Exam 4: Fundamentals of Cost Analysis for Decision Making

Exam 1: Cost Accounting: Information for Decision Making145 Questions

Exam 2: Cost Concepts and Behavior153 Questions

Exam 3: Fundamentals of Cost-Volume-Profit Analysis161 Questions

Exam 4: Fundamentals of Cost Analysis for Decision Making150 Questions

Exam 5: Cost Estimation131 Questions

Exam 6: Fundamentals of Product and Service Costing150 Questions

Exam 7: Job Costing159 Questions

Exam 8: Process Costing153 Questions

Exam 9: Activity-Based Costing153 Questions

Exam 10: Fundamentals of Cost Management144 Questions

Exam 11: Service Department and Joint Cost Allocation152 Questions

Exam 12: Fundamentals of Management Control Systems160 Questions

Exam 13: Planning and Budgeting157 Questions

Exam 14: Business Unit Performance Measurement147 Questions

Exam 15: Transfer Pricing147 Questions

Exam 16: Fundamentals of Variance Analysis156 Questions

Exam 17: Additional Topics in Variance Analysis138 Questions

Exam 18: Performance Measurement to Support Business Strategy148 Questions

Select questions type

Lafferty Corporation is a specialty component manufacturer with idle capacity. Management would like to use its unused capacity to generate additional profits. A potential customer has offered to buy 6,200 units of component Rocket. Each unit of Rocket requires 8 units of material CES4 and 6 units of material XES7. Data concerning these two materials follow:

Units in Original Cost Current Market Price Per Disposal Value Per Material Stock Per Unit Unit Unit CES4 32,420 \ 3.80 \ 3.35 \ 3.10 XES7 31,060 \ 2.30 \ 9.60 \ 3.35

Material CES4 is in use in many of the company's products and is routinely replenished. Material XES7 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials, in total, for purposes of determining a minimum acceptable price for the order for product Rocket? (CIMA adapted)

(Multiple Choice)

4.7/5  (47)

(47)

The relevance of a particular cost to a decision is determined by the: (CMA adapted)

(Multiple Choice)

4.8/5 (34)

The Garrison Company manufactures two products: Oxy Cleaner and Sonic Cleaner. The costs and revenues are as follows:

Oxy Sonic Clearner Clearner Sales Price \ 75 \ 44 Variable cost per unit 40 21

Total demand for Oxy is 10,000 units and for Sonic is 6,000 units. Machine time is a scarce resource. During the year, 50,000 machine hours are available. Oxy requires 4 machine hours per unit, while Sonic requires 2.5 machine hours per unit.

-

What is the maximum contribution margin Garrison can achieve during a year?

(Multiple Choice)

4.9/5 (39)

Which of the following statements regarding special orders is (are) false?

(A) The primary decision for special orders is determining whether the differential revenue is greater than the differential costs associated with the order.

(B) The differential analysis approach to pricing for special orders will always lead to underpricing in the long-run because fixed costs are not included in the analysis.

(Multiple Choice)

4.9/5 (36)

The operations of Winston Corporation are divided into the Blink Division and the Blur Division. Projections for the next year are as follows:

-

If the Blur Division were dropped, Blink Division's sales would increase by 30%. If this happened, the operating income for Winston Corporation as a whole would be:

(Multiple Choice)

4.7/5 (39)

The following information relates to a product produced by Faulkland Company:

Direct materials \ 10 Direct labor 7 Variable overhead 6 Fixed overhead Unit cost

Fixed selling costs are $1,000,000 per year. Variable selling costs of $4 per unit sold are added to cover the transportation cost. Although production capacity is 500,000 units per year, Faulkland expects to produce only 400,000 units next year. The product normally sells for $40 each. A customer has offered to buy 60,000 units for $30 each. The customer will pay the transportation company directly for the transportation charges on the units purchased. If Faulkland accepts the special order, the effect on operating profits would be a:

(Multiple Choice)

4.8/5 (34)

Park Corporation is preparing a bid for a special order that would require 720 liters of material SUN100. The company already has 560 liters of this raw material in stock that originally cost $6.30 per liter. Material SUN100 is used in the company's main product and is replenished on a periodic basis. The resale value of the existing stock of the material is $5.80 per liter. New stocks of the material can be readily purchased for $6.65 per liter. What is the relevant cost of the 720 liters of the raw material when deciding how much to bid on the special order? (CIMA adapted)

(Multiple Choice)

4.8/5 (37)

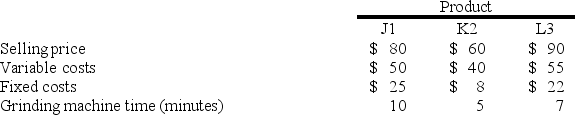

Atuso, Inc. produces three products. Data concerning the selling prices and unit costs of the three products appear below:

Fixed costs are applied to the products on the basis of direct labor hours.

Demand for the three products exceeds the company's productive capacity. The grinding machine is the constraint, with only 2,400 minutes of grinding machine time available this week.

Required:

a. Given the grinding machine constraint, which product should be emphasized? Support your answer with appropriate calculations.

b. Assuming that there is still unfilled demand for the product that the company should emphasize in part (a) above, up to how much should the company be willing to pay for an additional hour of grinding machine time?

Fixed costs are applied to the products on the basis of direct labor hours.

Demand for the three products exceeds the company's productive capacity. The grinding machine is the constraint, with only 2,400 minutes of grinding machine time available this week.

Required:

a. Given the grinding machine constraint, which product should be emphasized? Support your answer with appropriate calculations.

b. Assuming that there is still unfilled demand for the product that the company should emphasize in part (a) above, up to how much should the company be willing to pay for an additional hour of grinding machine time?

(Essay)

4.7/5 (29)

Explain the distinction between predatory pricing and peak-load pricing.

(Essay)

4.9/5 (41)

Damon Industries manufactures 20,000 components per year. The manufacturing costs of the components was determined as follows:

Direct materials \ 100,000 Direct labor 160,000 Variable manufacturing overhead 60,000 Fixed manufacturing overhead 80,000

An outside supplier has offered to sell the component for $17. If Damon purchases the component from the outside supplier, the manufacturing facilities would be unused and could be rented out for $10,000. If Damon purchases the component from the supplier instead of manufacturing it, the effect on operating profits would be a:

(Multiple Choice)

4.8/5 (34)

The operations of Bridgeton Corporation are divided into the Adams Division and the Carter Division. Projections for the next year are as follows:

Operating income for Bridgeton Corporation as a whole if the Carter Division were dropped would be:

(Multiple Choice)

4.8/5 (33)

Barry Inc. makes a range of products. The company's predetermined overhead rate is $14 per direct labor-hour, which was calculated using the following budgeted data:

Variable manufacturing overhead \1 00,000 Fixed manufacturing overhead \2 50,000 Direct labor-hour's 25,000

Component ZZ9 is used in one of the company's products. The unit cost of the component according to the company's cost accounting system is determined as follows:

Direct materials \ 28.00 Direct labor 56.00 Manufacturing overhead applied 39.20 Unit product cost \ 123.20

An outside supplier has offered to supply component ZZ9 for $108 each. The outside supplier is known for quality and reliability. Assume that direct labor is a variable cost, variable manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing overhead would not be affected by this decision. Barry chronically has idle capacity. (CIMA adapted)

Required:

Is the offer from the outside supplier financially attractive? Why?

(Essay)

4.8/5 (34)

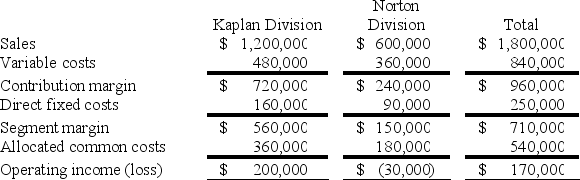

The operations of Balance Corporation are divided into the Kaplan Division and the Norton Division. Projections for the next year are as follows:

Required:

a. Operating income for Balance Corporation, as a whole, if the Norton Division were dropped would be:

b. If the Norton Division were dropped, Kaplan Division's sales would increase by 45%. If this happened, the operating income for Balance Corporation as a whole would be:

Required:

a. Operating income for Balance Corporation, as a whole, if the Norton Division were dropped would be:

b. If the Norton Division were dropped, Kaplan Division's sales would increase by 45%. If this happened, the operating income for Balance Corporation as a whole would be:

(Essay)

4.9/5 (39)

Price Candies (PC) makes three types of chocolate candy bars. The head of marketing, Nathan Lord found the chart below and believes PC should drop the Almond line. He asks controller, Faye Martin, to review the situation and determine the fate of the Almond Line.

Required:

a. Review the information above and determine the fate of the Almond Line. Prepare your answer in good form. Note: Facility and product level costs are fixed and will not change; they are allocated based upon sales.

b. Prepare a memo defending your position on this important issue.

Required:

a. Review the information above and determine the fate of the Almond Line. Prepare your answer in good form. Note: Facility and product level costs are fixed and will not change; they are allocated based upon sales.

b. Prepare a memo defending your position on this important issue.

(Essay)

4.9/5 (37)

Which of the following statements about the theory of constraints is (are) true?

(A) The theory of constraints focuses on determining the optimal product mix when one or more resources restrict the attainment of a goal or objective.

(B) The theory of constraints focuses on the rate of throughput contribution and minimizing investment and other operating costs.

(Multiple Choice)

4.8/5 (42)

Financial statements prepared in accordance with generally accepted accounting principles (GAAP) provide differential cost information.

(True/False)

4.9/5 (42)

Bacon Company makes four products in a single facility. These products have the following unit product costs:

A B C D Direct materials \ 14.30 \ 10.20 \ 11.00 \ 10.60 Direct labor 19.40 27.40 33.60 40.40 Variable manufacturing 4.30 2.70 2.60 3.20 overhead Fixed manufacturing 26.50 34.80 26.60 37.20 overhead Unit product cost \6 4.50 \7 5.10 \7 3.80 \9 1.40

Additional data concerning these products are listed below.

A B C D Grinding minutes per unit 3.80 5.30 4.30 3.40 Selling price per unit \ 76.10 \ 93.50 \ 87.40 \ 104.20 Variable selling cost per \ 2.20 \ 1.20 \ 3.30 \ 1.60 unit Monthly demand in units 2,000 4,000 3,000 2,000

The grinding machines are the constraint in the production facility. A total of 53,600 minutes is available per month on these machines.

Direct labor is a variable cost in this company.

-

How many minutes of grinding machine time would be required to satisfy demand for all four products?

(Multiple Choice)

4.8/5 (35)

Starla Corporation is a specialty component manufacturer with idle capacity. Management would like to use its extra capacity to generate additional profits. A potential customer has offered to buy 4,200 units of component JOLT. Each unit of JOLT requires 6 units of material OX8 and 9 units of material POW6. Data concerning these two materials follow:

Units in Original Cost Current Market Price Per Disposal Value Per Material Stock Per Unit Unit Unit OX8 18,600 PoW6 1.65

Material OX8 is in use in many of the company's products and is routinely replenished. Material POW6 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials, in total, for purposes of determining a minimum acceptable price for the order for product JOLT? (CIMA adapted)

(Multiple Choice)

4.8/5 (32)

Explain what is meant by "the full-cost fallacy" in making pricing decisions.

(Essay)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)