedge against their exposure to volatile oil prices, BI and PU contact a swap dealer to arrange the six-year oil swap described below:

-Refer to Exhibit 23.4. Describe the transaction that occurs between PU and the swap dealer if the monthly average oil futures settlement price is $55.50.

-Refer to Exhibit 23.4. Describe the transaction that occurs between PU and the swap dealer if the monthly average oil futures settlement price is $55.50.

(Multiple Choice)

4.9/5 (36)

Exhibit 23.10

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

TexMex Corporation has decided to borrow $50,000,000 for six months in two three-month issues. The corporation is concerned that interest rates will rise over the next three months. Thus, the corporation purchases a 3 * 6 FRA whereby the corporation pays the dealer's quoted fixed rate of 3.5% in exchange for receiving 3-month LIBOR at the settlement date. In order to hedge her exposure, the dealer buys LIBOR from Newport Inc. at its bid rate of 3%. The notional principal is $50,000,000 and that there are 60 days between month 3 and month 6.

-Refer to Exhibit 23.10. How much compensation does the dealer receive for transaction costs, credit risk and other costs associated with matching the FRA's?

(Multiple Choice)

4.7/5 (36)

Exhibit 23.8

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

An international investment firm buys an interest rate cap that pays the difference between LIBOR and 6% if LIBOR exceeds 6%. Current LIBOR is 5%. The amount of the option is $1,500,000, and the settlement is every 3 months. Assume a 360 day year.

-Refer to Exhibit 23.8. Find the payoff if LIBOR closes at 6.3%.

(Multiple Choice)

4.8/5 (29)

The payment of any compensation for loss is contingent on the actual occurrence of a credit-related event under a

(Multiple Choice)

4.9/5 (34)

Convertibles provide the upside potential of common stock and the downside protection of a bond.

(True/False)

4.9/5 (39)

A warrant is an option to buy a stated number of shares of common stock at a specified price at any time during the life of the warrant.

(True/False)

4.8/5 (37)

Exhibit 23.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Chimichango Industries has decided to borrow $50,000,000.00 for six months in two three-month issues. As the Treasurer, you are concerned that interest rates will rise over the next three months and the rate upon which the second payment will be based will be undesirable. (The amount of Chimichango's first payment will be known at origination.) To reduce the company's interest rate exposure, you decide to purchase a 3 * 6 FRA whereby you pay the dealer's quoted fixed rate of 5.91% in exchange for receiving 3-month LIBOR at the settlement date. In order to hedge her exposure, the dealer buys LIBOR from Megabuks Industries at its bid rate of 5.85%. (Assume a notional principal of $50,000,000.00 and that there are 60 days between month 3 and month 6.)

-Refer to Exhibit 23.3. Assuming that 3-month LIBOR is 5.6% on the rate determination day, and the contract specified settlement in arrears at month 6, describe the transaction that occurs between the dealer and Chimichango.

(Multiple Choice)

4.9/5 (48)

The intrinsic value of a warrant = (Market price of common stock + Warrant exercise price)* Number of shares specified by the warrant.

(True/False)

4.8/5 (33)

The following are all advantages of having an equity swap market except

(Multiple Choice)

4.9/5 (44)

Exhibit 23.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The Skalmory Corporation has entered into a 3-year interest rate swap, with semiannual settlement, to pay a fixed rate of 7.5% per year and receive 6-month LIBOR. The notional principal is $10,000,000.

-Refer to Exhibit 23.9. Assuming that one year after the swap was initiated the fixed rate on a new 2-year receive fixed pay floating LIBOR swap has fallen to 7% per year, calculate the market value of the 7.5% fixed rate bond based on $100 face value. Settlement is on a semiannual basis.

(Multiple Choice)

4.9/5 (38)

A plain vanilla swap agreement is used in similar situations as a forward rate agreement.

(True/False)

4.8/5 (35)

Which of the following is not a characteristic of warrants?

(Multiple Choice)

4.9/5 (36)

In convertible bonds, the value of the common stock price upon immediate conversion is the

(Multiple Choice)

4.8/5 (31)

Exhibit 23.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Chimichango Industries has decided to borrow $50,000,000.00 for six months in two three-month issues. As the Treasurer, you are concerned that interest rates will rise over the next three months and the rate upon which the second payment will be based will be undesirable. (The amount of Chimichango's first payment will be known at origination.) To reduce the company's interest rate exposure, you decide to purchase a 3 * 6 FRA whereby you pay the dealer's quoted fixed rate of 5.91% in exchange for receiving 3-month LIBOR at the settlement date. In order to hedge her exposure, the dealer buys LIBOR from Megabuks Industries at its bid rate of 5.85%. (Assume a notional principal of $50,000,000.00 and that there are 60 days between month 3 and month 6.)

-Refer to Exhibit 23.3. How much compensation does the dealer receive for transaction costs, credit risk and other costs associated with matching the FRA's?

(Multiple Choice)

4.8/5 (37)

Exhibit 23.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The Skalmory Corporation has entered into a 3-year interest rate swap, with semiannual settlement, to pay a fixed rate of 7.5% per year and receive 6-month LIBOR. The notional principal is $10,000,000.

-Refer to Exhibit 23.9. Assume that one year later the fixed rate on a new 2-year receive fixed pay floating LIBOR swap has fallen to 7% per year. Settlement is on a semiannual basis. Calculate the market value of the FRN based on $100 face value.

(Multiple Choice)

4.8/5 (34)

Exhibit 23.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The WallMal Company has entered into a 4-year interest rate swap, with semiannual settlement, to pay a fixed rate of 8% per year and receive 6-month LIBOR. The notional principal is $50,000,000.

-Refer to Exhibit 23.7. Indicate the market value of the swap to the WallMal Company.

(Multiple Choice)

4.8/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)