Exam 13: Segment and Interim Reporting

Exam 7: Intercompany Transfers of Services and Noncurrent Assets47 Questions

Exam 8: Intercompany Indebtedness39 Questions

Exam 8: Appendix a Intercompany Indebtedness40 Questions

Exam 9: Consolidation Ownership Issues51 Questions

Exam 10: Additional Consolidation Reporting Issues44 Questions

Exam 11: Multinational Accounting: Foreign Currency Transactions and Financial Instruments62 Questions

Exam 12: Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements65 Questions

Exam 13: Segment and Interim Reporting61 Questions

Exam 14: Sec Reporting49 Questions

Exam 15: Partnerships: Formation, Operation, and Changes in Membership55 Questions

Exam 16: Partnerships: Liquidation59 Questions

Exam 17: Governmental Entities: Introduction and General Fund Accounting79 Questions

Exam 18: Governmental Entities: Special Funds and Governmentwide Financial Statements79 Questions

Exam 19: Not-For-Profit Entities121 Questions

Exam 20: Corporations in Financial Difficulty41 Questions

Select questions type

Five of eight internally reported operating segments of Rollins Company qualify under the standards set by ASC 280 for segment reporting. However, the five identified segments do not meet the 75 percent revenue test. ASC 280 prescribes that management:

Free

(Multiple Choice)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

C

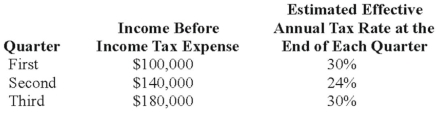

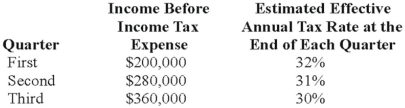

Denver Company, a calendar-year corporation, had the following actual income before income tax expense and estimated effective annual income tax rates for the first three quarters in 20X8:  Denver's income tax expense in its interim income statement for the third quarter should be:

Denver's income tax expense in its interim income statement for the third quarter should be:

Free

(Multiple Choice)

4.9/5 (34)

Correct Answer:Verified

B

Interim income statements are required for Smith Orchards. Smith does most of its sales in the fall quarter of the year. These sales are both to individual and commercial customers. How do you recommend Smith report sales during the spring quarter of the year?

Free

(Essay)

4.8/5 (36)

Correct Answer:Verified

Smith Orchards should be encouraged to supplement their interim reports with information for the 12-month periods ending at the interim date for both the current and preceding years. This form of disclosure reduces the possibility that users of the reports might make unwarranted inferences about the annual results from an interim report with material seasonal variations.

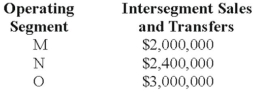

Main Manufacturing Corporation reported consolidated revenues of $50,000,000 on its income statement for 20X8. The management of the corporation identified 3 industry segments, M, N, and O. These segments had the following intersegment sales and transfers during 20X8:  For Main Manufacturing Corporation, the revenue test would be satisfied if any of its industry segments had revenue equal to or greater than which of the following?

For Main Manufacturing Corporation, the revenue test would be satisfied if any of its industry segments had revenue equal to or greater than which of the following?

(Multiple Choice)

4.9/5 (43)

Note: This is a Kaplan CPA Review Question

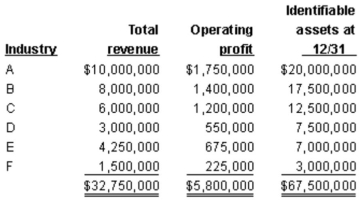

Correy Corp. and its divisions are engaged solely in manufacturing operations. The following data (consistent with prior years' data) pertain to the industries in which operations were conducted for the year ended December 31st:  In its segment information for the year, how many reportable segments does Correy have?

In its segment information for the year, how many reportable segments does Correy have?

(Multiple Choice)

4.9/5 (39)

In 20X6 and 20X7, each of Putney Company's four operating segments met one of the three quantitative tests for segment reporting. In 20X8, Segment B failed to qualify under the prescribed tests because of abnormal financial conditions. The other three segments qualified for reporting. For 20X8, Segment B:

(Multiple Choice)

4.7/5 (32)

On June 30, 20X8, String Corporation incurred a $220,000 net loss from disposal of a business component. Also, on June 30, 20X8, String paid $60,000 for property taxes assessed for the calendar year 20X8. What amount of the preceding items should be included in the determination of String's net income or loss for the six-month interim period ended June 30, 20X8?

(Multiple Choice)

4.9/5 (37)

Stone Company reported $100,000,000 of revenues on its 20X8 income statement. During the year ended December 31, 20X8, Stone made sales of $8,000,000 to external customers in Western Europe. In addition, Stone made sales of $10,000,000 to the U.S. government and $4,000,000 of sales to various state governments. In the footnotes to its financial statements for 20X8, in reporting enterprisewide disclosures, Stone is required to disclose:

(Multiple Choice)

4.9/5 (38)

Toledo Imports, a calendar-year corporation, had the following income before tax expense and estimated effective annual income tax rates for the first three quarters in 20X8:  Toledo's income tax expense in its interim income statement for the nine months ended September 30 and for the third quarter, respectively, are:

Toledo's income tax expense in its interim income statement for the nine months ended September 30 and for the third quarter, respectively, are:

(Multiple Choice)

4.7/5 (40)

Trevor Company discloses supplementary operating segment information for its three reportable segments. Data for 20X8 are available as follows:  Allocable costs for the year was $180,000. Allocable costs are assigned based on the ratio of a segment's income before allocable costs to total income before allocable costs. The 20X8 operating profit for Segment B was:

Allocable costs for the year was $180,000. Allocable costs are assigned based on the ratio of a segment's income before allocable costs to total income before allocable costs. The 20X8 operating profit for Segment B was:

(Multiple Choice)

4.9/5 (42)

The income tax expense applicable to the second quarter's income statement is determined by:

(Multiple Choice)

4.7/5 (36)

If a company changes the method it uses to compute the allowance for uncollectible accounts receivable because more recent information has become available, how is this change in method is accounted for?

(Multiple Choice)

4.9/5 (42)

On March 15, 20X9, Clarion Company paid property taxes of $60,000 on its factory building for calendar year 20X9. On July 1, 20X9, Clarion made $40,000 in unanticipated repairs to its machinery. The repairs will benefit operations for the remainder of the calendar year. What total amount of these expenses should be included in Clarion's quarterly income statement for the three months ended September 30, 20X9?

(Multiple Choice)

4.8/5 (44)

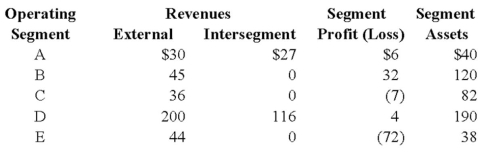

An analysis of Abbey Company's operating segments provides the following information:  Refer to the above information. Which of the operating segments above are reportable segments?

Refer to the above information. Which of the operating segments above are reportable segments?

(Multiple Choice)

4.7/5 (38)

Wakefield Company uses a perpetual inventory system. In August, it sold 2,000 units from its LIFO-base inventory, which had originally cost $35 per unit. The replacement cost is expected to be $45 per unit. The company is planning to reduce its inventory and expects to replace only 1,500 of these units by December 31, the end of its fiscal year. The company replaced 1,500 units in November at an actual cost of $50 per unit.

Assume that the replacement did not happen in November. In December, the company decided not to replace any of the 1,500 units. The entry required on December 31 to eliminate valuation accounts related to the inventory that will not be replaced will include:

(Multiple Choice)

4.8/5 (36)

Missoula Corporation disposed of one of its segments in the second quarter and incurred a gain from disposal of discontinued segment of $600,000, net of taxes. What is the effect of this gain from disposal of discontinued segment?

(Multiple Choice)

4.8/5 (39)

Samuel Corporation foresees a downturn in its business in the medium term. It expects to sustain an operating loss of $160,000 for the full year ending December 31, 20X8. Samuel's tax rate is 35 percent. Anticipated tax credits for 20X8 total $8,000. No permanent differences are expected. Realization of the full tax benefit of the expected operating loss and realization of anticipated tax credits are assured beyond any reasonable doubt because they will be carried back. For the first quarter ended March 31, 20X8, Samuel reported an operating loss of $30,000. How much of a tax benefit should Samuel report for the interim period ended March 31, 20X8?

(Multiple Choice)

4.9/5 (32)

Note: This is a Kaplan CPA Review Question

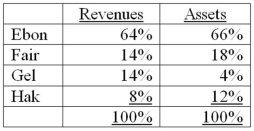

Cott Co.'s four business segments have revenues and identifiable assets expressed as percentages of Cott's total revenues and total assets as follows:  Which of these business segments are deemed to be reportable segments?

Which of these business segments are deemed to be reportable segments?

(Multiple Choice)

4.8/5 (39)

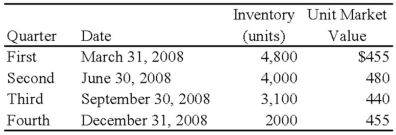

Forge Company, a calendar-year entity, had 6,000 units in its beginning inventory for 20X8. On December 31, 20X7, the units had been adjusted down to $470 per unit from an actual cost of $510 per unit. It was the lower of cost or market. No additional units were purchased during 20X8. The following additional information is provided for 20X8:  Forge does not have sufficient experience with the seasonal market for its inventory units and assumes that any reductions in market value during the year will be permanent.

Based on the preceding information, the cost of goods sold for the first quarter is:

Forge does not have sufficient experience with the seasonal market for its inventory units and assumes that any reductions in market value during the year will be permanent.

Based on the preceding information, the cost of goods sold for the first quarter is:

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)