Exam 10: Analysis and Valuation

Membership or subscription businesses, such as health clubs and magazine publishers, may inflate revenue by booking the full value of muliyear contracts in the first year of the contract.

True

The fair value concept is applied when no strong market exists for a business or it is not possible to identify the value of substantially similar firms.

True

Taking Advantage of a “Cupcake Bubble”

_____________________________________________________________________________________

Key Points

Financing growth represents a common challenge for most small businesses.

Selling a portion of the business either to private investors or in a public offering represents a common way for small businesses to finance major expansion plans.

____________________________________________________________________________

When Crumbs first opened in 2003 on the upper west side of Manhattan, the bakery offered three varieties of cupcakes among 150 other items. When the cupcakes became increasingly popular, the bakery began introducing cupcakes with different toppings and decorations. The firm’s founders, Jason and Mia Bauer, followed a straightforward business model: Hold costs down, and minimize investment in equipment. Although all of Crumbs’ cupcake recipes are Mia Bauer’s, there are no kitchens or ovens on the premises. Instead, Crumbs outsources all of the baking activities to commercial facilities. The firm avoids advertising, preferring to give away free cupcakes when it opens a new store and to rely on “word of mouth.” By keeping costs low, the firm has expanded without adding debt. The firm targets locations with high daytime “foot traffic,” such as urban markets. In 2010, the firm sold 13 million cupcakes through 34 locations, accounting for $31 million in revenue and $2.5 million in earnings before interest, taxes, and depreciation. Crumbs’ success spawned a desire to accelerate growth by opening up as many as 200 new locations by 2014. The challenge was how to finance such a rapid expansion.

The Bauers were no strangers to raising capital to finance the ongoing growth of their business, having sold one-half of the firm to Edwin Lewis, former CEO of Tommy Hilfiger, for $10 million in 2008. This enabled them to reinvest a portion in the business to sustain growth as well as to draw cash out of the business for their personal use. However, this time the magnitude of their financing requirements proved daunting. The couple was reluctant to burden the business with excessive debt, well aware that this had contributed to the demise of so many other rapidly growing businesses. Equity could be sold directly in the private placement market or to the public. Private placements could be expensive and may not provide the amount of financing needed; tapping the public markets directly through an IPO required dealing with underwriters and a level of financial expertise they lacked. Selling to another firm seemed to satisfy best their primary objectives: Get access to capital, retain their top management positions, and utilize the financial expertise of others to tap the public capital markets and to share in any future value creation.

The 57th Street General Acquisition Corporation (57th Street), a special-purpose acquisition company, or SPAC, appeared to meet their needs. In May 2010, 57th Street raised $54.5 million through an IPO, with the proceeds placed in a trust pending the completion of planned acquisitions. One year later, 57th Street announced it had acquired Crumbs for $27 million in cash and $39 million in 57th Street stock. On June 30, 2011, 57th announced that NASDAQ had approved the listing of its common stock, giving Crumbs a market value of nearly $60 million.

Panda Ethanol Goes Public in a Shell Corporation

In early 2007, Panda Ethanol, owner of ethanol plants in west Texas, decided to explore the possibility of taking its ethanol production business public to take advantage of the high valuations placed on ethanol-related companies in the public market at that time. The firm was confronted with the choice of taking the company public through an initial public offering or by combining with a publicly traded shell corporation through a reverse merger.

After enlisting the services of a local investment banker, Grove Street Investors, Panda chose to "go public" through a reverse merger. This process entailed finding a shell corporation with relatively few shareholders who were interested in selling their stock. The investment banker identified Cirracor Inc. as a potential merger partner. Cirracor was formed on October 12, 2001, to provide website development services and was traded on the over-the-counter bulletin board market (i.e., a market for very low-priced stocks). The website business was not profitable, and the company had only ten shareholders. As of June 30, 2006, Cirracor listed $4,856 in assets and a negative shareholders' equity of $(259,976). Given the poor financial condition of Cirracor, the firm's shareholders were interested in either selling their shares for cash or owning even a relatively small portion of a financially viable company to recover their initial investments in Cirracor. Acting on behalf of Panda, Grove Street formed a limited liability company, called Grove Panda, and purchased 2.73 million Cirracor common shares, or 78 percent of the company, for about $475,000.

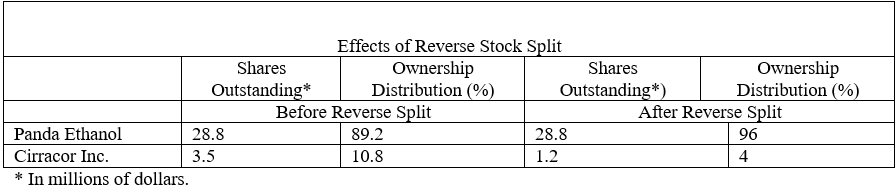

The merger proposal provided for one share of Cirracor common stock to be exchanged for each share of Panda Ethanol common outstanding stock and for Cirracor shareholders to own 4 percent of the newly issued and outstanding common stock of the surviving company. Panda Ethanol shareholders would own the remaining 96 percent. At the end of 2005, Panda had 13.8 million shares outstanding. On June 7, 2007, the merger agreement was amended to permit Panda Ethanol to issue 15 million new shares through a private placement to raise $90 million. This brought the total Panda shares outstanding to 28.8 million. Cirracor common shares outstanding at that time totaled 3.5 million. However, to achieve the agreed-on ownership distribution, the number of Cirracor shares outstanding had to be reduced. This would be accomplished by an approximate three-for-one reverse stock split immediately prior to the completion of the reverse merger (i.e., each Cirracor common share would be converted into 0.340885 shares of Cirracor common stock). As a consequence of the merger, the previous shareholders of Panda Ethanol were issued 28.8 million new shares of Cirracor common stock. The combined firm now has 30 million shares outstanding, with the Cirracor shareholders owning 1.2 million shares. The following table illustrates the effect of the reverse stock split.

A special Cirracor shareholders' meeting was required by Nevada law (i.e., the state in which Cirracor was incorporated) in view of the substantial number of new shares that were to be issued as a result of the merger. The proxy statement filed with the Securities and Exchange Commission and distributed to Cirracor shareholders indicated that Grove Panda, a 78 percent owner of Cirracor common stock, had already indicated that it would vote its shares for the merger and the reverse stock split. Since Cirracor's articles of incorporation required only a simple majority to approve such matters, it was evident to all that approval was imminent.

On November 7, 2007, Panda completed its merger with Cirracor Inc. As a result of the merger, all shares of Panda Ethanol common stock (other than Panda Ethanol shareholders who had executed their dissenters' rights under Delaware law) would cease to have any rights as a shareholder except the right to receive one share of Cirracor common stock per share of Panda Ethanol common. Panda Ethanol shareholders choosing to exercise their right to dissent would receive a cash payment for the fair value of their stock on the day immediately before closing. Cirracor shareholders had similar dissenting rights under Nevada law. While Cirracor is the surviving corporation, Panda is viewed for accounting purposes as the acquirer. Accordingly, the financial statements shown for the surviving corporation are those of Panda Ethanol.

-Why do you believe Panda did not directly approach Cirraco ? How were the Panda Grove investment holdings used to influence the outcome of the proposed merger?

A special Cirracor shareholders' meeting was required by Nevada law (i.e., the state in which Cirracor was incorporated) in view of the substantial number of new shares that were to be issued as a result of the merger. The proxy statement filed with the Securities and Exchange Commission and distributed to Cirracor shareholders indicated that Grove Panda, a 78 percent owner of Cirracor common stock, had already indicated that it would vote its shares for the merger and the reverse stock split. Since Cirracor's articles of incorporation required only a simple majority to approve such matters, it was evident to all that approval was imminent.

On November 7, 2007, Panda completed its merger with Cirracor Inc. As a result of the merger, all shares of Panda Ethanol common stock (other than Panda Ethanol shareholders who had executed their dissenters' rights under Delaware law) would cease to have any rights as a shareholder except the right to receive one share of Cirracor common stock per share of Panda Ethanol common. Panda Ethanol shareholders choosing to exercise their right to dissent would receive a cash payment for the fair value of their stock on the day immediately before closing. Cirracor shareholders had similar dissenting rights under Nevada law. While Cirracor is the surviving corporation, Panda is viewed for accounting purposes as the acquirer. Accordingly, the financial statements shown for the surviving corporation are those of Panda Ethanol.

-Why do you believe Panda did not directly approach Cirraco ? How were the Panda Grove investment holdings used to influence the outcome of the proposed merger?

: Note that Panda could have approached Ciracco directly. However, this may have alerted the Ciracco shareholders to the Panda’s intentions and could have encouraged them to hold out for a higher purchase price for their stock. As an agent for Panda, Grove was able to buy the stock less expensively since Ciracco’s shareholders, desperate to recover a portion of their original investment, would have welcomed almost any alternative to bankruptcy.

Nevada, the state in which Cirracor was incorporate, state law requires that given the significant number of new share issued a shareholders vote was required to approve the new issue. Approval required a simple majority vote. Since Panda Grove let other shareholders know that it owned 78% and that in proxy materials indicated that it would vote for the merger and reverse split, it was evident to all shareholders that approval was imminent.

Note: Total Panda shares outstanding (including 15 million newly issued shares in the private placement) equaled 28.8 million shares. As a result of negotiations, Panda shareholders would own 96% of the merged firms and Cirracor shareholders 4%. This implied that total shares outstanding of the merged firms could not exceed 30 million shares (i.e., 28.8/.96). Consequently, Cirracor shareholders would own 1.2 million shares (i.e., 30 – 28.8). Since Cirracor shares outstanding totaled 3.5 million before the merger, a reverse split was implemented coincidental to the reverse merger using a ratio of .340885 shares of Cirracor stock for each share of Panda stock (i.e., .340885 x 3.5 = 1.19). Note the 1.2 reflects rounding error due to rounding the number of shares outstanding for both firms.

Succession issues tend to be easier for small family owned firms than for large publicly traded firms.

Increasing market liquidity will reduce the value of control; an increasing value of control will reduce market liquidity and contribute to increasing liquidity discounts.

Firms that are family owned but not managed by family members are often well managed, as family shareholders with large equity stakes carefully monitor those charged with managing the business.

The purpose of adjusting the target's income statement is to provide an accurate estimate of the

current year's reported operating income or operating cash flow.

The control model of corporate governance may be more applicable where ownership tends to be highly diverse and the right to control the business is separate from ownership.

If a buyer expects that the target firm's revenue has been overstated, the buyer can reconstruct revenue by examining usage levels of the key inputs required to produce the product or service.

Why might succession planning be more challenging for family owned firms?

What is the purpose of ultimately listing of a major stock exchange such as NASDAQ?

All of the following represent common sources of value in appraising private or publicly owned businesses except for

Studies show that control premiums vary widely across countries reflecting the efficacy of shareholder rights laws and how well such laws are enforced in each country.

Determining Liquidity Discounts: The Taylor Devices and Tayco Development Merger

Privately held shares or shares for which there is not a readily available resale market often can only be sold at a discount from what is believed to be their intrinsic value.

However, estimating the magnitude of the discount often is highly problematic.

____________________________________________________________________________________________

This discussion is a highly summarized version of how a business valuation firm evaluated the liquidity risk associated with Taylor Devices’ unregistered common stock, registered common shares, and a minority investment in a business that it was planning to sell following its merger with Tayco Development. The estimated liquidity discounts were used in a joint proxy statement submitted to the SEC by the two firms to justify the value of the offer the boards of Taylor Devices and Tayco Development had negotiated.

Taylor Devices and Tayco Development agreed to merge in early 2008. Tayco would be merged into Taylor, with Taylor as the surviving entity. The merger would enable Tayco’s patents and intellectual property to be fully

Source: SEC Form S4 filing of a proxy statement for Taylor Devices and Tayco Development dated 1/15/08.

integrated into Taylor’s manufacturing operations, since intellectual property rights transfer with the Tayco stock. Each share of Tayco common stock would be converted into one share of Taylor common stock, according to the terms of the deal. Taylor’s common stock is traded on the NASDAQ Small Cap Market under the symbol TAYD, and on January 8, 2009 (the last trading day before the date of the filing of the joint proxy statement with the SEC), the stock closed at $6.29 per share. Tayco common stock is traded over the counter on “Pink Sheets” (i.e., an informal trading network) under the trading symbol TYCO.PK, and it closed on January 8, 2009, at $5.11 per share.

An appraisal firm was hired to value Taylor’s unregistered shares, which were treated as if they were restricted shares because there was no established market for trading in these shares. The appraiser believed that the risk of Taylor’s unregistered shares is greater than for letter stocks, which have a stipulated period during which the shares cannot be sold, because the Taylor shares lacked a date indicating when they could be sold. Using this line of reasoning, the appraisal firm estimated a liquidity discount of 20%, which it believed approximated the potential loss that holders of these shares might incur in attempting to sell their shares. The block of registered Taylor stock differs from the unregistered shares, in that they are not subject to Rule 144. Based on the trading volume of Taylor common stock over the preceding 12 months, the appraiser believed that it would likely take less than one year to convert the block of registered stock into cash and estimated the discount at 13%, consistent with the Aschwald (2000) studies.

The appraisal firm also was asked to estimate the liquidity discount for the sale of Taylor’s minority investment in a real estate development business. Due to the increase in liquidity of restricted stocks since 1990, the business appraiser argued that restricted-stock studies conducted before that date may provide a better proxy for liquidity discounts for this type of investment. Interests in closely held firms are more like letter-stock transactions occurring before the changes in SEC Rule 144 beginning in 1990, when the holding period was reduced from three years to two and later (after 1997) to one. Such firms have little ability to raise capital in public markets due to their small size, and they face high transaction costs. Based on the SEC and other prior 1990 studies, the liquidity discount for this investment was expected to be between 30% and 35%. Pre-IPO studies could push it higher to a range of 40–45%. The appraisal firm argued that the discount for most minority-interest investments tended to fall in the range of 25–45%. Because of the small size of the real estate development business, the liquidity discount is believed by the appraisal firm to be at the higher end of the range.

-What other factors could the appraiser have used to estimate the liquidity discount on the unregistered stock?

In many family owned firms, family influence is exercised by family members holding senior management positions, seats on the board of directors, and through holding super-voting stock (i.e., stock with multiple voting rights).

A minority discount is the reduction in the value of a minority investor's investment because minority owners have little influence in how the firm is managed.

Restricted stock is often issued to employees of privately held firms as a significant portion of their total

compensation. Such stock is similar to other types of common stock except that its sale on the open market is prohibited for a period of time.

Revenue Ruling 59-60 describes the general factors that the IRS and tax courts consider relevant in valuing private businesses. Of the following valuation methods, which do the IRS and tax courts view as the most important?

What are some of the reasons a family-owned or privately-owned business may want to go public? What are some of the reasons that discourage such firms from going public?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)