Exam 11: Service Department and Joint Cost Allocation

Clean-Burn, Inc. is a small petroleum company that acquires high-grade crude oil from low-volume production wells owned by individuals and small partnerships. The crude oil is processed in a single refinery into Two Oil, Six Oil, and impure distillates. Clean-Burn does not have the technology or capacity to process these products further and sell most of its output each month to major refineries. There were no inventories on November 1.

Crude o1l acquired and placed into production \ 5,000,000 Direct labor and related costs 2,000,000 Refinery overhead 3,000,000

Production and sales

Two Oil, 300,000 barrels produced; 280,000 barrels sold at $20 each.

Six Oil, 240,000 barrels produced; 220,000 barrels sold at $30 each.

Distillates, 120,000 barrels produced and sold at $15 per barrel.

Required:

a. Allocate the joint costs to the products using the physical quantities method.

b. Allocate the joint costs to the products using the net realizable value method.

a. Two Oil: $4,545,455; Six Oil: $3,636,364; Distillates: $1,818,181.

b. Two Oil: $4,000,000; Six Oil: $4,800,000; Distillates: $1,200,000.

Total joint cost: $5,000,000 + 2,000,000 + 3,000,000 = $10,000,000.

a.Two Oil: [300,000/(300,000 + 240,000 + 120,000)] × $10,000,000 = $4,545,455.

Six Oil: [240,000/(300,000 + 240,000 + 120,000)] × $10,000,000 = $3,636,364.

Distillates: [120,000/(300,000 + 240,000 + 120,000)] × $10,000,000 = $1,818,181.

b.Net realizable values: Two Oil: 300,000 × $20 = $6,000,000; Six Oil: 240,000 × $30 = $7,200,000; Distillates: 120,000 × $15 = $1,800,000; Total = $15,000,000.

Two Oil: ($6,000,000/$15,000,000) × $10,000,000 = $4,000,000.

Six Oil: ($7,200,000/$15,000,000) × $10,000,000 = $4,800,000.

Distillates: ($1,800,000/$15,000,000) × $10,000,000 = $1,200,000.

The following is a system of simultaneous linear equations to allocate costs using the reciprocal method. Matrix algebra is not required.

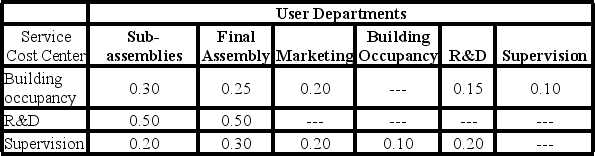

The following costs were incurred in three operating departments and three service departments in Westmoreland Company.

Department Direct Costs Label Subassemblies \ 550,000 P1 Final assembly 775,000 P2 Marketing 285,000 P3 Building occupancy 85,000 S 1 Research \& development 120,000 S2 Supervision 45,000 S 3

Use of services by other departments is as follows.

-

The equation for department S2 (research and development) is:

-

The equation for department S2 (research and development) is:

C

Criteria for selecting allocation bases for service department allocations should not include:

D

The Joplin Company conducts a simple chemical process in Department #1, which produces three separate items: A, K, and H. A is processed further in Department #2. K is processed further in Department #3. Product H is a by-product, to be accounted for by the other revenue method. The following information relates to September:

Department #1's costs $420,000.

Department #2's costs $150,000.

Department #3's costs $60,000.

A: 25,000 pounds completed; 23,500 pounds sold for $12 per pound.

K: 75,000 pounds completed; 70,000 pounds sold for $7.50 per pound.

H: 10,000 pounds completed; 10,000 pounds sold for $1.50 per pound. (There are shipping costs of $0.30 per pound.)

There were no beginning inventories.

Required:

Prepare a schedule to show the computation for the unit costs per pound for Products A, K, and H assuming Joplin uses the physical quantities method to allocate joint costs to the main products.

In a sell-or-process-further decision, (a) what are the relevant data to be considered and (b) what is the decision process associated with the split-off point?

In general, it is better to use a product's market value at the split-off point than its estimated net realizable value in allocating joint costs.

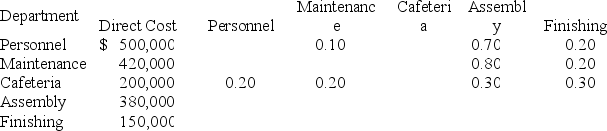

Mena Corporation has two production departments, Assembly and Finishing, and three service departments, Personnel, Maintenance, and Cafeteria. Data relevant to Mena are:

Assembly and Finishing worked on two jobs during the month: Jobs 100 and 101. Costs are allocated to jobs based on machine hours in Assembly and labor hours in Finishing. The machine and labor hours worked in each department are as follows:

Assembly Finishing Job 100 Labor Hours 200 Machine Hours 1,000 200 Job 101 Labor Hours 100 900 Machine Hours 500 100

Required:

Determine the amount of service department costs to be allocated to Jobs 100 and 101. Mena allocates service department costs to production departments using the direct method of allocation. (Round cost per hour to four decimal places and all other calculations to the nearest whole dollar.)

Assembly and Finishing worked on two jobs during the month: Jobs 100 and 101. Costs are allocated to jobs based on machine hours in Assembly and labor hours in Finishing. The machine and labor hours worked in each department are as follows:

Assembly Finishing Job 100 Labor Hours 200 Machine Hours 1,000 200 Job 101 Labor Hours 100 900 Machine Hours 500 100

Required:

Determine the amount of service department costs to be allocated to Jobs 100 and 101. Mena allocates service department costs to production departments using the direct method of allocation. (Round cost per hour to four decimal places and all other calculations to the nearest whole dollar.)

Yellville Regional Hospital is a small hospital with two service departments and three revenue areas:

Square Laundry Service Department Direct Costs Feet Pounds Housekeeping (HK) \ 80,000 - 16,000 Laundry \ 132,000 500 Revernue Areas: Surgery \ 400,000 1,500 48,000 Serniprivate roorns \ 200,000 2,000 24,000 Maternity \ 150,000 1,000 12,000

The hospital wants to allocate the service department costs to the revenue areas. Housekeeping is allocated based on square footage; Laundry is allocated based on pounds of laundry. The normal capacity for Surgery is 200 hours per month; normal capacity for semiprivate rooms is 600 patient days; and normal capacity for maternity is 200 patient days.

Required:

Determine the overhead rate for the three revenue areas. Allocate the service department costs to the revenue areas using the step method. Allocate the service department with the largest dollar value first.

The following information relates to Osceola Corporation for the past accounting period.

Direct costs Service Department A \ 80,000 Service Department B 60,000 Producing Department C 15,006 Producing Department D 20,000

Propartion of sernceby A to: 10\% 60\% 30\%

Proportion of service by B to: A 30\% C 20\% D 50\%

-

Using the reciprocal (simultaneous solution) method, Department B's cost allocated to Department C (rounded to the nearest whole dollar) is:

The physical quantities method allocates joint costs so that each joint product has the same gross margin as a percentage of sales.

Atkinson, Inc., manufactures products A, B, and C from a common process. Joint costs were $60,000. Additional information is as follows:

Units Sales Value at Split- Additional Product Produced Off Sales Value Costs A 6,000 40,000 55,000 \ 4,000 B 4,000 35,000 45,000 6,000 C 2,000 25.000 30.000 8,000 12,000 \ 100,000 \ 130,000 \ 18,000

-

Assuming that joint product costs are allocated using the net realizable value method, what were the total costs assigned to Product B?

Timberland Corporation produces three products from a joint process: One-X, Two-Y, and Three-Z. Each product can be processed further and sold for more. Data on the processes are as follows:

Product One-X Two-Y Three-Z Total Units produced 16,000 8,000 4,000 28,000 Joint costs \ 60,000 (a) (b) \ 120,000 Sales value at split-off (c) (d) \ 30,000 \ 200,000 Additional Processing Costs \ 14,000 \ 10,000 \ 6,000 \ 30,000 Sales value if Processed \ 140,000 \ 60,000 \ 40,000 \ 240,000

The amount of joint costs for One-X is the amount that has been allocated.

Required:

Determine the values for the lettered spaces. (CPA adapted)

Highlands, Inc. operates a sawmill facility. The company accounts for the sawdust that results from the primary sawing operation as a by-product. The sawdust is sold to another company at a price of $1.00 per hundred cubic feet. Normally, sales revenue from the sawdust is $21,200 per month. The sawdust is charged to inventory at $2.20 per hundred cubic feet, although there is no direct cost to process it.

As an alternative, Highlands can rent equipment that will process the dust into imitation logs for fireplaces. These logs sell for $25.00 per log to wholesalers, who package and add scent to them. 75 logs can be produced from 100 cubic feet of sawdust.

Cost of the equipment to produce these logs and the additional personnel required to operate the equipment are $360,000 per month, regardless of the output.

Required:

Should Highlands sell the sawdust for $1.00 per hundred cubic feet or process it into imitation logs? Support your answer with the appropriate calculations.

Penny's Pineapples is a pineapple grower. After cultivating, fertilizing, growing, and picking pineapples, the company sells whole pineapples to food processors. The company is considering adding a processing line where sliced pineapples and pineapple juice, along with a "mash" used for animal feed will be the final products. Projected information about the costs follows:

Separable Final selling price Product Units produced costs per unit Sliced pineapple 900,000 cans \ 600,000 \ 3.00 per can Pineapple juice 400,000 bottles \ 150,000 \ 1.75 per bottle Mash 500,000 pounds \ 120,000 \ 0.50 per pound

Joint product costs of cultivating, fertilizing and picking pineapples total $1,000,000.

Required:

(a) Determine the amount of joint costs allocated to each product using the net realizable value method.

(b) Determine the final cost per unit for each product.

(c) Determine the gross margin as a percent of sales for each product.

(d) A fertilizer manufacturer approaches Penny Martin, the President of the company, and asks to buy the rinds and other excess materials currently used to produce Mash. He would be willing to pay $0.30 per pound for these materials. What advice would you give Penny?

Which of the following is a weakness of the step method of service cost allocations?

Jack Donaldson owns and operates Jack's Abstracting Service. Jack's two revenue generating operations (Abstracting Services and Closing Services) are supported by two service departments: Clerical and Custodial. Costs in the service departments are allocated in the following order using the designated allocation bases.

Clerical: number of transactions processed.

Custodial: square footage of space occupied.

Average and expected activity levels for next month are as follows:

Numbers of Trarsactions Square Footage Expected Costs Abstract services 50 1,800 Closing services 25 2,200 Clerical 1,600 \4 0,000 Custodial 5 10,000

Required:

Use the direct method to allocate the service department costs to the revenue generating departments. Provide the total costs for the revenue departments.

Portofino Manufacturing Corporation manufactures three products in a joint process. Additional information is as follows:

Product Total Units produced 16,000 4,000 2,000 22,000 Sales value at split-off \ 300,000 \ 100,000 \ 20,000 \ 420,000 Additional costs if processed further \ 48,000 \ 20,000 \ 6,000 \ 74,000 Sales value if processed further \3 40,000 \1 60,000 \4 0,000 \4 50,000 Joint Costs \1 20,000

Required:

(a) Allocate the joint costs to the three products using the net realizable value method.

(b) Determine which products should be sold at split-off and which products should be processed further.

Which of the following is not a benefit of cost allocation?

Aardvark Industries has two production departments, Assembly and Finishing, and three Service Departments, Personnel, Maintenance, and Cafeteria. Data relevant to Aardvark are:

Required:

Allocate the service department costs of Aardvark Industries using the step method of cost allocation.

Required:

Allocate the service department costs of Aardvark Industries using the step method of cost allocation.

Jack Donaldson owns and operates Jack's Abstracting Service. Jack's two revenue generating operations Abstracting Services and Closing Services are supported by two service departments: Clerical and Custodial. Costs in the service departments are allocated in the following order using the designated allocation bases.

Clerical: number of transactions processed.

Custodial: square footage of space occupied.

Average and expected activity levels for next month are as follows:

Number of Tramsactions Square Footage Expected Costs Abstract services 50 1,800 Closing services 25 2,200 Clerical 1,600 \ 40,000 Custodial 5 10,000

Required:

a. Use the step method to allocate the service department costs to the revenue generating departments. Assume Clerical costs are allocated before Custodial costs and round all calculations to the nearest whole dollar. Provide the total costs for the revenue departments.

b. Use the step method to allocate the service department costs to the revenue generating departments but now assume Custodial costs are allocated before Clerical costs. Provide the total costs for the revenue departments.

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)