Exam 9: Multifactor Models of Risk and Return

Exam 1: The Investment Setting78 Questions

Exam 2: The Asset Allocation Decision80 Questions

Exam 3: Selecting Investments in a Global Market80 Questions

Exam 4: Organization and Functioning of Securities Markets91 Questions

Exam 5: Security-Market Indexes84 Questions

Exam 6: Efficient Capital Markets90 Questions

Exam 7: An Introduction to Portfolio Management97 Questions

Exam 8: An Introduction to Asset Pricing Models119 Questions

Exam 9: Multifactor Models of Risk and Return59 Questions

Exam 10: Analysis of Financial Statements89 Questions

Exam 11: Introduction to Security Valuation86 Questions

Exam 12: Macroanalysis and Microvaluation of the Stock Market119 Questions

Exam 13: Industry Analysis90 Questions

Exam 14: Company Analysis and Stock Valuation133 Questions

Exam 15: Technical Analysis83 Questions

Exam 16: Equity Portfolio Management Strategies58 Questions

Exam 17: Bond Fundamentals89 Questions

Exam 18: The Analysis and Valuation of Bonds108 Questions

Exam 19: Bond Portfolio Management Strategies87 Questions

Exam 20: An Introduction to Derivative Markets and Securities108 Questions

Exam 21: Forward and Futures Contracts99 Questions

Exam 22: Option Contracts106 Questions

Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives87 Questions

Exam 24: Professional Money Management, Alternative Assets, and Industry Ethics102 Questions

Exam 25: Evaluation of Portfolio Performance96 Questions

Select questions type

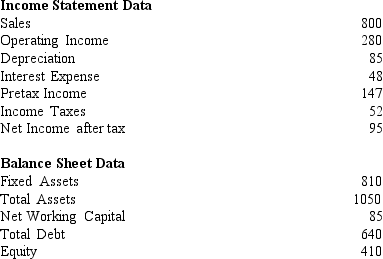

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-According to the APT model all securities should be priced such that riskless arbitrage is possible.

-According to the APT model all securities should be priced such that riskless arbitrage is possible.

Free

(True/False)

4.9/5  (40)

(40)

Correct Answer: Verified

Verified

False

A 1994 study by Burmeister, Roll, and Ross defined all of the following risk factors except

Free

(Multiple Choice)

4.9/5 (39)

Correct Answer:Verified

B

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-The January Effect is an anomaly where returns in January are significantly smaller than in any other month.

Free

(True/False)

5.0/5 (36)

Correct Answer:Verified

False

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The equation for the single-index market model is

-The equation for the single-index market model is

(Multiple Choice)

4.7/5 (36)

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-In one of their empirical tests of the APT, Roll and Ross examined the relationship between a security's returns and its own standard deviation. A finding of a statistically significant relationship would indicate that

(Multiple Choice)

4.8/5 (36)

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-Fama and French suggest a four factor model approach that explains many prior market anomalies.

(True/False)

4.8/5 (36)

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-To date, the results of empirical tests of the Arbitrage Pricing Model have been

(Multiple Choice)

4.8/5 (36)

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Assume that you are embarking on a test of the small-firm effect using APT. You form 10 size-based portfolios. The following finding would suggest there is evidence supporting APT:

(Multiple Choice)

4.8/5 (39)

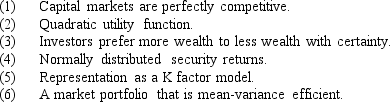

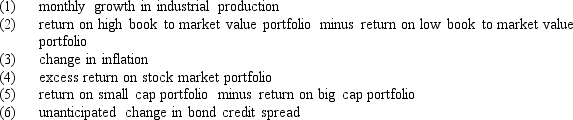

Consider the following list of risk factors:  Which of the following factors would you use to develop a microeconomic-based risk factor model?

Which of the following factors would you use to develop a microeconomic-based risk factor model?

(Multiple Choice)

4.7/5 (39)

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-Studies indicate that neither firm size nor the time interval used are important when computing beta.

(True/False)

4.8/5 (34)

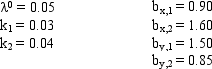

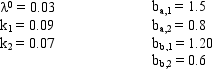

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. The expected prices one year from now for stocks X, Y, and Z are

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. The expected prices one year from now for stocks X, Y, and Z are

(Multiple Choice)

4.9/5 (41)

In a micro-economic (or characteristic) based risk factor model the following factor would be one of many appropriate factors:

(Multiple Choice)

4.8/5 (47)

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-In the APT model the idea of riskless arbitrage is to assemble a portfolio that

(Multiple Choice)

4.9/5 (38)

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-Empirical tests of the APT model have found that as the size of a portfolio increased so did the number of factors.

(True/False)

4.8/5 (38)

Under the following conditions, what are the expected returns for stocks X and Y?

(Multiple Choice)

4.9/5 (36)

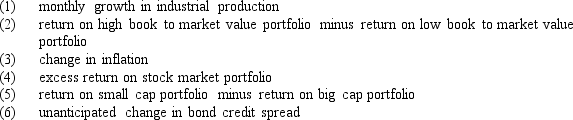

Consider the following list of risk factors:  Which of the following factors would you use to develop a macroeconomic-based risk factor model?

Which of the following factors would you use to develop a macroeconomic-based risk factor model?

(Multiple Choice)

4.9/5 (27)

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-The APT assumes that security returns are normally distributed.

(True/False)

5.0/5 (37)

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The excess return form of the single-index market model is

(Multiple Choice)

4.9/5 (39)

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. The expected returns for stock X, stock Y, and stock Z are

(Multiple Choice)

4.8/5 (36)

Under the following conditions, what are the expected returns for stocks A and B?

(Multiple Choice)

4.9/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)