Exam 4: Fundamentals of Cost Analysis for Decision Making

Exam 1: Cost Accounting: Information for Decision Making145 Questions

Exam 2: Cost Concepts and Behavior153 Questions

Exam 3: Fundamentals of Cost-Volume-Profit Analysis161 Questions

Exam 4: Fundamentals of Cost Analysis for Decision Making150 Questions

Exam 5: Cost Estimation131 Questions

Exam 6: Fundamentals of Product and Service Costing150 Questions

Exam 7: Job Costing159 Questions

Exam 8: Process Costing153 Questions

Exam 9: Activity-Based Costing153 Questions

Exam 10: Fundamentals of Cost Management144 Questions

Exam 11: Service Department and Joint Cost Allocation152 Questions

Exam 12: Fundamentals of Management Control Systems160 Questions

Exam 13: Planning and Budgeting157 Questions

Exam 14: Business Unit Performance Measurement147 Questions

Exam 15: Transfer Pricing147 Questions

Exam 16: Fundamentals of Variance Analysis156 Questions

Exam 17: Additional Topics in Variance Analysis138 Questions

Exam 18: Performance Measurement to Support Business Strategy148 Questions

Select questions type

The theory of constraints focuses on determining the optimal product mix when one or more resources restrict the attainment of a goal or objective.

(True/False)

4.7/5  (38)

(38)

Bacon Company makes four products in a single facility. These products have the following unit product costs:

A B C D Direct materials \ 14.30 \ 10.20 \ 11.00 \ 10.60 Direct labor 19.40 27.40 33.60 40.40 Variable manufacturing 4.30 2.70 2.60 3.20 overhead Fixed manufacturing 26.50 34.80 26.60 37.20 overhead Unit product cost \ 64.50 \ 75.10 \ 73.80 \ 91.40

Additional data concerning these products are listed below.

A B C D Grinding minutes per unit 3.80 5.30 4.30 3.40 Selling price per unit \ 76.10 \ 93.50 \ 87.40 \ 104.20 Variable selling cost per \ 2.20 \ 1.20 \ 3.30 \ 1.60 unit Monthly demand in units 4,000 4,000 3,000 2,000

The grinding machines are the constraint in the production facility. A total of 53,600 minutes is available per month on these machines.

Direct labor is a variable cost in this company.

-

Which product makes the MOST profitable use of the grinding machines?

(Multiple Choice)

4.8/5 (39)

Which of the following costs are not considered in a differential analysis for a make-or-buy decision?

(Multiple Choice)

4.7/5 (37)

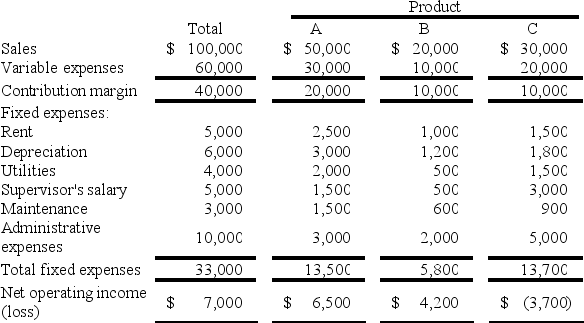

Mr. Morgan Henry, accountant for Black & Logan Co. Inc., has prepared the following product-line income data:

The following additional information is available:

The following additional information is available:  The factory rent of $1,500 assigned to Product C is avoidable if the product were dropped.

The factory rent of $1,500 assigned to Product C is avoidable if the product were dropped.  The company's total depreciation would not be affected by dropping C.

The company's total depreciation would not be affected by dropping C.  Eliminating Product C will reduce the monthly utility bill from $1,500 to $800.

Eliminating Product C will reduce the monthly utility bill from $1,500 to $800.  The supervisor's salary is avoidable.

The supervisor's salary is avoidable.  If Product C is discontinued, the maintenance department will be able to reduce monthly expenses from $3,000 to $2,000.

If Product C is discontinued, the maintenance department will be able to reduce monthly expenses from $3,000 to $2,000.  Elimination of Product C will make it possible to cut two persons from the administrative staff; their combined salaries total $3,000.

Required:

Prepare an analysis showing whether Product C should be eliminated.

Elimination of Product C will make it possible to cut two persons from the administrative staff; their combined salaries total $3,000.

Required:

Prepare an analysis showing whether Product C should be eliminated.

(Essay)

4.7/5 (33)

The price based on customers' perceived value for the product and the price that competitors charge is the:

(Multiple Choice)

4.8/5 (47)

Which of the following statements regarding differential costs is (are) false?

(A) The full-cost fallacy occurs when a decision-maker fails to include fixed manufacturing overhead in the product's cost.

(B) When deciding whether or not to accept a special order, a decision-maker should focus on differential costs instead of full costs.

(Multiple Choice)

4.9/5 (36)

Carlson Company makes 4,000 units per year of a part called an axial tap for use in one of its products. Data concerning the unit production costs of the axial tap follow:

Direct materials \ 35 Direct labor 10 Variable manufacturing overhead 8 Fixed manufacturing overhead 20 Total manufacturing cost per unit \7 3

An outside supplier has offered to sell Carlson Company all of the axial taps it requires. If Carlson Company decided to discontinue making the axial taps, 40% of the above fixed manufacturing overhead costs could be avoided. Assume that direct labor is a variable cost.

Required:

a. Assume Carlson Company has no alternative use for the facilities presently devoted to production of the axial taps. If the outside supplier offers to sell the axial taps for $65 each, should Carlson Company accept the offer? Fully support your answer with appropriate calculations.

b. Assume that Carlson Company could use the facilities presently devoted to production of the axial taps to expand production of another product that would yield an additional contribution margin of $80,000 annually. What is the maximum price Carlson Company should be willing to pay the outside supplier for axial taps?

(Essay)

4.8/5 (33)

Varix Company makes three products in a single facility. These products have the following unit product costs:

Additional data concerning these products are listed below.

Product A B Mixing minutes per unit 3.70 3.40 3.90 Selling price per unit \ 59.20 \ 60.10 \ 55.30 Variable selling cost per unit \ 2.90 \ 2.70 \ 3.70 Monthly demarnd in units 2,000 4,000 2,000

The mixing machines are potentially the constraint in the production facility. A total of 24,200 minutes is available per month on these machines.

Direct labor is a variable cost in this company.

Required:

a. How many minutes of mixing machine time would be required to satisfy demand for all three products?

b. How much of each product should be produced to maximize net operating income? (Round off to the nearest whole unit.)

c. Up to how much should the company be willing to pay for one additional hour of mixing machine time if the company has made the best use of the existing mixing machine capacity? (Round off to the nearest whole cent.)

Additional data concerning these products are listed below.

Product A B Mixing minutes per unit 3.70 3.40 3.90 Selling price per unit \ 59.20 \ 60.10 \ 55.30 Variable selling cost per unit \ 2.90 \ 2.70 \ 3.70 Monthly demarnd in units 2,000 4,000 2,000

The mixing machines are potentially the constraint in the production facility. A total of 24,200 minutes is available per month on these machines.

Direct labor is a variable cost in this company.

Required:

a. How many minutes of mixing machine time would be required to satisfy demand for all three products?

b. How much of each product should be produced to maximize net operating income? (Round off to the nearest whole unit.)

c. Up to how much should the company be willing to pay for one additional hour of mixing machine time if the company has made the best use of the existing mixing machine capacity? (Round off to the nearest whole cent.)

(Essay)

4.8/5 (33)

The following information relates to the Magna Company for the upcoming year, based on 400,000 units.

Amount Per Unit Sales \ 4,000,000 \ 10.00 Cost of goods sold Gross margin 800,000 2.00 Operating expenses Operating profits

The cost of goods sold includes $1,200,000 of fixed manufacturing overhead; the operating expenses include $100,000 of fixed marketing expenses. A special order offering to buy 50,000 units for $7.50 per unit has been made to Magna. Fortunately, there will be no additional operating expenses associated with the order and Magna has sufficient capacity to handle the order. How much will operate profits be increased if Magna accepts the special order?

(Multiple Choice)

4.8/5 (46)

Dumping occurs when a company exports its product to consumers in another country at an export price that is below the domestic price.

(True/False)

4.9/5 (39)

Douglas Corporation produces and sells three products. The three products, Alpha, Beta, and Gamma, are sold in a local market and in a regional market. At the end of the first quarter of the current year, the following income statement (in thousands of dollars) has been prepared:

Total Local Regional Sales revenue \ 5,200 \ 4,000 \ 1,200 Cost of goods sold 4,040 3,100 940 Gross margin 1,160 900 260 Marketing costs 420 240 180 Administrative costs 208 160 48 Operating profits \5 32 \5 00 \3 2

Management has expressed special concern with the regional market because of the extremely poor return on sales. This market was entered a year ago because of excess capacity. It was originally believed that the return on sales would improve with time, but after a year, no noticeable improvement can be seen from the results as reported in the above quarterly statement. In attempting to decide whether to eliminate the regional market, the following information has been gathered:

Products Alpha Beta Gamma Sales reveruse \ 2,000 \ 1,600 \ 1,600 Variable manufacturing cost\% of sales 60\% 70\% 60\% Variable marketing cost 3\% 2\% 2\%

Product Sales by Markets Local Regional Alpha \ 1,600 \ 400 Beta 1,200 400 Gamma 1,200 400

All administrative costs and fixed manufacturing costs are common to the three products and the two markets and are fixed for the period. Remaining marketing costs are fixed for the period and separable by market. All fixed costs have been arbitrarily allocated to markets.

Required:

a. Assuming there are no alternative uses for the Douglas Corporation's present capacity, would you recommend dropping the regional market? Why or why not?

b. Prepare the quarterly income statement showing contribution margins by products. Do not allocate fixed costs to products.

c. It is believed that a new product can be ready for sale next year if the Douglas Corporation decides to go ahead with continued research. The new product can be produced by simply converting equipment presently used in producing product Gamma. This conversion will increase fixed costs by $40,000 per quarter. What must the minimum contribution margin per quarter be for the new product to make the changeover financially feasible?

(Essay)

5.0/5 (38)

A customer has asked Balkans Corporation to supply 5,000 units of product DX9, with some modifications, for $40.20 each. The normal selling price of this product is $52.80 each. The normal unit product cost of product DX9 is computed as follows:

Direct materials \ 12.70 Direct labor 6.10 Variable manuffacturing overhead 8.70 Fixed manufacturing overhead 7.70 Unit product cost \3 5.20

Direct labor is a variable cost. The special order would have no effect on the company's total fixed manufacturing overhead costs. The customer would like some modifications made to product DX9 that would increase the variable costs by $3.50 per unit and that would require a one-time investment of $23,000 in special molds that would have no salvage value. This special order would have no effect on the company's other sales. The company has ample capacity for producing the special order.

Required:

Determine the effect on the company's total net operating income of accepting the special order. Show your work!

(Essay)

4.8/5 (38)

With constrained resources, the important measure of profitability is the contribution margin per unit of scarce resource.

(True/False)

5.0/5 (33)

A study has been conducted to determine if Product A should be dropped. Sales of the product total $200,000 per year; variable expenses total $140,000 per year. Fixed expenses charged to the product total $90,000 per year. The company estimates that $40,000 of these fixed expenses will continue even if the product is dropped. These data indicate that if Product A is dropped, the company's overall net operating income would:

(Multiple Choice)

4.8/5 (44)

The following information relates to the Jasmine Company for the upcoming year, based on 400,000 units:

Amount Per Unit Sales \ 8,000,000 \ 20.00 Cost of goods sold Gross margin 1,600,000 4.00 Operating expenses Operating profits

The cost of goods sold includes $2,400,000 of fixed manufacturing overhead; the operating expenses include $200,000 of fixed marketing expenses. A special order offering to buy 50,000 units for $15.00 per unit has been made to Jasmine.

- Fortunately, there will be no additional operating expenses associated with the order and Jasmine has sufficient capacity to handle the order. How much will operating profits increase if Jasmine accepts the special order?

(Multiple Choice)

4.8/5 (38)

Darren Company produces three products with the following costs and selling prices:

X Y Z Selling price per unit \ 40 \ 30 \ 35 Variable costs per unit 24 16 20 Contribution margin per unit \ 16 \ 14 \ 15 Direct labor hours per unit 4 2 3 Machine hours per unit 5 7 4

-

If Darren has a limit of 30,000 machine hours but no limit on units sold or direct labor hours, then the ranking of the products from the most profitable to the least profitable use of the constrained resource is:

(Multiple Choice)

4.8/5 (32)

Snagless Corporation has received a request for a special order of 9,000 units of product ZX9 for $46.50 each. The normal selling price of this product is $51.60 each, but the units would need to be modified slightly for the customer. The normal unit product cost of product ZX9 is computed as follows:

Direct materials 17.30 Direct labor 6.60 Variable manuffacturing overhead 3.80 Fixed manufacturing overhead 6.70 Unit product cost \ 34.40

Direct labor is a variable cost. The special order would have no effect on the company's total fixed manufacturing overhead costs. The customer would like some modifications made to product ZX9 that would increase the variable costs by $6.20 per unit and that would require a one-time investment of $46,000 in special molds that would have no salvage value. This special order would have no effect on the company's other sales. The company has ample capacity for producing the special order.

Required:

Determine the effect on the company's total net operating income of accepting the special order. Show your work!

(Essay)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)