Exam 7: Intercompany Transfers of Services and Noncurrent Assets

Exam 7: Intercompany Transfers of Services and Noncurrent Assets47 Questions

Exam 8: Intercompany Indebtedness39 Questions

Exam 8: Appendix a Intercompany Indebtedness40 Questions

Exam 9: Consolidation Ownership Issues51 Questions

Exam 10: Additional Consolidation Reporting Issues44 Questions

Exam 11: Multinational Accounting: Foreign Currency Transactions and Financial Instruments62 Questions

Exam 12: Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements65 Questions

Exam 13: Segment and Interim Reporting61 Questions

Exam 14: Sec Reporting49 Questions

Exam 15: Partnerships: Formation, Operation, and Changes in Membership55 Questions

Exam 16: Partnerships: Liquidation59 Questions

Exam 17: Governmental Entities: Introduction and General Fund Accounting79 Questions

Exam 18: Governmental Entities: Special Funds and Governmentwide Financial Statements79 Questions

Exam 19: Not-For-Profit Entities121 Questions

Exam 20: Corporations in Financial Difficulty41 Questions

Select questions type

On January 1, 20X7, Servant Company purchased a machine with an expected economic life of five years. On January 1, 20X9, Servant sold the machine to Master Corporation and recorded the following entry:  Master Corporation holds 75 percent of Servant's voting shares. Servant reported net income of $50,000, and Master reported income from its own operations of $100,000 for 20X9. There is no change in the estimated economic life of the equipment as a result of the intercorporate transfer.

Based on the preceding information, in the preparation of the 20X9 consolidated income statement, depreciation expense will be:

Master Corporation holds 75 percent of Servant's voting shares. Servant reported net income of $50,000, and Master reported income from its own operations of $100,000 for 20X9. There is no change in the estimated economic life of the equipment as a result of the intercorporate transfer.

Based on the preceding information, in the preparation of the 20X9 consolidated income statement, depreciation expense will be:

Free

(Multiple Choice)

4.8/5  (34)

(34)

Correct Answer: Verified

Verified

B

Phobos Company holds 80 percent of Deimos Company's voting shares. During the preparation of consolidated financial statements for 20X9, the following eliminating entry was made:  Which of the following statements is correct?

Which of the following statements is correct?

Free

(Multiple Choice)

5.0/5 (39)

Correct Answer:Verified

D

PeopleMag sells a plot of land for $100,000 to Seven Star Company, its 100 percent owned subsidiary, on January 1, 20X7. The cost of the land was $75,000, when it was purchased in 20X6. In 20X9, Seven Star sells the land to Hot Properties Inc., an unrelated entity, for $120,000. How is the land reported in the consolidated financial statements for 20X7, 20X8 and 20X9?

Free

(Essay)

4.9/5 (41)

Correct Answer:Verified

PeopleMag cannot report a gain on the sale of land for 2008 or 2009 in the consolidated financial statements. The land must be reported on the consolidated balance sheet at its original cost of $75,000. The intercompany gain is unrealized and is eliminated. In 2010, the entire gain of $45,000 ($120,000 - $75,000) is realized and recognized when the land is sold to an outside party.

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipment on a straight-line basis.

Based on the preceding information, the gain on sale of equipment recorded by Mortar for 20X8 is:

(Multiple Choice)

4.9/5 (44)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipments on a straight-line basis.

Based on the preceding information, in the preparation of elimination entries related to the equipment transfer for the 20X9 consolidated financial statements, the net effect on accumulated depreciation will be:

(Multiple Choice)

4.9/5 (36)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipment on a straight-line basis.

Based on the preceding information, in the preparation of the 20X8 consolidated financial statements, equipment will be:

(Multiple Choice)

5.0/5 (31)

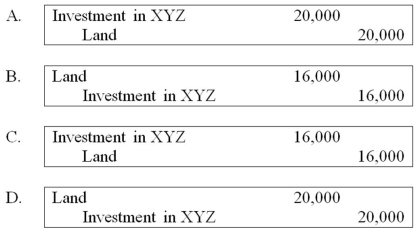

ABC Corporation purchased land on January 1, 20X6, for $50,000. On July 15, 20X8, it sold the land to its subsidiary, XYZ Corporation, for $70,000. ABC owns 80 percent of XYZ's voting shares.

Based on the preceding information, what will be the worksheet eliminating entry to remove the effects of the intercompany sale of land in preparing the consolidated financial statements for 20X9?

(Multiple Choice)

4.7/5 (40)

Peter Architectural Services owns 100 percent of Smith Manufacturing. During the course of 20X8 Peter provides $100,000 of architectural services associated with Smith's new manufacturing facility, which will open January 4, 20X9, and has a 5 year useful life. Explain the impact providing this service has on Peter Architectural Services' 20X8 and 20X9 consolidated financial statements.

(Essay)

4.9/5 (34)

Blue Corporation holds 70 percent of Black Company's voting common stock. On January 1, 20X3, Black paid $500,000 to acquire a building with a 10-year expected economic life. Black uses straight-line depreciation for all depreciable assets. On December 31, 20X8, Blue purchased the building from Black for $180,000. Blue reported income, excluding investment income from Black, of $140,000 and $162,000 for 20X8 and 20X9, respectively. Black reported net income of $30,000 and $45,000 for 20X8 and 20X9, respectively.

Based on the preceding information, the amount to be reported as consolidated net income for 20X9 will be:

(Multiple Choice)

4.7/5 (43)

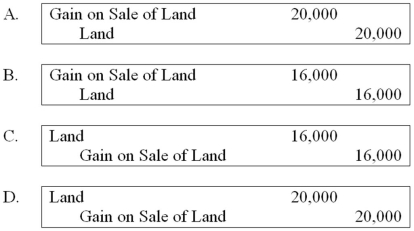

ABC Corporation purchased land on January 1, 20X6, for $50,000. On July 15, 20X8, it sold the land to its subsidiary, XYZ Corporation, for $70,000. ABC owns 80 percent of XYZ's voting shares.

Based on the preceding information, what will be the worksheet eliminating entry to remove the effects of the intercompany sale of land in preparing the consolidated financial statements for 20X8?

(Multiple Choice)

4.9/5 (38)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipment on a straight-line basis.

Based on the preceding information, in the preparation of the 20X9 consolidated income statement, depreciation expense will be:

(Multiple Choice)

4.8/5 (42)

Big Company acquired 75 percent of Little Company's stock at underlying book value on January 1, 20X8. At that date, the fair value of the noncontrolling interest was equal to 25 percent of the book value of Little Company. Little Company reported shares outstanding of $350,000 and retained earnings of $100,000. During 20X8, Little Company reported net income of $60,000 and paid dividends of $3,000. In 20X9, Little Company reported net income of $90,000 and paid dividends of $15,000. The following transactions occurred between Big Company and Little Company in 20X8 and 20X9:

Little Co. sold equipment to Big Co. for a $42,000 gain on December 31, 20X8. Little Co. had originally purchased the equipment for $140,000 and it had a carrying value of $28,000 on December 31, 20X8. At the time of the purchase, Big Co. estimated that the equipment still had a seven-year remaining useful life.

Big sold land costing $90,000 to Old Company on June 28, 20X9, for $110,000.

Required:

Give all eliminating entries needed to prepare a consolidation worksheet for 20X9 assuming that Big Co. uses the modified equity method to account for its investment in Old Company.

(Essay)

4.8/5 (45)

Sky Corporation owns 75 percent of Earth Company's stock. On July 1, 20X8, Sky sold a building to Earth for $33,000. Sky had purchased this building on January 1, 20X6, for $36,000. The building's original eight-year estimated total economic life remains unchanged. Both companies use straight-line depreciation. The equipment's residual value is considered negligible.

Based on the information provided, in the preparation of the 20X9 consolidated income statement, depreciation expense will be:

(Multiple Choice)

4.7/5 (43)

Blue Corporation holds 70 percent of Black Company's voting common stock. On January 1, 20X3, Black paid $500,000 to acquire a building with a 10-year expected economic life. Black uses straight-line depreciation for all depreciable assets. On December 31, 20X8, Blue purchased the building from Black for $180,000. Blue reported income, excluding investment income from Black, of $140,000 and $162,000 for 20X8 and 20X9, respectively. Black reported net income of $30,000 and $45,000 for 20X8 and 20X9, respectively.

Based on the preceding information, the amount of income assigned to the controlling shareholders in the consolidated income statement for 20X9 will be:

(Multiple Choice)

4.9/5 (34)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipment on a straight-line basis.

Based on the preceding information, in the preparation of elimination entries related to the equipment transfer for the 20X9 consolidated financial statements, net effect on accumulated depreciation will be:

(Multiple Choice)

4.8/5 (37)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipments on a straight-line basis.

Based on the preceding information, the gain on sale of the equipment recorded by Mortar for 20X8 is:

(Multiple Choice)

4.7/5 (35)

A parent sold land to its partially owned subsidiary during the year at a loss. The subsidiary continues to hold the land at the end of the year. The amount to be reported as consolidated net income for the year should equal:

(Multiple Choice)

4.8/5 (34)

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is expected to have a 10-year useful life and no salvage value. Both companies depreciate equipment on a straight-line basis.

Based on the preceding information, in the preparation of elimination entries related to the equipment transfer for the 20X8 consolidated financial statements, net effect on accumulated depreciation will be:

(Multiple Choice)

4.9/5 (36)

A wholly owned subsidiary sold land to its parent during the year at a gain. The parent continues to hold the land at the end of the year. The amount to be reported as consolidated net income for the year should equal:

(Multiple Choice)

4.8/5 (41)

Using the fully adjusted equity method, an intercompany gain on an upstream sale of land is:

(Multiple Choice)

5.0/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)