Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues

Exam 19: Accounting for Estates and Trusts85 Questions

Exam 18: Accounting and Reporting for Private Not-For-Profit Organizations74 Questions

Exam 17: Accounting for State and Local Governments, Part II51 Questions

Exam 16: Accounting for State and Local Governments, Part I87 Questions

Exam 15: Partnerships: Termination and Liquidation73 Questions

Exam 14: Partnerships: Formation and Operation91 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations88 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission79 Questions

Exam 11: Worldwide Accounting Diversity and International Accounting Standards65 Questions

Exam 10: Translation of Foreign Currency Financial Statements101 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk108 Questions

Exam 8: Segment and Interim Reporting120 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income Taxes127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues119 Questions

Exam 5: Consolidated Financial Statements Intra-Entity Asset Transactions126 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership128 Questions

Exam 3: Consolidations - Subsequent to the Date of Acquisition123 Questions

Exam 2: Consolidation of Financial Information124 Questions

Exam 1: The Equity Method of Accounting for Investments123 Questions

Select questions type

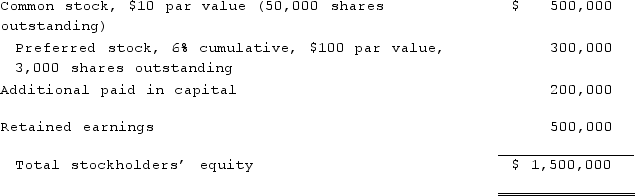

On January 1, 2021, Nichols Company acquired 80% of Smith Company's common stock and 40% of its non-voting, cumulative preferred stock. The consideration transferred by Nichols was $1,200,000 for the common and $124,000 for the preferred. There was no premium in the value of consideration transferred. Any excess acquisition-date fair value over book value is considered goodwill. The capital structure of Smith immediately prior to the acquisition is:  Compute the goodwill recognized in consolidation.

Compute the goodwill recognized in consolidation.

(Multiple Choice)

4.9/5  (32)

(32)

How do outstanding subsidiary stock warrants affect the calculation of consolidated earnings per share?

(Multiple Choice)

5.0/5 (28)

Wolff corporation owns 70% of the outstanding stock of Sanders, Inc. During the current year, Sanders made $75,000 in sales to Wolff. How does this transfer affect the consolidated statement of cash flows?

(Multiple Choice)

4.9/5 (38)

Where do dividends paid to the noncontrolling interest of a subsidiary appear on a consolidated statement of cash flows?

(Multiple Choice)

4.8/5 (45)

Which of the following characteristics is not indicative of an enterprise qualifying as a primary beneficiary with a controlling financial interest in a variable interest entity?

(Multiple Choice)

4.8/5 (31)

Webb Company purchased 90% of Jones Company for $990,000 when the book value of Jones was $1,000,000. There was no premium paid by Webb. Jones currently has 100,000 shares outstanding and a book value of $1,200,000.Assume Jones issues 20,000 new shares of its common stock to outside parties for $15 per share.After acquiring the additional shares, what adjustment is needed for Webb's investment in Jones account?

(Multiple Choice)

4.8/5 (35)

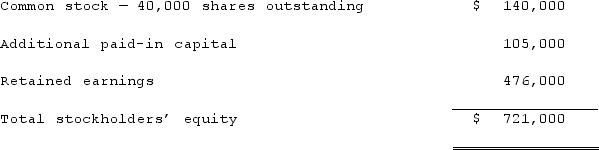

Popper Co. acquired 80% of the common stock of Cocker Co. on January 1, 2019, when Cocker had the following stockholders' equity accounts.  To acquire this interest in Cocker, Popper paid a total of $682,000 with any excess acquisition date fair value over book value being allocated to goodwill, which has been measured for impairment annually and has not been determined to be impaired as of January 1, 2022.Popper did not pay any premium when it acquired its original interest in Cocker. On January 1, 2022, Cocker reported a net book value of $1,113,000 before the following transactions were conducted. Popper uses the equity method to account for its investment in Cocker, thereby reflecting the change in book value of Cocker.On January 1, 2022, Cocker reacquired 8,000 of the outstanding shares of its own common stock for $34 per share. None of these shares belonged to Popper. How would this transaction have affected the additional paid-in capital of the parent company?

To acquire this interest in Cocker, Popper paid a total of $682,000 with any excess acquisition date fair value over book value being allocated to goodwill, which has been measured for impairment annually and has not been determined to be impaired as of January 1, 2022.Popper did not pay any premium when it acquired its original interest in Cocker. On January 1, 2022, Cocker reported a net book value of $1,113,000 before the following transactions were conducted. Popper uses the equity method to account for its investment in Cocker, thereby reflecting the change in book value of Cocker.On January 1, 2022, Cocker reacquired 8,000 of the outstanding shares of its own common stock for $34 per share. None of these shares belonged to Popper. How would this transaction have affected the additional paid-in capital of the parent company?

(Multiple Choice)

4.7/5 (27)

Webb Company purchased 90% of Jones Company for $990,000 when the book value of Jones was $1,000,000. Jones currently has 100,000 shares outstanding and a book value of $1,200,000.Jones sells 20,000 shares of previously unissued shares of its common stock to outside parties for $10 per share.What is the new percent ownership of Webb in Jones after the stock issuance?

(Multiple Choice)

4.7/5 (38)

Webb Company purchased 90% of Jones Company for $990,000 when the book value of Jones was $1,000,000. Jones currently has 100,000 shares outstanding and a book value of $1,200,000.Jones sells 20,000 shares of previously unissued shares of its common stock to outside parties for $10 per share.What is the adjusted book value of Jones after the sale of the shares?

(Multiple Choice)

4.8/5 (33)

A parent company owns a controlling interest in a subsidiary whose stock has a valuation basis of $27 per share. On the last day of the year, the subsidiary issues new shares entirely to outside parties at $25 per share. The parent still holds control over the subsidiary. Which of the following statements is true?

(Multiple Choice)

4.8/5 (40)

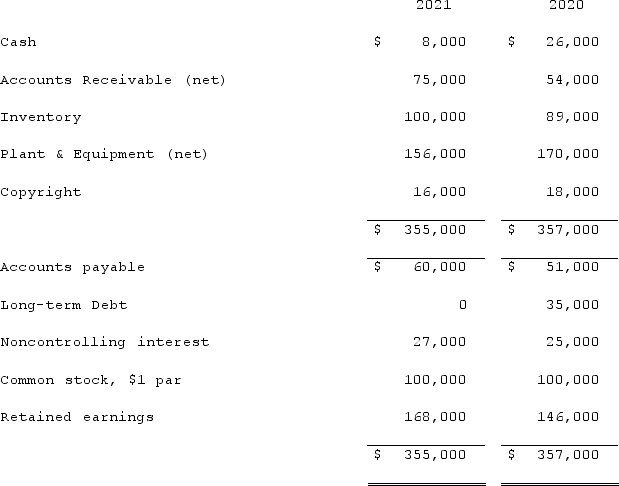

Anderson, Inc. has owned 70% of its subsidiary, Arthur Corp., for several years. The consolidated balance sheets of Anderson, Inc. and Arthur Corp. are presented below:  Additional information for 2021:The combination occurred using the equity method. Consolidated net income was $50,000. The noncontrolling interest share of consolidated net income of Arthur was $3,200.Arthur paid $4,000 in dividends.There were no purchases or disposals of plant & equipment or copyright this year.Net cash flow from operating activities was:

Additional information for 2021:The combination occurred using the equity method. Consolidated net income was $50,000. The noncontrolling interest share of consolidated net income of Arthur was $3,200.Arthur paid $4,000 in dividends.There were no purchases or disposals of plant & equipment or copyright this year.Net cash flow from operating activities was:

(Multiple Choice)

4.8/5 (36)

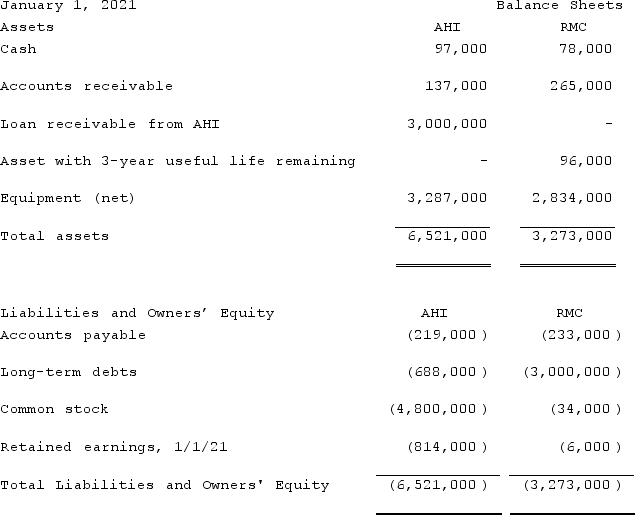

On January 1, 2021, A. Hamilton, Inc. ("AHI") provides a loan for $3,000,000 to Reynolds Manufacturing Corp. ("RMC"). The terms of the loan require payment of the loan no later than January 1, 2026. RMC was in terrible financial condition and would cease operations absent securing a loan. Prior to requesting a loan from AHI, RMC exhausted all other possible avenues for funding. The terms of the loan agreement include provisions that require RMC to provide AHI with the following from January 1, 2021 through January 1, 2026: (i) 6% annual interest on the principal amount of the loan, which reflects a market rate of interest; (ii) 100% participation rights to RMC's profits less $17,000 in a guaranteed annual dividend to RMC's common shareholders; and (iii) complete decision-making authority over RMC's operations and financing decisions.At the end of the term of the loan, AHI is given the right to acquire RMC or, in its discretion, extend the term of the original loan an additional 5 years. At the date the loan was extended to RMC, RMC's common stock had an estimated fair value of $136,000 and a book value of $40,000. The $96,000 difference was attributed to an asset with a 3-year useful life remaining ("Asset"). At January 1, 2021, the balance sheets for AHI and RMC are as follows:  With respect to the acquisition-date consolidation worksheet, which of the following is accurate?

With respect to the acquisition-date consolidation worksheet, which of the following is accurate?

(Multiple Choice)

4.8/5 (45)

Dayton, Inc. owns 80% of Haber Corp. The consolidated income statement for a year reports $60,000 Noncontrolling Interest in Haber Corp.'s Net Income. Haber paid dividends in the amount of $75,000 for the year. What are the effects of these transactions in the consolidated statement of cash flows for the year?

(Multiple Choice)

4.9/5 (30)

Where do dividends paid by a subsidiary to the parent company appear in a consolidated statement of cash flows?

(Multiple Choice)

4.8/5 (44)

Which of the following is not a potential loss or return of a variable interest entity?

(Multiple Choice)

4.8/5 (38)

During 2021, Parent Corporation purchased at carrying value some of the outstanding bonds of its subsidiary. How would this acquisition have been reflected in the consolidated statement of cash flows?

(Essay)

4.9/5 (40)

The following information has been taken from the consolidation worksheet of Graham Company and its 80% owned subsidiary, Stage Company.(1.) Graham reports a loss on sale of land (to an outside party) of $5,000. The land cost Graham $20,000.(2.) Noncontrolling interest in Stage's net income was $30,000.(3.) Graham paid dividends of $15,000.(4.) Stage paid dividends of $10,000.(5.) Excess acquisition-date fair value over book value amortization was $6,000.(6.) Consolidated accounts receivable decreased by $8,000.(7.) Consolidated accounts payable decreased by $7,000.How will dividends be reported in consolidated statement of cash flows?

(Multiple Choice)

4.9/5 (41)

Carlson, Inc. owns 80% of Madrid, Inc. Carlson reports net income for 2021 (without consideration of its investment in Madrid, Inc.) of $1,500,000. For the same year, Madrid reports net income of $705,000. Carlson had bonds payable outstanding on January 1, 2021 with a carrying value of $1,200,000. Madrid acquired the bonds on the open market on January 3, 2021 for $1,090,000. For the year 2021, Carlson reported interest expense on the bonds in the amount of $96,000, while Madrid reported interest income of $94,000 for the same bonds. Assuming there are no excess amortizations or other intra-entity transactions, what is Carlson's share of consolidated net income?

(Multiple Choice)

4.8/5 (37)

Which of the following statements is false concerning variable interest entities (VIEs)?

(Multiple Choice)

4.8/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)