Exam 10: Fundamentals of Cost Management

Exam 1: Cost Accounting: Information for Decision Making145 Questions

Exam 2: Cost Concepts and Behavior153 Questions

Exam 3: Fundamentals of Cost-Volume-Profit Analysis161 Questions

Exam 4: Fundamentals of Cost Analysis for Decision Making150 Questions

Exam 5: Cost Estimation131 Questions

Exam 6: Fundamentals of Product and Service Costing150 Questions

Exam 7: Job Costing159 Questions

Exam 8: Process Costing153 Questions

Exam 9: Activity-Based Costing153 Questions

Exam 10: Fundamentals of Cost Management144 Questions

Exam 11: Service Department and Joint Cost Allocation152 Questions

Exam 12: Fundamentals of Management Control Systems160 Questions

Exam 13: Planning and Budgeting157 Questions

Exam 14: Business Unit Performance Measurement147 Questions

Exam 15: Transfer Pricing147 Questions

Exam 16: Fundamentals of Variance Analysis156 Questions

Exam 17: Additional Topics in Variance Analysis138 Questions

Exam 18: Performance Measurement to Support Business Strategy148 Questions

Select questions type

Which of the following items would be classified as a product-related cost in an activity-based cost management (ABCM) system?

(Multiple Choice)

4.8/5  (33)

(33)

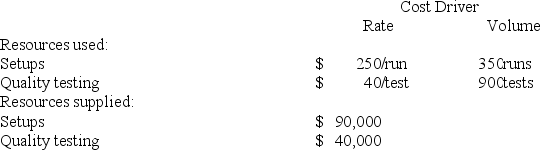

Denim Products reports the following information about resources. At the beginning of the year, Denim estimated it would spend $84,000 for setups and $41,000 for quality testing.

-

The unused resource capacity for setups for Denim Products is:

-

The unused resource capacity for setups for Denim Products is:

(Multiple Choice)

5.0/5 (31)

Water Industries' quality control report for August contains the following items:

Gathering, analysis, and reporting quality data \1 ,000 Inspecting raw materials received from vendors 2,000 Testing and inspecting finished products 3,000 Visiting customer sites to test product 4,000 Designing product to reduce production problems 5,000 Repairing and/or replacing products under warranty 6,000 Maintaining the equipment used to gather quality data 7,000 Cost (net) of materials wasted during production 8,000

-

What would be the total of the external failure costs on the August quality control report for Water Industries?

(Multiple Choice)

4.8/5 (36)

Fence Industries is preparing its annual profit plan. As part of its analysis of the profitability of its customers, management estimates that the $12,000 for sales support should be assigned to the individual customers from the information given as follows:

Customer A Customer B Units purchased 100,000 200,000 Purchase orders (annual) 5 20

-

What is the amount of the sales support costs that should be allocated to Customer B, assuming Fence uses units purchased to compute activity-based costs?

(Multiple Choice)

4.8/5 (37)

A company has high winter demand and low summer demand for its services. The cost of the unused summer capacity should be allocated:

(Multiple Choice)

4.8/5 (36)

Which of the following items would not be used as the cost driver for a volume-related cost in an activity-based cost management (ABCM) system?

(Multiple Choice)

4.9/5 (31)

Tabor Detective Services is evaluating its system. The company gathered the information below:

Process Available Hours per Week Value-Added Time (hours per client) Average Demand Interviews 70 2 20 Research 130 3 30 Pursuit 75 0.5 120 Travel 200 45 35

Practical capacity is 75% for each process.

Which process is most likely to be a current bottleneck?

(Multiple Choice)

4.9/5 (30)

Cost allocation bases are factors that cost management analysts use to assign indirect costs to cost objects. Ideally, cost-allocation bases should reflect a cause-and-effect relationship between resource spending and use. Ideally, an Activity-Based Costing (ABC) approach will provide a more accurate and useful accounting for an organization's resources. Recent studies have found that, in spite of increasing costs and diminishing resources, very few Higher Education Institutions use the tools and techniques of an ABC cost allocation system to assign costs to academic departments. While direct costs, such as faculty salaries, are traceable to individual academic departments or courses, many indirect costs, such as facility use, computer use, and student support services, are more difficult to assign. In a traditional approach, many higher education institutions assign such costs based on a single factor, such as the number of courses taught in the university. (Source: Activity-Based Costing for Higher Education Institutions, Management Accounting Quarterly, Winter, 2001)

Required:

(a) Explain why the use of a single-cost driver such as the number of courses may result in inaccurate management information as to the cost of offering courses in individual academic departments.

(b) For each of the indirect costs listed below, identify an appropriate cost-driver that might be used to allocate costs to determine the cost of offering a single course in an academic department if an Activity-Based-Costing model were used.

∙ Computer use

∙ Facility use

∙ Student services

∙ Course design

∙ Lecturing/class meeting time

∙ Assignment grading

(Essay)

4.8/5 (29)

Fence Industries is preparing its annual profit plan. As part of its analysis of the profitability of its customers, management estimates that the $12,000 for sales support should be assigned to the individual customers from the information given as follows:

Customer A Customer B Units purchased 100,000 200,000 Purchase orders (annual) 5 20

-

What is the amount of the sales support costs that should be allocated to Customer A, assuming Fence uses purchases orders to compute activity-based costs?

(Multiple Choice)

4.9/5 (39)

Smooth, Inc. manufactures bath and beauty products such as soaps, skin creams, lotions, and other products primarily for people with dry and sensitive skin. It has just introduced a new line of product that removes the spotting and wrinkling in skin associated with aging. It sells these products in pharmacies and department stores at prices slightly higher than those of other brands because of Smooth's excellent reputation for quality and effectiveness.

Smooth currently has very low utilization of plant capacity. Two years ago, in anticipation of rapid growth, the company opened a new large manufacturing plant, which has yet to be utilized more than 50 percent. Partly for this reason, Smooth has sought new partners and was able, with the help of financial analysts, to locate suitable business partners. The first potential partner identified in this search was a large supermarket chain, Price-Mart, which is interested in the partnership because it wants Smooth to manufacture an age cream to sell in its stores. The product would be essentially the same as the Smooth product but would be packaged in the Price-Mart brand name. The agreement would pay Smooth $2.00 per unit and would allow Price-Mart a limited right to advertise the product as manufactured for Price-Mart by Smooth. Smooth's CFO has made some calculations and has determined that the direct materials, direct labor, and other variable costs needed for the Price-Mart order would be about $1.00 per unit as compared to the full cost of $2.50 (materials, labor, and overhead) for the equivalent Smooth product.

Required:

Should Smooth Inc. accept the proposal from Price-Mart? Why or why not? (Include strategic considerations)

(Essay)

4.9/5 (43)

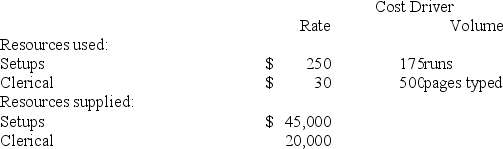

Macon Publishing reports the following information about resources. At the beginning of the year, Macon estimated it would spend $42,000 for setups and $21,000 for clerical.

-

The unused resource capacity for clerical for Macon Publishing is:

-

The unused resource capacity for clerical for Macon Publishing is:

(Multiple Choice)

4.8/5 (40)

Unused capacity costs incurred for the benefit of a company's customers (e.g., meet seasonal demands) should be assigned to the customers that require (use) the excess capacity.

(True/False)

4.7/5 (33)

Glory Enterprises quality control report for August contains the following items:

Liability costs associated with defective products \1 0,000 Disposal costs of defective products failing inspection 20,000 Disposal costs of raw materials failing inspection 30,000 Quality training provided to workers 40,000 Lost sales due to poor quality and defective products 50,000 Advertising costs to offset perception of poor product quality 60,000 Raw materials used to correct defects before product was sold 70,000 Testing and inspecting a sample of finished goods 80,000

-

What would be the total of the appraisal costs on the August quality control report for Glory Enterprises?

(Multiple Choice)

4.7/5 (23)

The unused resource capacity is the difference between the resources supplied and the resources:

(Multiple Choice)

4.7/5 (36)

Bison Creek Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $250,000 for purchasing support should be assigned to the individual vendors from the information given as follows:

Vendor A Vendor B Vendor C Units purchased 100,000 100,000 500,000 Purchase orders (annual) 12 24 50 Number of shipments received 12 52 100

Required:

a. Allocate the purchasing costs to the three vendors, assuming Bison Creek uses units purchased to compute activity-based costs.

b. Allocate the purchasing costs to the three vendors, assuming Bison Creek uses purchases orders to compute activity-based costs.

c. Allocate the purchasing costs to the three vendors, assuming Bison Creek uses number of shipments to compute activity-based costs.

(Essay)

4.8/5 (34)

Stella McDonald is a purchasing agent for a motorcycle manufacturer. Stella is evaluating two potential suppliers of seats for the company's motorcycles. One supplier (A) quotes a price of $165 per seat and assures 100% quality and delivery standards. The second supplier (B) quotes a price of $135 per seat but does not give any written assurances on quality or delivery. McDonald is not sure which supplier should be awarded the contract.

Assume you are the management accountant for the motorcycle manufacturer. McDonald asks you to prepare an estimate of the related costs of buying the seats from supplier B. She tells you that the estimate is needed because unless dollar estimates are attached to nonfinancial factors, such as lost production costs, her supervisor will not give it full attention. McDonald provides you with the following information:

∙ Production output is 2,000 motorcycles per year based on 250 production days a year.

∙ Production time per day is 8 hours at a cost of $4,000 per hour to run the production line.

∙ Lost production time due to poor quality is 1%.

∙ Satisfied customers purchase, on average, three motorcycles during a lifetime.

∙ Satisfied customers recommend the product, on average, to 5 other people.

∙ Marketing estimates that using the seat from supplier B will result in 5 lost customers per year from repeat business and referrals.

∙ Average contribution margin per motorcycle is $5,000.

Required:

Estimate the costs of buying motorcycle seats from supplier B. (Note: This problem requires you to think creatively and make reasonable estimates; therefore, there is more than one correct answer.)

(Essay)

4.7/5 (39)

Kingston Company produces precision components. Kingston has 11 customers, one of which accounts for 60 percent of the sales, with the remaining ten accounting for the rest of the sales. The ten smaller customers purchase components in roughly equal quantities. Orders placed by the smaller customers are about the same size. Data concerning Kingston's customer activity follow:

Ten Small Large Customer Customern Units purchased 300,000 200,000 Orders placed 12 420 Number of sales calls 20 230 Manufacturing cost \ 900,000 \ 600,000

Order-filling costs for Kingston Company total $360,000, and sales-force costs are $300,000.

Required:

a. Determine the profitability of each of the two classes of customers (large and small). Allocate the order-filling and sales force costs to the customers based on sales volume.

b. Determine the profitability of each of the two classes of customers (large and small). Allocate the order-filling and sales force costs to the customers using an activity-based costing approach.

(Essay)

5.0/5 (43)

Which of the following activities is most likely to be classified as value-added for a merchandise company?

(Multiple Choice)

4.7/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)