Exam 10: Fundamentals of Cost Management

Exam 1: Cost Accounting: Information for Decision Making145 Questions

Exam 2: Cost Concepts and Behavior153 Questions

Exam 3: Fundamentals of Cost-Volume-Profit Analysis161 Questions

Exam 4: Fundamentals of Cost Analysis for Decision Making150 Questions

Exam 5: Cost Estimation131 Questions

Exam 6: Fundamentals of Product and Service Costing150 Questions

Exam 7: Job Costing159 Questions

Exam 8: Process Costing153 Questions

Exam 9: Activity-Based Costing153 Questions

Exam 10: Fundamentals of Cost Management144 Questions

Exam 11: Service Department and Joint Cost Allocation152 Questions

Exam 12: Fundamentals of Management Control Systems160 Questions

Exam 13: Planning and Budgeting157 Questions

Exam 14: Business Unit Performance Measurement147 Questions

Exam 15: Transfer Pricing147 Questions

Exam 16: Fundamentals of Variance Analysis156 Questions

Exam 17: Additional Topics in Variance Analysis138 Questions

Exam 18: Performance Measurement to Support Business Strategy148 Questions

Select questions type

Activity-based costing (ABC) information cannot be used by managerial decision-makers to evaluate the:

(Multiple Choice)

4.8/5  (34)

(34)

Glory Enterprises quality control report for August contains the following items:

Liability costs associated with defective products \1 0,000 Disposal costs of defective products failing inspection 20,000 Disposal costs of raw materials failing inspection 30,000 Quality training provided to workers 40,000 Lost sales due to poor quality and defective products 50,000 Advertising costs to offset perception of poor product quality 60,000 Raw materials used to correct defects before product was sold 70,000 Testing and inspecting a sample of finished goods 80,000

-

What would be the total of the internal failure costs on the August quality control report for Glory Enterprises?

(Multiple Choice)

4.8/5 (39)

Theoretical capacity is the amount of production possible assuming expected downtime for scheduled maintenance, normal breaks, and vacations.

(True/False)

4.8/5 (34)

Mobile Repair Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $125,000 for purchasing support should be assigned to the individual vendors from the information given as follows:

Vendor A Vendor B Vendor C Units purchased 100,000 200,000 200,000 Purchase orders (annual) 6 24 100 Number of shipments received 12 52 25

Required:

a. Allocate the purchasing costs to the three vendors, assuming Mobile Repair uses units purchased to compute activity-based costs.

b. Allocate the purchasing costs to the three vendors, assuming Mobile Repair uses purchases orders to compute activity-based costs.

c. Allocate the purchasing costs to the three vendors, assuming Mobile Repair uses number of shipments to compute activity-based costs.

(Essay)

4.9/5 (39)

McArthur Company has gathered the following data related to its production process of two of its products for the week ended April 30:

Model Item \#B200 Item \#C440 Quantity produced 60 100 Unit-related material costs \ 42,000 \ 100,000 Variable conversion costs 72,000 300,000 Total direct costs \ 114,000 \ 400,000 Indirect costs: Indirect manufacturing costs 163,200 272,000 Indirect operating costs 255,000 425,000 Total indirect costs 418,200 697,000 Total cost \ 532,200 \ 1,097,000

The costs above that appear to be allocated rather than traced are:

(Multiple Choice)

5.0/5 (35)

Water Industries' quality control report for August contains the following items:

Gathering, analysis, and reporting quality data \1 ,000 Inspecting raw materials received from vendors 2,000 Testing and inspecting finished products 3,000 Visiting customer sites to test product 4,000 Designing product to reduce production problems 5,000 Repairing and/or replacing products under warranty 6,000 Maintaining the equipment used to gather quality data 7,000 Cost (net) of materials wasted during production 8,000

-

What would be the total of the appraisal costs on the August quality control report for Water Industries?

(Multiple Choice)

4.8/5 (39)

Activity-based costing (ABC) techniques used to evaluate customer profitability can also be applied to evaluating suppliers.

(True/False)

4.8/5 (33)

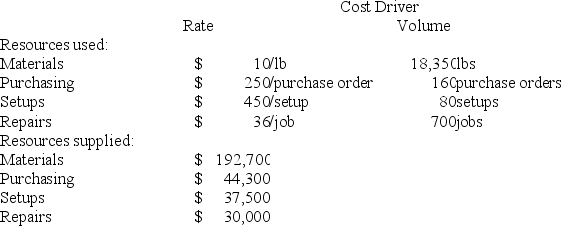

South Beach Industries reports the following information about resources. At the beginning of the year, South Beach estimated it would spend $180,000 for materials, $42,000 for purchasing, $35,000 for setups, and $36,000 for repairs.

-

The unused resource capacity for setups for South Beach is:

-

The unused resource capacity for setups for South Beach is:

(Multiple Choice)

4.8/5 (37)

Activity analysis is one of the first stages in implementing activity-based cost management (ABCM). Which of the following steps in activity analysis is usually performed first?

(Multiple Choice)

4.9/5 (34)

Identify each of the following as Prevention Activities (P), Appraisal Activities (A), Internal Failure Activities (I) or External Failure Activities (E):

(1) Field Testing

(2) Statistical process control

(3) Sampling at the end of process

(4) Disposing of scrap

(5) Quality evaluations

(6) Retesting

(7) Settling product liability

(8) Resolving customer complaints

(9) Lost sales

(10) Restoring reputation

(Essay)

4.9/5 (39)

Which of the following is not an example of an external failure cost?

(Multiple Choice)

4.9/5 (38)

Taylor's Cafe Supply Company delivers restaurant supplies throughout the city. Taylor's adds 4% to the order cost to cover the delivery cost. The delivery fee is meant to just cover the cost of delivery. A consultant has analyzed the delivery service using activity-based costing methods and identified four activities. Data on these activities are:

Activity Cost Driver Cost Driver Volume Process order number of orders \2 5,000 4,000 orders Load truck number of items 50,000 80,000 items Deliver merchandise number of orders 30,000 4,000 orders Process invoice number of invoices 24,000 6,000 invoice Total overhead \1 29,000

Two of Taylor's customers are City Diner and Le Chien Chaud. Below are data on orders and deliveries to these two customers:

City Diner Le Chien Chaud Order value \ 24,000 \ 32,000 Number of orders 50 100 Number of items 550 1,600 Number of invoices 12 120

Required:

(a) What would be the delivery charge for each customer under the current policy of 4% of order value?

(b) What would the activity-based costing system estimate as the cost of delivering to each customer?

(Essay)

4.8/5 (34)

The degree to which a good or service meets specifications is called:

(Multiple Choice)

4.8/5 (43)

Which of the following is a prevention activity in controlling quality?

(Multiple Choice)

4.9/5 (30)

Thompson Metal Corporation (TMC) supplies various types of machine tools to manufacturing companies. TMC has always paid a lot of attention to the quality of its products. Recently, an outside supplier has approached TMC to supply an important and intricate component of one of its more advanced tools that TMC has been manufacturing in-house. Sam Weiss, a junior accountant at TMC, has collected the following information regarding this proposal.

The cost of manufacturing one unit of this component internally are as follows:

Direct materials: \ 29.60 Direct labor: 13.00 Variable overhead: 19.50@150\% of direct labor cost) Fixed overhead: 26.00@200\% of direct labor cost) Total cost: \ 88.10

The outside supplier has quoted a price of $90 per unit for supplying this component. The following is a conversation that took place among the manufacturing manager (Dana Rice), buyer (Emily Scanlon), and Sam Weiss.

Weiss: I think that we should continue to manufacture internally because we can save $1.90 per unit on this component.

Rice: According to your report, we would save $1.90 per unit, but I do not agree with those numbers.

Weiss: What do you mean? I have followed the same costing guidelines this company has used for years. I have even cross-checked my numbers with historical data and know for sure that the overhead rates which I have used are correct.

Rice: I am sure you have done your job thoroughly, but I think that our costing system is archaic. This component is complex and difficult to manufacture. I believe that our overhead allocation method does not accurately capture the production difficulties and the additional resources that are devoted to the manufacture of this component. For example, a significant portion of our quality problems are due to this component. We spend close to a third of our quality inspection time on just this component alone, but that is not reflected. These quality problems cause delays in getting this component to the assembly department, and that causes a delay in getting the final product to the customers. Many of our customers are expecting just-in-time deliveries, and they get upset when we're late.

Scanlon: I know that the supplier that has approached us has a strong reputation for quality. Therefore, we can rest assured that we will have negligible quality problems.

Rice: Sam, your report does not consider this additional benefit from buying outside. I would appreciate if you can rework your numbers to better reflect the true costs associated with manufacturing this component internally.

Required:

(a) Assume the role of Sam Weiss. What are the different elements of costs that are likely to be associated with the manufacture of the component? Does the current costing system capture these costs?

(b) Recommend improvements in the costing system.

(c) How can Weiss quantify "qualitative" benefits such as quality and on-time delivery?

(Essay)

4.9/5 (44)

Benton Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $48,000 for purchasing support should be assigned to the individual vendors from the information given as follows:

Vendor A Vendor B Units purchased 100,000 200,000 Purchase orders (annual) 6 24 Number of shiprnents received 12 52

What is the amount of the purchasing costs that should be allocated to Vendor A, assuming Benton uses units purchased to compute activity-based costs?

(Multiple Choice)

4.8/5 (30)

Mirror Industries manufactures electric trolling motors. Sales for the month totaled $1,700,000. Information regarding resources for the month follows:

Resources Used Resources Supplied Administrative \ 100,000 \ 140,000 Customer service 20,000 40,000 Depreciation 120,000 200,000 Energy 100,000 100,000 Engineering 50,000 52,000 Long-term labor 50,000 70,000 Marketing 140,000 150,000 Materials 300,000 300,000 Parts management 60,000 70,000 Quality inspections 90,000 100,000 Setups 140,000 200,000 Temporary labor 40,000 48,000

Required:

a. Prepare a traditional income statement.

b. Prepare an activity-based income statement.

(Essay)

4.7/5 (33)

Morrison Supply provides the following information about resources:

Cost Driver Rate Cost Driver Volurne Resources used Adrninistrative \ 50 1,200 drniristrative hours Customer service 310 65 Energy 80 770 machine hours Long-tem labor 90 1,60 labor hours Materials 12 50,000 mits Purchasing 145 120 purchase orders Setups 450 115

Resources used Adrninistrative \6 8,000 Customer service 31,200 Energy 66,480 Long-tem labor 163,000 Materials 625,000 Purchasing 34,000 Setups 60,400

Required:

Compute the unused resource capacity for each preceding item.

(Essay)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)