Exam 14: Applying Financial Modeling

Exam 1: Introduction to Mergers, Acquisitions, and Other Restructuring Activities139 Questions

Exam 2: The Regulatory Environment129 Questions

Exam 3: The Corporate Takeover Market:152 Questions

Exam 4: Planning: Developing Business and Acquisition Plans: Phases 1 and 2 of the Acquisition Process137 Questions

Exam 5: Implementation: Search Through Closing: Phases 310 of the Acquisition Process131 Questions

Exam 6: Postclosing Integration: Mergers, Acquisitions, and Business Alliances138 Questions

Exam 7: Merger and Acquisition Cash Flow Valuation Basics108 Questions

Exam 8: Relative, Asset-Oriented, and Real Option109 Questions

Exam 9: Financial Modeling Basics:97 Questions

Exam 10: Analysis and Valuation127 Questions

Exam 11: Structuring the Deal:138 Questions

Exam 12: Structuring the Deal:125 Questions

Exam 13: Financing the Deal149 Questions

Exam 14: Applying Financial Modeling116 Questions

Exam 15: Business Alliances: Joint Ventures, Partnerships, Strategic Alliances, and Licensing138 Questions

Exam 16: Alternative Exit and Restructuring Strategies152 Questions

Exam 17: Alternative Exit and Restructuring Strategies:118 Questions

Exam 18: Cross-Border Mergers and Acquisitions:120 Questions

Select questions type

Potential sources of value rarely include factors not recorded on a firm's balance sheet.

(True/False)

5.0/5  (39)

(39)

A standalone business is one whose financial statements reflect all the costs of running the business and all of the revenues generated by the business.

(True/False)

4.8/5 (27)

The maximum offer price is equal to the sum of the standalone value (or minimum price) plus some fraction of present value net synergy.

(True/False)

4.9/5 (39)

Underutilized borrowing capacity or significant excess cash balances also can make an acquisition target less attractive.

(True/False)

4.8/5 (49)

The current stock price of the acquiring firm may decline in a share for share exchange due to the potential

dilution in earnings per share.

(True/False)

4.8/5 (42)

Complex models because of their greater sophistication are necessarily more accurate than simple models.

(True/False)

4.8/5 (36)

An acquirer will be more likely to finance a takeover using borrowed funds if

(Multiple Choice)

4.8/5 (36)

For most transactions, the full impact of net synergy will not be realized for many months. Why? What factors could account for the delay?

(Essay)

4.8/5 (34)

Assuming Thermo Fisher would have been able to purchase the firm in a share for share exchange, what would have happened to the EPS in the first year? (Hint: In the form of payment section of the Acquirer Transaction Summary Worksheet, set the percentage of the payment denoted by "% Stock" to 100%. In the Sources and Uses Section, set excess cash, new common shares issued, and convertible preferred shares to zero.)

(Essay)

4.9/5 (50)

Tribune Company Acquires the Times Mirror Corporation

in a Tale of Corporate Intrigue

Background: Oh, What Tangled Webs We Weave. .

.

CEO Mark Willes had reason to be optimistic about the future. Operating profits had grown at a double-digit rate, and earnings per share had grown at a 55% annual rate between 1995 to 1999. Many shareholders appeared to be satisfied. However, some were not. Although pleased with the improvement in profitability, they were concerned about the long-term growth prospects of the firm. Reflecting this disenchantment, Times Mirror's largest shareholder, the Chandler family, was contemplating the sale of the company and along with it the crown jewel Los Angeles Times. It had been assumed for years that the Chandler family trusts made a sale of Times Mirror out of the question. The Chandler's super voting stock (i.e., stock with multiple voting rights) allowed them to exert a disproportionate influence on corporate decisions. The Chandler Trusts controlled more than two-thirds of voting shares, although the family owned only about 28% of the total shares of the outstanding stock.

In May 1999 the Tribune Chairman John Madigan contacted Willes and made an offer for the company, but Willes, with the help of his then-chief financial officer (CFO), Thomas Unterman, made it clear to Madigan that the company was not for sale. What Willes did not realize was that Unterman soon would be serving in a dual role as CFO and financial adviser to the Chandlers and that he would eventually step down from his position at Times Mirror to work directly for the family. In his dual role, he worked without Willes' knowledge to structure the deal with the Tribune.

Following months of secret negotiations, the Chicago-based Tribune Company and the Times Mirror Corporation announced a merger of the two companies in a cash and stock deal valued at approximately $7.2 billion, including $5.7 billion in equity and $1.5 billion in assumed debt. The transaction, announced March 13, 2000, created a media giant that has national reach and a major presence in 18 of the nation's top 30 U.S. markets, including New York, Los Angeles, and Chicago. The combined company has 22 television stations, four radio stations, and 11 daily newspapers-including the Los Angeles Times, the nation's largest metropolitan daily newspaper and flagship of the Times Mirror chain.

Transaction Terms: Tribune Shareholders Get Choice of Cash or Stock

The Tribune agreed to buy 48% of the outstanding Times Mirror stock, about 28 million shares, through a tender offer. After completion of the tender offer, each remaining Times Mirror share would be exchanged for 2.5 shares of Tribune stock. Under the terms of the transaction, Times Mirror shareholders could elect to receive $95 in cash or 2.5 shares of Tribune common stock in exchange for each share of Times Mirror stock. Holders of 27.2 million shares of Times Mirror stock elected to receive Tribune stock, whereas holders of 10.6 million elected to receive cash. Because the amount of cash offered in the merger was limited and the cash election was oversubscribed, Times Mirror shareholders electing to receive cash actually received a combination of cash and stock on a pro rata basis (Table 1).

Table 1. Times Mirror Transaction Terms As of June 12,2000 Transaction Value Times Mirror Shares Outstanding @ 3/13/00 59.700.000 No. of Times Mirror Shares Exchanged for 2.3 Shares of Tribune Stock 27,238,253 \ 2,587,634,03 No. of Times Mirror Shares Exchanged for Cash 10,648,318 \ 1,011,536,96 Times Mirror Shares Outstanding after Tender Offer 21,813,429 No. of New Tribune Shares Issued for Remaining Times Mirror Shares 54,533,57 \ 2,072,275,774 Equity Value of Offer \ 5,671,446,777 Market Value of Times Mirror on Merger Announcement Date \ 2,805,900,000 Premium 102\%

27,238,253\times2.5\times\ 38/ share of Tribune stock. \ 41.70 in cash +1.4025 shares of Tribune stock \times\ 38 per share for each Times Mirror shareremaining \times 10,648,318 . Equals 2.5 shares \times21,813,429\times\ 38 per Tribune share. Times Mirror share price on announcement date of \ 47 times 59,700,000 . The total number of new Tribute shares issued equals 27,238,318\times2.5+10,648,318\times2.5+54,533,573 or 137,537,013 . Newspaper Advertising Revenues Continue to Shrink

Most U.S. newspapers are mired in the mature or declining phase of their product life cycle. For the past half-century, newspapers have watched their portion of the advertising market shrink because of increased competition from radio and television. By the early 1990s, all major media began taking a significant hit in their advertising revenue streams as businesses discovered that direct mail could target their message more precisely. Moreover, consolidation among major retailers further reduced the size of advertising dollar pool. The same has happened with numerous large supermarket chain mergers. Newspaper advertising revenues also have been threatened by increasing competition from advertising and editorial content delivered on the internet. Finally, newspapers simply have become less attractive places to advertise as readership continues to decline as a result of an aging population and new generations that do not see newspapers as relevant.

Times Mirror: A Largely Traditional Business Model

As essentially a traditional newspaper, Times Mirror publishes five metropolitan and two suburban daily newspapers, a variety of magazines, and professional information such as flight maps for commercial airline pilots. The Los Angeles Times, a southern California institution founded in 1881, is Times Mirror's largest holding and operates some two dozen expensive foreign news bureaus-more than any other newspaper in the country. The Los Angeles Times has more than 1200 Los Angeles Times reporters and editors around the world (CNNfn, March 13, 2000).

Tribune Company Profile: The Face of New Media?

Unlike the Times Mirror, Tribune has built its strategy around four business groups: broadcasting, publishing, education, and interactive. The Tribune is also an equity investor in America Online and other leading internet companies, underscoring the company's commitment to new-media technologies. Applying leading edge new-media technology has allowed the Tribune to transform they way it does business, and the technology commitment creates the opportunity for future growth. The internet has been the greatest driver for change, and the Tribune's interactive business group continues to focus on capitalizing on emerging Web technologies. Throughout the company, new technologies have been applied aggressively to create new products, improve existing products, and make operations more efficient. The Tribune's non-newspaper revenues accounted for more than half of its earnings by 2000.

Anticipated Synergy

Cost Savings: Opportunities Abound

Cost savings are expected because of the closing of selected foreign and domestic news bureaus, a reduction in the cost of newsprint through greater volume purchases, the closing of the Times Mirror corporate headquarters, and elimination of corporate staff. Such savings are expected to reach $200 million per year (Table 2).

Table 2. Annual Merge-Related Cost Savings Source of Value Annual Savings Bureau Closings \ 73,000,000 Newsprint Savings \ 93,000,000 Other Office Closings (e.g., Corporate Office in Los Angeles) \ 34,000,000 Total Annual Savings \ 200,000,000

Assumes Tribune will close overlapping bureaus in United States (9) and most of the Times Mirror's foreign bureaus ( 21 abroad).

As a result of bulk purchasing and more favorable terms with different suppliers, of the newsprint expense of the combined companies is expected to be saved.

Layoffs of 120 L.A. Times Mirror Corporate Office personnd at an average salary of and benefits equal to of base salaries. Total payroll expenses equal (i. e., ). Lease, travel and entertainment, and other support expenses added another million.

Source: Moore, Kathryn, Tim Schnabel, and Mark Yemma, "A Media Marriage," paper prepared for Chapman University, EMBA 696, May 18, 2000, p. 9. Revenue: Great Potential . . . But Is It Achievable?

The combined companies will have a major presence in 18 of the nation's top 30 U.S. advertising markets, including New York, Los Angeles, and Chicago. The combined companies provide unprecedented opportunities for advertisers to reach major market consumers in any media form-broadcast, newspapers, or interactive. In addition, the combined companies will benefit consumers by giving them rich and diverse choices for obtaining the news, information, and entertainment they want anytime, anywhere. These factors provide an increased ability to capture national advertising in the most important U.S. population centers. The significantly greater breadth of the combined firm's geographic coverage is expected to boost advertising revenues from about 3% to 6% annually.

Integration Challenges: Cultural Warfare?

Based on the current, traditional culture found at the Los Angeles Times and other Times Mirror properties, integration following the merger was likely to be slow and painful. Concerns among journalists about spreading their talents thin across three or four media-print, television, online, and radio-in the course of a day's work raised the stress level. Although the Tribune has been able to make the transition to a largely multimedia company more rapidly than the more traditional newspapers, it has been costly. For example, development losses in 1999 were $30-35 million at Chicagotribune.com and an estimated $45 million in 2000. The bleeding was expected to continue for some time and to constitute a major distraction for the management of the new company.

Financial Analysis

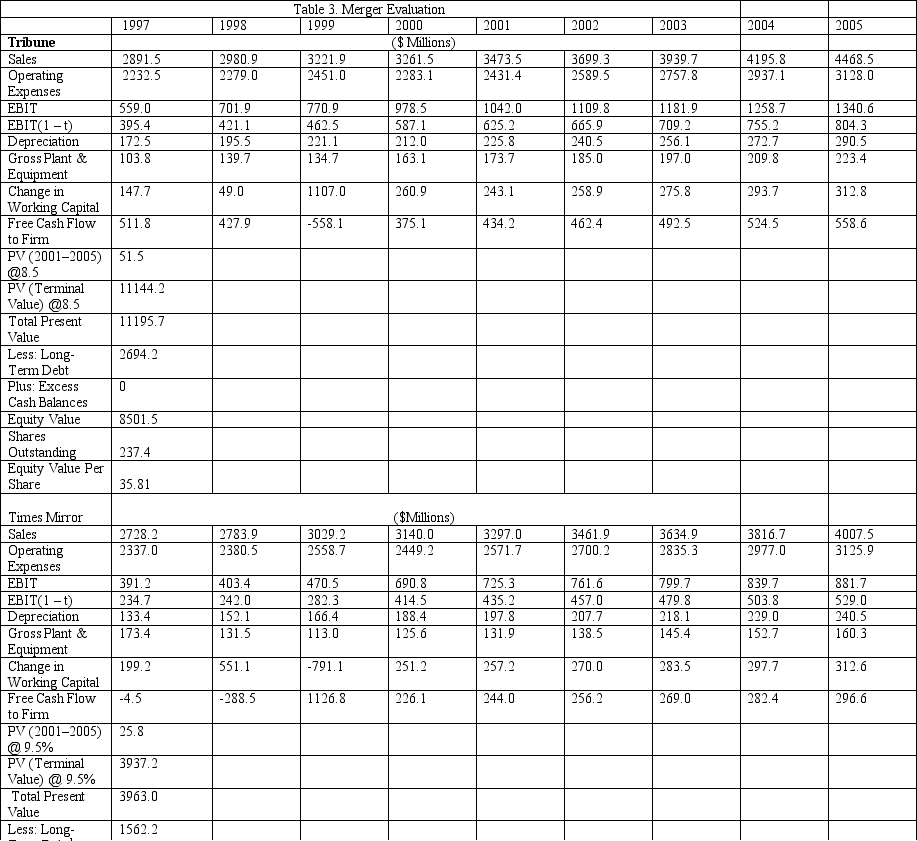

The present values of the Tribune, Times Mirror, and the combined firms are $8.5 billion, $2.4 billion, and $16.5 billion, respectively; the estimated present value of synergy is $5.6 billion (Table 3). This assumes that pretax cost savings are phased in as follows: $25 million in 2000, $100 million in 2001, and $200 million thereafter. The cost savings are net of all expenses related to realizing such savings such as severance, lease buyouts, and legal fees. Table 4 describes how the initial offer price could have been determined and the postmerger distribution of ownership between Times Mirror and Tribune shareholders.

Table 4. Offer Price Determination Tribune Times Mirror Combined Incl. Synergy Value of Synergy Equity Valuations 8501.5 2375.0 16443.7 5567.3 Minimum Offer 2805.9 Maximum Offer Price 8373.2 Actual Offer Price 5671.4 \% Maximum Offer 67.7\% Price Purchase Price Premium 1.02 New Tribune Shares Issued 137.50 Ownership Distribution TM Shareholders 0.37 Tribune Shareholders 0.63

Epilogue

Only time will tell if actual returns to shareholders in the combined Tribune and Times Mirror company exceed the expected financial returns provided in the valuation models in this case study. Times Mirror shareholders earned a substantial 102% purchase price premium over the value of their shares on the day the merger was announced. Some portion of those undoubtedly "cashed out" of their investment following receipt of the new Tribune shares. However, for those former Times Mirror shareholders continuing to hold their Tribune stock and for Tribune shareholders of record on the day the transaction closed, it is unclear if the transaction made good economic sense.

:

-Using the Merger Evaluation table given in the case, determine the estimated equity values of Tribune, Times Mirror and the combined firms. Why is long-term debt deducted from the total present value estimates in order to obtain equity value?

Table 4. Offer Price Determination Tribune Times Mirror Combined Incl. Synergy Value of Synergy Equity Valuations 8501.5 2375.0 16443.7 5567.3 Minimum Offer 2805.9 Maximum Offer Price 8373.2 Actual Offer Price 5671.4 \% Maximum Offer 67.7\% Price Purchase Price Premium 1.02 New Tribune Shares Issued 137.50 Ownership Distribution TM Shareholders 0.37 Tribune Shareholders 0.63

Epilogue

Only time will tell if actual returns to shareholders in the combined Tribune and Times Mirror company exceed the expected financial returns provided in the valuation models in this case study. Times Mirror shareholders earned a substantial 102% purchase price premium over the value of their shares on the day the merger was announced. Some portion of those undoubtedly "cashed out" of their investment following receipt of the new Tribune shares. However, for those former Times Mirror shareholders continuing to hold their Tribune stock and for Tribune shareholders of record on the day the transaction closed, it is unclear if the transaction made good economic sense.

:

-Using the Merger Evaluation table given in the case, determine the estimated equity values of Tribune, Times Mirror and the combined firms. Why is long-term debt deducted from the total present value estimates in order to obtain equity value?

(Essay)

4.8/5 (44)

Using the M&A Valuation & Deal Structuring Model accompanying this text:

a. On the Valuation Worksheet, note the enterprise and equity values for Newco.

b. On the Summary Worksheet under Incremental Sales Synergy, change incremental

revenue by $200 million in the first year and $250 million in the second year and

$350 in the third year.

What is the impact on Newco’s enterprise and equity values? (Hint: See Valuation Worksheet)

Close model but do not save results.

(Short Answer)

4.9/5 (30)

Mars Buys Wrigley in One Sweet Deal

Under considerable profit pressure from escalating commodity prices and eroding market share, Wrigley Corporation, a U.S.-based leader in gum and confectionery products, faced increasing competition from Cadbury Schweppes in the U.S. gum market. Wrigley had been losing market share to Cadbury since 2006. Mars Corporation, a privately owned candy company with annual global sales of $22 billion, sensed an opportunity to achieve sales, marketing, and distribution synergies by acquiring Wrigley Corporation.

On April 28, 2008, Mars announced that it had reached an agreement to merge with Wrigley Corporation for $23 billion in cash. Under the terms of the agreement, which were unanimously approved by the boards of the two firms, shareholders of Wrigley would receive $80 in cash for each share of common stock outstanding, a 28 percent premium to Wrigley's closing share price of $62.45 on the announcement date. The merged firms in 2008 would have a 14.4 percent share of the global confectionary market, annual revenue of $27 billion, and 64,000 employees worldwide. The merger of the two family-controlled firms represents a strategic blow to competitor Cadbury Schweppes's efforts to continue as the market leader in the global confectionary market with its gum and chocolate business. Prior to the announcement, Cadbury had a 10 percent worldwide market share.

As of the September 28, 2008 closing date, Wrigley became a separate stand-alone subsidiary of Mars, with $5.4 billion in sales. The deal is expected to help Wrigley augment its sales, marketing, and distribution capabilities. To provide more focus to Mars's brands in an effort to stimulate growth, Mars would in time transfer its global nonchocolate confectionery sugar brands to Wrigley. Bill Wrigley Jr., who controls 37 percent of the firm's outstanding shares, remained the executive chairman of Wrigley. The Wrigley management team also remained in place after closing.

The combined companies would have substantial brand recognition and product diversity in six growth categories: chocolate, nonchocolate confectionary, gum, food, drinks, and pet care products. While there is little product overlap between the two firms, there is considerable geographic overlap. Mars is located in 100 countries, while Wrigley relies heavily on independent distributors in its growing international distribution network. Furthermore, the two firms have extensive sales forces, often covering the same set of customers.

While mergers among competitors are not unusual, the deal's highly leveraged financial structure is atypical of transactions of this type. Almost 90 percent of the purchase price would be financed through borrowed funds, with the remainder financed largely by a third-party equity investor. Mars's upfront costs would consist of paying for closing costs from its cash balances in excess of its operating needs. The debt financing for the transaction would consist of $11 billion and $5.5 billion provided by J.P. Morgan Chase and Goldman Sachs, respectively. An additional $4.4 billion in subordinated debt would come from Warren Buffet's investment company, Berkshire Hathaway, a nontraditional source of high-yield financing. Historically, such financing would have been provided by investment banks or hedge funds and subsequently repackaged into securities and sold to long-term investors, such as pension funds, insurance companies, and foreign investors. However, the meltdown in the global credit markets in 2008 forced investment banks and hedge funds to withdraw from the high-yield market in an effort to strengthen their balance sheets. Berkshire Hathaway completed the financing of the purchase price by providing $2.1 billion in equity financing for a 9.1 percent ownership stake in Wrigley.

-Why was market share in the confectionery business an important factor in Mars' decision to acquire Wrigley?

(Essay)

4.8/5 (32)

Which of the following is not true about generally accepted accounting principles (GAAP)?

(Multiple Choice)

4.8/5 (39)

Tribune Company Acquires the Times Mirror Corporation

in a Tale of Corporate Intrigue

Background: Oh, What Tangled Webs We Weave. .

.

CEO Mark Willes had reason to be optimistic about the future. Operating profits had grown at a double-digit rate, and earnings per share had grown at a 55% annual rate between 1995 to 1999. Many shareholders appeared to be satisfied. However, some were not. Although pleased with the improvement in profitability, they were concerned about the long-term growth prospects of the firm. Reflecting this disenchantment, Times Mirror's largest shareholder, the Chandler family, was contemplating the sale of the company and along with it the crown jewel Los Angeles Times. It had been assumed for years that the Chandler family trusts made a sale of Times Mirror out of the question. The Chandler's super voting stock (i.e., stock with multiple voting rights) allowed them to exert a disproportionate influence on corporate decisions. The Chandler Trusts controlled more than two-thirds of voting shares, although the family owned only about 28% of the total shares of the outstanding stock.

In May 1999 the Tribune Chairman John Madigan contacted Willes and made an offer for the company, but Willes, with the help of his then-chief financial officer (CFO), Thomas Unterman, made it clear to Madigan that the company was not for sale. What Willes did not realize was that Unterman soon would be serving in a dual role as CFO and financial adviser to the Chandlers and that he would eventually step down from his position at Times Mirror to work directly for the family. In his dual role, he worked without Willes' knowledge to structure the deal with the Tribune.

Following months of secret negotiations, the Chicago-based Tribune Company and the Times Mirror Corporation announced a merger of the two companies in a cash and stock deal valued at approximately $7.2 billion, including $5.7 billion in equity and $1.5 billion in assumed debt. The transaction, announced March 13, 2000, created a media giant that has national reach and a major presence in 18 of the nation's top 30 U.S. markets, including New York, Los Angeles, and Chicago. The combined company has 22 television stations, four radio stations, and 11 daily newspapers-including the Los Angeles Times, the nation's largest metropolitan daily newspaper and flagship of the Times Mirror chain.

Transaction Terms: Tribune Shareholders Get Choice of Cash or Stock

The Tribune agreed to buy 48% of the outstanding Times Mirror stock, about 28 million shares, through a tender offer. After completion of the tender offer, each remaining Times Mirror share would be exchanged for 2.5 shares of Tribune stock. Under the terms of the transaction, Times Mirror shareholders could elect to receive $95 in cash or 2.5 shares of Tribune common stock in exchange for each share of Times Mirror stock. Holders of 27.2 million shares of Times Mirror stock elected to receive Tribune stock, whereas holders of 10.6 million elected to receive cash. Because the amount of cash offered in the merger was limited and the cash election was oversubscribed, Times Mirror shareholders electing to receive cash actually received a combination of cash and stock on a pro rata basis (Table 1).

Table 1. Times Mirror Transaction Terms As of June 12,2000 Transaction Value Times Mirror Shares Outstanding @ 3/13/00 59.700.000 No. of Times Mirror Shares Exchanged for 2.3 Shares of Tribune Stock 27,238,253 \ 2,587,634,03 No. of Times Mirror Shares Exchanged for Cash 10,648,318 \ 1,011,536,96 Times Mirror Shares Outstanding after Tender Offer 21,813,429 No. of New Tribune Shares Issued for Remaining Times Mirror Shares 54,533,57 \ 2,072,275,774 Equity Value of Offer \ 5,671,446,777 Market Value of Times Mirror on Merger Announcement Date \ 2,805,900,000 Premium 102\%

27,238,253\times2.5\times\ 38/ share of Tribune stock. \ 41.70 in cash +1.4025 shares of Tribune stock \times\ 38 per share for each Times Mirror shareremaining \times 10,648,318 . Equals 2.5 shares \times21,813,429\times\ 38 per Tribune share. Times Mirror share price on announcement date of \ 47 times 59,700,000 . The total number of new Tribute shares issued equals 27,238,318\times2.5+10,648,318\times2.5+54,533,573 or 137,537,013 . Newspaper Advertising Revenues Continue to Shrink

Most U.S. newspapers are mired in the mature or declining phase of their product life cycle. For the past half-century, newspapers have watched their portion of the advertising market shrink because of increased competition from radio and television. By the early 1990s, all major media began taking a significant hit in their advertising revenue streams as businesses discovered that direct mail could target their message more precisely. Moreover, consolidation among major retailers further reduced the size of advertising dollar pool. The same has happened with numerous large supermarket chain mergers. Newspaper advertising revenues also have been threatened by increasing competition from advertising and editorial content delivered on the internet. Finally, newspapers simply have become less attractive places to advertise as readership continues to decline as a result of an aging population and new generations that do not see newspapers as relevant.

Times Mirror: A Largely Traditional Business Model

As essentially a traditional newspaper, Times Mirror publishes five metropolitan and two suburban daily newspapers, a variety of magazines, and professional information such as flight maps for commercial airline pilots. The Los Angeles Times, a southern California institution founded in 1881, is Times Mirror's largest holding and operates some two dozen expensive foreign news bureaus-more than any other newspaper in the country. The Los Angeles Times has more than 1200 Los Angeles Times reporters and editors around the world (CNNfn, March 13, 2000).

Tribune Company Profile: The Face of New Media?

Unlike the Times Mirror, Tribune has built its strategy around four business groups: broadcasting, publishing, education, and interactive. The Tribune is also an equity investor in America Online and other leading internet companies, underscoring the company's commitment to new-media technologies. Applying leading edge new-media technology has allowed the Tribune to transform they way it does business, and the technology commitment creates the opportunity for future growth. The internet has been the greatest driver for change, and the Tribune's interactive business group continues to focus on capitalizing on emerging Web technologies. Throughout the company, new technologies have been applied aggressively to create new products, improve existing products, and make operations more efficient. The Tribune's non-newspaper revenues accounted for more than half of its earnings by 2000.

Anticipated Synergy

Cost Savings: Opportunities Abound

Cost savings are expected because of the closing of selected foreign and domestic news bureaus, a reduction in the cost of newsprint through greater volume purchases, the closing of the Times Mirror corporate headquarters, and elimination of corporate staff. Such savings are expected to reach $200 million per year (Table 2).

Table 2. Annual Merge-Related Cost Savings Source of Value Annual Savings Bureau Closings \ 73,000,000 Newsprint Savings \ 93,000,000 Other Office Closings (e.g., Corporate Office in Los Angeles) \ 34,000,000 Total Annual Savings \ 200,000,000

Assumes Tribune will close overlapping bureaus in United States (9) and most of the Times Mirror's foreign bureaus ( 21 abroad).

As a result of bulk purchasing and more favorable terms with different suppliers, of the newsprint expense of the combined companies is expected to be saved.

Layoffs of 120 L.A. Times Mirror Corporate Office personnd at an average salary of and benefits equal to of base salaries. Total payroll expenses equal (i. e., ). Lease, travel and entertainment, and other support expenses added another million.

Source: Moore, Kathryn, Tim Schnabel, and Mark Yemma, "A Media Marriage," paper prepared for Chapman University, EMBA 696, May 18, 2000, p. 9. Revenue: Great Potential . . . But Is It Achievable?

The combined companies will have a major presence in 18 of the nation's top 30 U.S. advertising markets, including New York, Los Angeles, and Chicago. The combined companies provide unprecedented opportunities for advertisers to reach major market consumers in any media form-broadcast, newspapers, or interactive. In addition, the combined companies will benefit consumers by giving them rich and diverse choices for obtaining the news, information, and entertainment they want anytime, anywhere. These factors provide an increased ability to capture national advertising in the most important U.S. population centers. The significantly greater breadth of the combined firm's geographic coverage is expected to boost advertising revenues from about 3% to 6% annually.

Integration Challenges: Cultural Warfare?

Based on the current, traditional culture found at the Los Angeles Times and other Times Mirror properties, integration following the merger was likely to be slow and painful. Concerns among journalists about spreading their talents thin across three or four media-print, television, online, and radio-in the course of a day's work raised the stress level. Although the Tribune has been able to make the transition to a largely multimedia company more rapidly than the more traditional newspapers, it has been costly. For example, development losses in 1999 were $30-35 million at Chicagotribune.com and an estimated $45 million in 2000. The bleeding was expected to continue for some time and to constitute a major distraction for the management of the new company.

Financial Analysis

The present values of the Tribune, Times Mirror, and the combined firms are $8.5 billion, $2.4 billion, and $16.5 billion, respectively; the estimated present value of synergy is $5.6 billion (Table 3). This assumes that pretax cost savings are phased in as follows: $25 million in 2000, $100 million in 2001, and $200 million thereafter. The cost savings are net of all expenses related to realizing such savings such as severance, lease buyouts, and legal fees. Table 4 describes how the initial offer price could have been determined and the postmerger distribution of ownership between Times Mirror and Tribune shareholders.

Table 4. Offer Price Determination Tribune Times Mirror Combined Incl. Synergy Value of Synergy Equity Valuations 8501.5 2375.0 16443.7 5567.3 Minimum Offer 2805.9 Maximum Offer Price 8373.2 Actual Offer Price 5671.4 \% Maximum Offer 67.7\% Price Purchase Price Premium 1.02 New Tribune Shares Issued 137.50 Ownership Distribution TM Shareholders 0.37 Tribune Shareholders 0.63

Epilogue

Only time will tell if actual returns to shareholders in the combined Tribune and Times Mirror company exceed the expected financial returns provided in the valuation models in this case study. Times Mirror shareholders earned a substantial 102% purchase price premium over the value of their shares on the day the merger was announced. Some portion of those undoubtedly "cashed out" of their investment following receipt of the new Tribune shares. However, for those former Times Mirror shareholders continuing to hold their Tribune stock and for Tribune shareholders of record on the day the transaction closed, it is unclear if the transaction made good economic sense.

:

-In your judgment, did it make good strategic sense to combine the Tribune and Times Mirror corporations? Why? / Why not?

(Essay)

4.7/5 (40)

The share exchange ratio is defined as offer price divided by the target firm's current share price. True or False

(True/False)

4.8/5 (28)

A target firm's high employee turnover is often considered a destroyer of value.

(True/False)

4.8/5 (42)

Mark Fisher, CEO of Thermo Fisher, asked rhetorically what if synergy were not realized as quickly and in the amount expected. How patient would shareholders be if the projected impact on earnings per share was not realized? Assume that the integration effort is far more challenging than anticipated and that only one-fourth of the expected SG&A savings, margin improvement, and revenue synergy are realized. Furthermore, assume that actual integration expenses (shown on Newco's Assumptions Worksheet) due to the unanticipated need to upgrade and co-locate research and development facilities and to transfer hundreds of staff are $150 million in 2014, $150 million in 2015, $100 million in 2016, and $50 million in 2017. The model output resulting from these assumption changes is called the Impaired Integration Case.

What is the impact on Thermo Fisher's earning per share (including Life Tech) and the net present value of the combined firms? Compare the difference between the model "Base Case" and the model output from the "Impaired Integration Case" resulting from making the changes indicated in this question. (Hints: In the Synergy Section of the Acquirer (Thermo Fisher) Worksheet, reduce the synergy inputs for each year between 2014 and 2016 by seventy-five percent and allow them to remain at those levels through 2018.

New Synergy Inputs Year SG\&A Synergies Gross Nargin Improvement Incremental Sales Revenue 2014 2.5 18.75 1.25 2015 5.0 50.0 5.0 2016 6.25 56.25 6.25 On the Newco Assumptions Worksheet, change the integration expense figures to reflect the new numbers for 2014, 2015, 2016, and 2017.).

(Essay)

4.8/5 (40)

The present value of net synergy is the difference between the present value of projected cash flows from sources and destroyers of value.

(True/False)

4.8/5 (34)

Which of the following is not true of share exchange ratios?

(Multiple Choice)

4.8/5 (41)

The most common sources of value include potential cost savings resulting from all of the following except for which of the following:

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)