Exam 14: Applying Financial Modeling

Exam 1: Introduction to Mergers, Acquisitions, and Other Restructuring Activities139 Questions

Exam 2: The Regulatory Environment129 Questions

Exam 3: The Corporate Takeover Market:152 Questions

Exam 4: Planning: Developing Business and Acquisition Plans: Phases 1 and 2 of the Acquisition Process137 Questions

Exam 5: Implementation: Search Through Closing: Phases 310 of the Acquisition Process131 Questions

Exam 6: Postclosing Integration: Mergers, Acquisitions, and Business Alliances138 Questions

Exam 7: Merger and Acquisition Cash Flow Valuation Basics108 Questions

Exam 8: Relative, Asset-Oriented, and Real Option109 Questions

Exam 9: Financial Modeling Basics:97 Questions

Exam 10: Analysis and Valuation127 Questions

Exam 11: Structuring the Deal:138 Questions

Exam 12: Structuring the Deal:125 Questions

Exam 13: Financing the Deal149 Questions

Exam 14: Applying Financial Modeling116 Questions

Exam 15: Business Alliances: Joint Ventures, Partnerships, Strategic Alliances, and Licensing138 Questions

Exam 16: Alternative Exit and Restructuring Strategies152 Questions

Exam 17: Alternative Exit and Restructuring Strategies:118 Questions

Exam 18: Cross-Border Mergers and Acquisitions:120 Questions

Select questions type

To determine if certain cash flows result from synergy ask if they can be generated only if the businesses are combined. If the answer is yes, then the cash flow in question is due to synergy.

Free

(True/False)

4.8/5  (41)

(41)

Correct Answer: Verified

Verified

True

Selecting the appropriate financing structure for the combined firms requires consideration of which of the following:

Free

(Multiple Choice)

5.0/5 (32)

Correct Answer:Verified

E

The effects of synergy resulting from combining the acquirer and target firms do not affect the acquirer's ability to finance the transaction.

Free

(True/False)

4.9/5 (48)

Correct Answer:Verified

False

Ultimately, what fraction of synergy is negotiated successfully by the target depends on its leverage or influence relative to the acquirer.

(True/False)

4.8/5 (41)

It is unimportant whether the acquirer uses the target's or its own weighted average cost of capital when valuing the target firm.

(True/False)

4.8/5 (41)

Thermo Fisher paid $76 per share for each outstanding share of Life Tech. What is the maximum offer price Thermo Fisher could have made without ceding all of the synergy value to Life Tech shareholders? (Hint: Using the Transaction Summary Worksheet, increase the offer price until the NPV in the section entitled Valuation turns negative.)

(Essay)

4.9/5 (43)

Pro forma financial statements are frequently used to show what the acquirer and target's combined financial statements would look like if they were merged.

(True/False)

4.8/5 (43)

Ford Acquires Volvo’s Passenger Car Operations

This case illustrates how the dynamically changing worldwide automotive market is spurring a move toward consolidation among automotive manufacturers. The Volvo financials used in the valuation are for illustration only— they include revenue and costs for all of the firm’s product lines. For purposes of exposition, we shall assume that Ford’s acquisition strategy with respect to Volvo was to acquire all of Volvo’s operations and later to divest all but the passenger car and possibly the truck operations. Note that synergy in this business case is determined by valuing projected cash flows generated by combining the Ford and Volvo businesses rather than by subtracting the standalone values for the Ford and Volvo passenger car operations from their combined value including the effects of synergy. This was done because of the difficulty in obtaining sufficient data on the Ford passenger car operations.

Background

By the late 1990s, excess global automotive production capacity totaled 20 million vehicles, and three-fourths of the auto manufacturers worldwide were losing money. Consumers continued to demand more technological innovations, while expecting to pay lower prices. Continuing mandates from regulators for new, cleaner engines and more safety measures added to manufacturing costs. With the cost of designing a new car estimated at $1.5 billion to $3 billion, companies were finding mergers and joint ventures an attractive means to distribute risk and maintain market share in this highly competitive environment.

By acquiring Volvo, Ford hoped to expand its 10% worldwide market share with a broader line of near-luxury Volvo sedans and station wagons as well as to strengthen its presence in Europe. Ford saw Volvo as a means of improving its product weaknesses, expanding distribution channels, entering new markets, reducing development and vehicle production costs, and capturing premiums from niche markets. Volvo Cars is now part of Ford’s Premier Automotive Group, which also includes Aston Martin, Jaguar, and Lincoln. Between 1987 and 1998, Volvo posted operating profits amounting to 3.7% of sales. Excluding the passenger car group, operating margins would have been 5.3%. To stay competitive, Volvo would have to introduce a variety of new passenger cars over the next decade. Volvo viewed the capital expenditures required to develop new cars as overwhelming for a company its size.

Historical and Projected Data

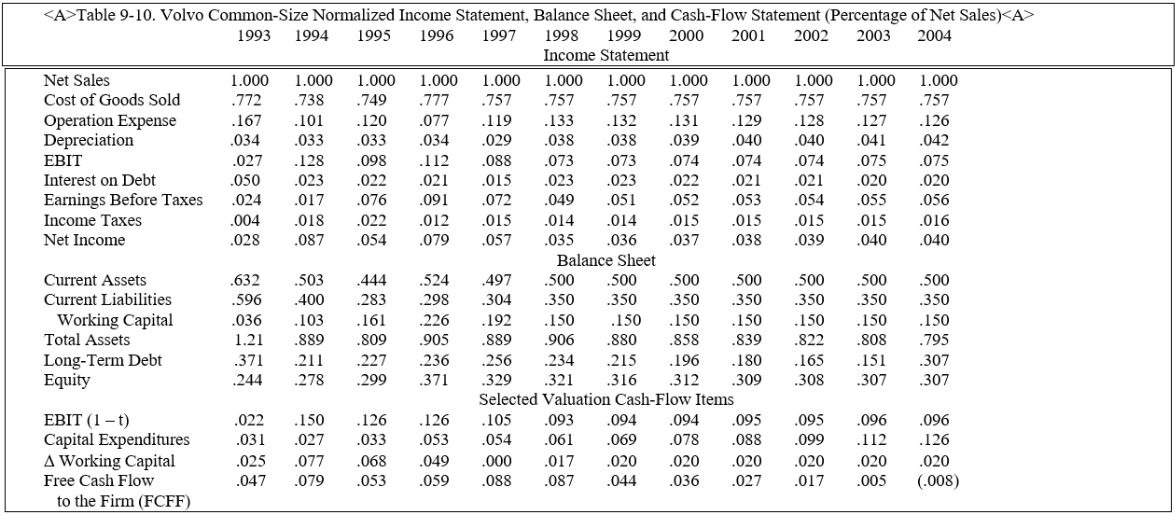

The initial review of Volvo’s historical data suggests that cash flow is highly volatile. However, by removing nonrecurring events, it is apparent that Volvo’s cash flow is steadily trending downward from its high in 1997. Table 9-10 displays a common-sized, normalized income statement, balance sheet, and cash-flow statement for Volvo, including both the historical period from 1993 through 1999 and a forecast period from 2000 through 2004. Although Volvo has managed to stabilize its cost of goods sold as a percentage of net sales, operating expenses as a percentage of net revenue have escalated in recent years. Operating margins have been declining since 1996. To regain market share in the passenger car market, Volvo would have to increase substantially its capital outlays. The primary reason valuation cash flow turns negative by 2004 is the sharp increase in capital outlays during the forecast period. Ford’s acquisition of Volvo will enable volume discounts from vendors, reduced development costs as a result of platform sharing, access to wider distribution networks, and increased penetration in selected market niches because of the Volvo brand name. Savings from synergies are phased in slowly over time, and they will not be fully realized until 2004. There is no attempt to quantify the increased cash flow that might result from increased market penetration.

Determining the Initial Offer Price

Volvo’s estimated value on a standalone basis is $15 billion. The present value of anticipated synergy is $1.1 billion, suggesting that the purchase price for Volvo should lie within a range of $15 million to about $16 billion. Although potential synergies appear to be substantial, savings due to synergies will be phased in gradually between 2000 and 2004. The absence of other current bidders for the entire company and Volvo’s urgent need to fund future capital expenditures in the passenger car business enabled Ford to set the initial offer price at the lower end of the range. Thus, the initial offer price could be conservatively set at about $15.25 billion, reflecting only about one-fourth of the total potential synergy resulting from combining the two businesses. Other valuation methodologies tended to confirm this purchase price estimate. The market value of Volvo was $11.9 billion on January 29, 1999. To gain a controlling interest, Ford had to pay a premium to the market value on January 29, 1999. Applying the 26% premium Ford paid for Jaguar, the estimated purchase price including the premium is $15 billion, or $34 per share. This compares to $34.50 per share estimated by dividing the initial offer price of $15.25 billion by Volvo’s total common shares outstanding of 442 million.

Determining the Appropriate Financing Structure

Ford had $23 billion in cash and marketable securities on hand at the end of 1998 (Naughton, 1999). This amount of cash is well in excess of its normal cash operating requirements. The opportunity cost associated with this excess cash is equal to Ford’s cost of capital, which is estimated to be 11.5%—about three times the prevailing interest on short-term marketable securities at that time. By reinvesting some portion of these excess balances to acquire Volvo, Ford would be adding to shareholder value, because the expected return, including the effects of synergy, exceeds the cost of capital. Moreover, by using this excess cash, Ford also is making itself less attractive as a potential acquisition target. The acquisition is expected to increase Ford’s EPS. The loss of interest earnings on the excess cash balances would be more than offset by the addition of Volvo’s pretax earnings.

Epilogue

Seven months after the megamerger between Chrysler and Daimler-Benz in 1998, Ford Motor Company announced that it was acquiring only Volvo’s passenger-car operations. Ford acquired Volvo’s passenger car operations on March 29, 1999, for $6.45 billion. At $16,000 per production unit, Ford’s offer price was considered generous when compared with the $13,400 per vehicle that Daimler-Benz AG paid for Chrysler Corporation in 1998. The sale of the passenger car business allows Volvo to concentrate fully on its truck, bus, construction equipment, marine engine, and aerospace equipment businesses. (Note that the standalone value of Volvo in the case was estimated to be $15 billion. This included Volvo’s trucking operations.)

-Ford anticipates substantial synergies from acquiring Volvo. What are these potential synergies? As a consultant hired to value Volvo, what additional information would you need to estimate the value of potential synergy from each of these areas?

Determining the Initial Offer Price

Volvo’s estimated value on a standalone basis is $15 billion. The present value of anticipated synergy is $1.1 billion, suggesting that the purchase price for Volvo should lie within a range of $15 million to about $16 billion. Although potential synergies appear to be substantial, savings due to synergies will be phased in gradually between 2000 and 2004. The absence of other current bidders for the entire company and Volvo’s urgent need to fund future capital expenditures in the passenger car business enabled Ford to set the initial offer price at the lower end of the range. Thus, the initial offer price could be conservatively set at about $15.25 billion, reflecting only about one-fourth of the total potential synergy resulting from combining the two businesses. Other valuation methodologies tended to confirm this purchase price estimate. The market value of Volvo was $11.9 billion on January 29, 1999. To gain a controlling interest, Ford had to pay a premium to the market value on January 29, 1999. Applying the 26% premium Ford paid for Jaguar, the estimated purchase price including the premium is $15 billion, or $34 per share. This compares to $34.50 per share estimated by dividing the initial offer price of $15.25 billion by Volvo’s total common shares outstanding of 442 million.

Determining the Appropriate Financing Structure

Ford had $23 billion in cash and marketable securities on hand at the end of 1998 (Naughton, 1999). This amount of cash is well in excess of its normal cash operating requirements. The opportunity cost associated with this excess cash is equal to Ford’s cost of capital, which is estimated to be 11.5%—about three times the prevailing interest on short-term marketable securities at that time. By reinvesting some portion of these excess balances to acquire Volvo, Ford would be adding to shareholder value, because the expected return, including the effects of synergy, exceeds the cost of capital. Moreover, by using this excess cash, Ford also is making itself less attractive as a potential acquisition target. The acquisition is expected to increase Ford’s EPS. The loss of interest earnings on the excess cash balances would be more than offset by the addition of Volvo’s pretax earnings.

Epilogue

Seven months after the megamerger between Chrysler and Daimler-Benz in 1998, Ford Motor Company announced that it was acquiring only Volvo’s passenger-car operations. Ford acquired Volvo’s passenger car operations on March 29, 1999, for $6.45 billion. At $16,000 per production unit, Ford’s offer price was considered generous when compared with the $13,400 per vehicle that Daimler-Benz AG paid for Chrysler Corporation in 1998. The sale of the passenger car business allows Volvo to concentrate fully on its truck, bus, construction equipment, marine engine, and aerospace equipment businesses. (Note that the standalone value of Volvo in the case was estimated to be $15 billion. This included Volvo’s trucking operations.)

-Ford anticipates substantial synergies from acquiring Volvo. What are these potential synergies? As a consultant hired to value Volvo, what additional information would you need to estimate the value of potential synergy from each of these areas?

(Essay)

4.8/5 (32)

In determining the initial offer price, the acquirer must decide how much of the anticipated synergy to share with the target firm's shareholders.

(True/False)

5.0/5 (36)

Acquiring Company is considering buying Target Company. Target Company is a small biotechnology

firm, which develops products that are licensed to the major pharmaceutical firms? Development costs are expected to generate negative cash flows during the first two years of the forecast period of $(10) and $(5) million, respectively. Licensing fees are expected to generate positive cash flows during years three through five of the forecast period of $5, $10, and $15 million, respectively. Due to the emergence of competitive products, cash flow is expected to grow at a modest 5 percent annually after the fifth year. The discount rate for the first five years is estimated to be 20 percent and then to drop to 10 percent beyond the fifth year. In addition, the present value of the estimated synergy by combining Acquiring and Target companies is $30 million. Calculate the minimum and maximum purchase prices for Target Company. Show your work.

(Essay)

4.7/5 (37)

Assume a firm's debt to equity ratio is currently below its industry average. Increasing it to the industry average can represent a source of value.

(True/False)

4.9/5 (28)

A firm's enterprise and equity values will increase in response to all of the following variables assuming other things are equal except for

(Multiple Choice)

4.7/5 (43)

The share exchange ratio is impacted by all of the following except for

(Multiple Choice)

4.9/5 (37)

Realizing synergy often requires spending money. Which of the following are examples of such expenditures?

(Multiple Choice)

4.8/5 (42)

The target firm's underutilized borrowing capacity is often considered a source of value.

(True/False)

5.0/5 (29)

Although public firms are required to file their financial statements with the Securities and Exchange Commission in accordance with GAAP, so-called pro forma financial statements are used as hypothetical representations of the potential performance of the acquirer and target firms if they were merged.

(True/False)

4.8/5 (38)

Which of the following questions can be addressed by financial models?

(Multiple Choice)

4.8/5 (39)

Can the initial offer price ever exceed the maximum purchase price? If yes, why? If no, why not?

(Essay)

4.9/5 (38)

How does a firm's enterprise value change if the firm issues equity and uses the proceeds to repay debt?

(Multiple Choice)

5.0/5 (41)

Mars Buys Wrigley in One Sweet Deal

Under considerable profit pressure from escalating commodity prices and eroding market share, Wrigley Corporation, a U.S.-based leader in gum and confectionery products, faced increasing competition from Cadbury Schweppes in the U.S. gum market. Wrigley had been losing market share to Cadbury since 2006. Mars Corporation, a privately owned candy company with annual global sales of $22 billion, sensed an opportunity to achieve sales, marketing, and distribution synergies by acquiring Wrigley Corporation.

On April 28, 2008, Mars announced that it had reached an agreement to merge with Wrigley Corporation for $23 billion in cash. Under the terms of the agreement, which were unanimously approved by the boards of the two firms, shareholders of Wrigley would receive $80 in cash for each share of common stock outstanding, a 28 percent premium to Wrigley's closing share price of $62.45 on the announcement date. The merged firms in 2008 would have a 14.4 percent share of the global confectionary market, annual revenue of $27 billion, and 64,000 employees worldwide. The merger of the two family-controlled firms represents a strategic blow to competitor Cadbury Schweppes's efforts to continue as the market leader in the global confectionary market with its gum and chocolate business. Prior to the announcement, Cadbury had a 10 percent worldwide market share.

As of the September 28, 2008 closing date, Wrigley became a separate stand-alone subsidiary of Mars, with $5.4 billion in sales. The deal is expected to help Wrigley augment its sales, marketing, and distribution capabilities. To provide more focus to Mars's brands in an effort to stimulate growth, Mars would in time transfer its global nonchocolate confectionery sugar brands to Wrigley. Bill Wrigley Jr., who controls 37 percent of the firm's outstanding shares, remained the executive chairman of Wrigley. The Wrigley management team also remained in place after closing.

The combined companies would have substantial brand recognition and product diversity in six growth categories: chocolate, nonchocolate confectionary, gum, food, drinks, and pet care products. While there is little product overlap between the two firms, there is considerable geographic overlap. Mars is located in 100 countries, while Wrigley relies heavily on independent distributors in its growing international distribution network. Furthermore, the two firms have extensive sales forces, often covering the same set of customers.

While mergers among competitors are not unusual, the deal's highly leveraged financial structure is atypical of transactions of this type. Almost 90 percent of the purchase price would be financed through borrowed funds, with the remainder financed largely by a third-party equity investor. Mars's upfront costs would consist of paying for closing costs from its cash balances in excess of its operating needs. The debt financing for the transaction would consist of $11 billion and $5.5 billion provided by J.P. Morgan Chase and Goldman Sachs, respectively. An additional $4.4 billion in subordinated debt would come from Warren Buffet's investment company, Berkshire Hathaway, a nontraditional source of high-yield financing. Historically, such financing would have been provided by investment banks or hedge funds and subsequently repackaged into securities and sold to long-term investors, such as pension funds, insurance companies, and foreign investors. However, the meltdown in the global credit markets in 2008 forced investment banks and hedge funds to withdraw from the high-yield market in an effort to strengthen their balance sheets. Berkshire Hathaway completed the financing of the purchase price by providing $2.1 billion in equity financing for a 9.1 percent ownership stake in Wrigley.

-How might the additional product and geographic diversity achieved by combining Mars and Wrigley benefit the combined firms?

(Essay)

4.7/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)