Exam 12: Structuring the Deal:

Exam 1: Introduction to Mergers, Acquisitions, and Other Restructuring Activities139 Questions

Exam 2: The Regulatory Environment129 Questions

Exam 3: The Corporate Takeover Market:152 Questions

Exam 4: Planning: Developing Business and Acquisition Plans: Phases 1 and 2 of the Acquisition Process137 Questions

Exam 5: Implementation: Search Through Closing: Phases 310 of the Acquisition Process131 Questions

Exam 6: Postclosing Integration: Mergers, Acquisitions, and Business Alliances138 Questions

Exam 7: Merger and Acquisition Cash Flow Valuation Basics108 Questions

Exam 8: Relative, Asset-Oriented, and Real Option109 Questions

Exam 9: Financial Modeling Basics:97 Questions

Exam 10: Analysis and Valuation127 Questions

Exam 11: Structuring the Deal:138 Questions

Exam 12: Structuring the Deal:125 Questions

Exam 13: Financing the Deal149 Questions

Exam 14: Applying Financial Modeling116 Questions

Exam 15: Business Alliances: Joint Ventures, Partnerships, Strategic Alliances, and Licensing138 Questions

Exam 16: Alternative Exit and Restructuring Strategies152 Questions

Exam 17: Alternative Exit and Restructuring Strategies:118 Questions

Exam 18: Cross-Border Mergers and Acquisitions:120 Questions

Select questions type

Which of the following is not true of taxable asset purchases?

Free

(Multiple Choice)

5.0/5  (32)

(32)

Correct Answer: Verified

Verified

A

The convertible debt is described as a "stock lockup." How does the convertible debt discourage other interested parties from bidding on Sprint?

Free

(Essay)

4.7/5 (41)

Correct Answer:Verified

The convertible debt enables SoftBank to acquire 16.2% of Sprint's stock even if the merger is not completed at $5.25 per share, well below the firm's $7.25 price trading on public exchanges. Any new acquirer would have a potential competitor as a sizeable shareholder.

Which of the following is true about purchase accounting?

Free

(Multiple Choice)

4.8/5 (38)

Correct Answer:Verified

E

Acquiring Company buys 100% of Target Company's equity for $5,000,000 in cash. As an analyst, you are given the

following pre-merger balance sheets for the two companies. Assuming plant and equipment is revalued upward by $500,000,

what will be the combined companies' shareholders' equity plus total liabilities? What is the difference between Acquiring

Company's shareholders' equity and the shareholders' equity of the combined companies? Show your work.

Balance Sheets (Dollars) Acquiring Company Target Company CurrentAssets 600,000 800,000 Plant and Equigment 1,200,000 1,500,000 Tatal Assets 1,800,000 2,300,000 Long-Tem Debt 500,000 300,000 Sharehalder's' Equity 1,300,000 2,000,000 Shareholder' Equity + Total 1,800,000 2.300,000 Limbilities

(Essay)

4.9/5 (41)

Type A reorganizations are generally viewed as the least flexible of the various types of tax-free reorganizations.

(True/False)

4.8/5 (33)

Which of the following are not true of net operating loss carrybacks and carryforwards?

(Multiple Choice)

4.9/5 (38)

Subchapter S Corporation shareholders, and LLC members, are taxed at their personal tax rates.

(True/False)

4.8/5 (33)

For financial reporting purposes, goodwill resulting from an acquisition

(Multiple Choice)

4.9/5 (34)

A type C reorganization is a stock-for-assets reorganization with the requirement that at least 50% of the FMV of the target's assets, as well as the assumption of certain specified liabilities, are acquired solely in exchange for voting stock.

(True/False)

5.0/5 (32)

The disadvantages of the forward triangular merger may include the requirement of the buyer to get shareholder approval.

(True/False)

4.9/5 (35)

According to Section 338 of the U.S. tax code, a purchaser of 80% or more of the assets of the target may elect to treat the acquisition as if it were an acquisition of the target's assets for tax purposes.

(True/False)

4.8/5 (36)

In a taxable purchase of target stock with cash, the target firm does not restate (i.e., revalue) its assets and liabilities for tax purposes to reflect the amount that the acquirer paid for the shares of common stock. Rather, the tax basis (i.e., their value on the target's financial statements) of assets and liabilities of the target before the acquisition carries over to the acquirer after the acquisition.

(True/False)

4.9/5 (41)

Teva Pharmaceuticals Buys Barr Pharmaceuticals to Create a Global Powerhouse

Foreign acquirers often choose to own U.S. firms in limited liability corporations.

American Depository Shares (ADSs) often are used by foreign buyers, since their shares do not trade directly on U.S. stock exchanges.

Despite a significant regulatory review, the firms employed a fixed share-exchange ratio in calculating the purchase price, leaving each at risk of Teva share price changes.

_____________________________________________________________________________________

On December 23, 2008, Teva Pharmaceuticals Ltd. completed its acquisition of U.S.-based Barr Pharmaceuticals Inc. The merged businesses created a firm with a significant presence in 60 countries worldwide and about $14 billion in annual sales. Teva Pharmaceutical Industries Ltd. is headquartered in Israel and is the world's leading generic-pharmaceuticals company. The firm develops, manufactures, and markets generic and human pharmaceutical ingredients called biologics as well as animal health pharmaceutical products. Over 80% of Teva's revenue is generated in North America and Europe.

Barr is a U.S.-headquartered global specialty pharmaceuticals company that operates in more than 30 countries. Barr's operations are based primarily in North America and Europe, with its key markets being the United States, Croatia, Germany, Poland, and Russia. With annual sales of about $2.5 billion, Barr is engaged primarily in the development, manufacture, and marketing of generic and proprietary pharmaceuticals and is one of the world's leading generic-drug companies. Barr also is involved actively in the development of generic biologic products, an area that Barr believes provides significant prospects for long-term earnings and profitability.

Based on the average closing price of Teva American Depository Shares (ADSs) on NASDAQ on July 16, 2008, the last trading day in the United States before the merger's announcement, the total purchase price was approximately $7.4 billion, consisting of a combination of Teva shares and cash. Each ADS represents one ordinary share of Teva deposited with a custodian bank. As a result of the transaction, Barr shareholders owned approximately 7.3% of Teva after the merger. The merger agreement provides that each share of Barr common stock issued and outstanding immediately prior to the effective time of the merger was to be converted into the right to receive 0.6272 ordinary shares of Teva, which trade in the United States as American Depository Shares, and $39.90 in cash. The 0.6272 represents the share-exchange ratio stipulated in the merger agreement. The value of the portion of the merger consideration comprising Teva ADSs could have changed between signing and closing, because the share-exchange ratio was fixed, per the merger agreement.

ADSs may be issued in uncertificated form or certified as an American Depositary Receipt, or ADR. ADRs provide evidence that a specified number of ADSs have been deposited by Teva commensurate with the number of new ADSs issued to Barr shareholders.

By most measures, the offer price for Barr shares constituted an attractive premium over the value of Barr shares prior to the merger announcement. Based on the closing price of a Teva ADS on the NASDAQ Stock Exchange on July 16, 2008, the consideration for each outstanding share of Barr common stock for Barr shareholders represented a premium of approximately 42% over the closing price of Barr common stock on July 16, 2008, the last trading day in the United States before the merger announcement. Since the merger qualified as a tax-free reorganization under U.S. federal income tax laws, a U.S. holder of Barr common stock generally did not recognize any gain or loss under U.S. federal income tax laws on the exchange of Barr common stock for Teva ADSs. A U.S. holder generally would recognize a gain on cash received in exchange for the holder's Barr common stock.

Teva was motivated to acquire Barr because of the desire to achieve increased economies of scale and scope as well as greater geographic coverage, with significant growth potential in emerging markets. Barr's U.S. generics drug offering in the United States is highly complementary with Teva's and extends Teva's product offering and product development pipeline into new and attractive product categories, such as a substantial women's healthcare business. The merger also is a response to the ongoing global trend of consolidation among the purchasers of pharmaceutical products as governments are increasingly becoming the primary purchaser of generic drugs.

Under the merger agreement, a wholly owned Teva corporate subsidiary, the Boron Acquisition Corp. (i.e., acquisition vehicle), merged with Barr, with Barr surviving the merger as a wholly owned subsidiary of Teva. Immediately following the closing of the merger, Barr was merged into a newly formed limited liability company (i.e., postclosing organization), also wholly owned by Teva, which is the surviving company in the second step of the merger. As such, Barr became a wholly owned subsidiary of Teva and ceased to be traded on the New York Stock Exchange.

The merger agreement contained standard preclosing covenants, in which Barr agreed to conduct its business only in the ordinary course (i.e., as it has historically, in a manner consistent with common business practices) and not to alter any supplier, customer, or employee agreements or declare any dividends or buy back any outstanding stock. Barr also agreed not to engage in one or more transactions or investments or assume any debt exceeding $25 million. The firm also promised not to change any accounting practices in any material way or in a manner inconsistent with generally accepted accounting principles. Barr also committed not to solicit alternative bids from any other possible investors between the signing of the merger agreement and the closing.

Teva agreed that from the period immediately following closing and ending on the first anniversary of closing it would require Barr or its subsidiaries to maintain each compensation and benefit plan in existence prior to closing. All annual base salary and wage rates of each Barr employee would be maintained at no less than the levels in effect before closing. Bonus plans also would be maintained at levels no less favorable than those in existence before the closing of the merger.

The key closing conditions that applied to both Teva and Barr included satisfaction of required regulatory and shareholder approvals, compliance with all prevailing laws, and that no representations and warranties were found to have been breached. Moreover, both parties had to provide a certificate signed by the chief executive officer and the chief financial officer that their firms had performed in all material respects all obligations required to be performed in accordance with the merger agreement prior to the closing date and that neither business had suffered any material damage between the signing and the closing.

The merger agreement had to be approved by a majority of the outstanding voting shares of Barr common stock. Shareholders failing to vote or abstaining were counted as votes against the merger agreement. Shareholders were entitled to vote on the merger agreement if they held Barr common stock at the close of business on the record date, which was October 10, 2008. Since the shares issued by Teva in exchange for Barr's stock had already been authorized and did not exceed 20% of Teva's shares outstanding (i.e., the threshold on some public stock exchanges at which firms are required to obtain shareholder approval), the merger was not subject to a vote of Teva's shareholders.

Teva and Barr each notified the U.S. Federal Trade Commission and the Antitrust Division of the U.S. Department of Justice of the proposed deal in order to comply with prevailing antitrust regulations. Each party subsequently received a "second request for information" from the FTC, whose effect was to extend the HSR waiting period another 30 days. Teva and Barr received FTC and Justice Department approval once potential antitrust concerns had been dispelled. Given the global nature of the merger, the two firms also had to file with the European Union Antitrust Commission as well as with other country regulatory authorities.

-Mergers of businesses with operations in many countries must seek approval from a number of regulatory agencies. How might this affect the time between the signing of the agreement and the actual closing? How might the ability to realize synergy following the merger of the two businesses be affected by actions required by the regulatory authorities before granting their approval? Be specific.

(Essay)

4.8/5 (24)

Cablevision Uses Tax Benefits to Help Justify the Price Paid for Bresnan Communications

In mid-2010, Cablevision Systems announced that it had reached an agreement to buy privately owned Bresnan Communications for $1.37 billion in a cash for stock deal. CVS’ motivation for the deal reflected the board’s belief that the firm’s shares were undervalued and their desire to expand coverage into the western United States.

CVS is the most profitable cable operator in the industry in terms of operating profit margins, due primarily to the firm’s heavily concentrated customer base in the New York City area. Critics immediately expressed concern that the acquisition would provide few immediate cost savings and relied almost totally on increasing the amount of revenue generated by Bresnan’s existing customers.

CVS saw an opportunity to gain market share from satellite TV operators providing services in BC’s primary geographic market. Bresnan, the nation’s 13th largest cable operator, serves Colorado, Montana, Wyoming, and Utah. CVS believes it can sell bundles of services, including Internet and phone services, to current Bresnan customers. Bresnan’s primary competition comes from DirecTV and DISH Network, which cannot offer phone and Internet access services.

In order to gain shareholder support, CVS announced a $500 million share repurchase to placate shareholders seeking a return of cash. The deal was financed by a $1 billion nonrecourse loan and $370 in cash from Cablevision. CVS points out that the firm’s direct investment in BC will be more than offset by tax benefits resulting from the structure of the deal in which both Cablevision and Bresnan agreed to treat the purchase of Bresnan’s stock as an asset purchase for tax reporting purposes (i.e., a 338 election). Consequently, CVS will be able to write up the net acquired Bresnan assets to their fair market value and use the resulting additional depreciation to generate significant future tax savings. Such future tax savings are estimated by CVS to have a net present value of approximately $400 million

Discussion Question:

1. How is the 338 election likely to impact Cablevision System’s earnings per share immediately following closing? Why?

2. As an analyst, how would you determine the impact of the anticipated tax benefits on the value of the firm?

3. What is the primary risk to realizing the full value of the anticipated tax benefits?

Teva Pharmaceuticals Buys Ivax Corporation

Teva Pharmaceutical Industries’, a manufacturer and distributor of generic drugs, takeover of Ivax Corp for $7.4 billion created the world's largest manufacturer of generic drugs. For Teva, based in Israel, and Ivax, headquartered in Miami, the merger eliminated a large competitor and created a distribution chain that spans 50 countries.

To broaden the appeal of the proposed merger, Teva offered Ivax shareholders the option to receive for each of their shares either 0.8471 of American depository receipts (ADRs) representing Teva shares or $26 in cash. ADRs represent the receipt given to U.S. investors for the shares of a foreign-based corporation held in the vault of a U.S. bank. Ivax shareholders wanting immediate liquidity chose to exchange their shares for cash, while those wanting to participate in future appreciation of Teva stock exchanged their shares for Teva shares.

At closing, each outstanding share of Ivax common stock was cancelled. Each cancelled share represented the right to receive either of these two previously mentioned payment options. The merger agreement also provided for the acquisition of Ivax by Teva through a merger of Merger Sub, a newly formed and wholly-owned subsidiary of Teva, into Ivax. As the surviving corporation, Ivax would be a wholly-owned subsidiary of Teva. The merger involving the exchange of Teva ADRs for Ivax shares was considered as tax-free for those Ivax shareholders receiving Teva stock under U.S. law as it consisted of predominately acquirer shares.

Case Study. JDS Uniphase–SDL Merger Results in Huge Write-Off

What started out as the biggest technology merger in history up to that point saw its value plummet in line with the declining stock market, a weakening economy, and concerns about the cash-flow impact of actions the acquirer would have to take to gain regulatory approval. The $41 billion mega-merger, proposed on July 10, 2000, consisted of JDS Uniphase (JDSU) offering 3.8 shares of its stock for each share of SDL’s outstanding stock. This constituted an approximate 43% premium over the price of SDL’s stock on the announcement date. The challenge facing JDSU was to get Department of Justice (DoJ) approval of a merger that some feared would result in a supplier (i.e., JDS Uniphase–SDL) that could exercise enormous pricing power over the entire range of products from raw components to packaged products purchased by equipment manufacturers. The resulting regulatory review lengthened the period between the signing of the merger agreement between the two companies and the actual closing to more than 7 months. The risk to SDL shareholders of the lengthening of the time between the determination of value and the actual receipt of the JDSU shares at closing was that the JDSU shares could decline in price during this period.

Given the size of the premium, JDSU’s management was unwilling to protect SDL’s shareholders from this possibility by providing a “collar” within which the exchange ratio could fluctuate. The absence of a collar proved particularly devastating to SDL shareholders, which continued to hold JDSU stock well beyond the closing date. The deal that had been originally valued at $41 billion when first announced more than 7 months earlier had fallen to $13.5 billion on the day of closing.

JDSU manufactures and distributes fiber-optic components and modules to telecommunication and cable systems providers worldwide. The company is the dominant supplier in its market for fiber-optic components. In 1999, the firm focused on making only certain subsystems needed in fiber-optic networks, but a flurry of acquisitions has enabled the company to offer complementary products. JDSU’s strategy is to package entire systems into a single integrated unit. This would reduce the number of vendors that fiber optic network firms must deal with when purchasing systems that produce the light that is transmitted over fiber. SDL’s products, including pump lasers, support the transmission of data, voice, video, and internet information over fiber-optic networks by expanding their fiber-optic communications networks much more quickly and efficiently than would be possible using conventional electronic and optical technologies. SDL had approximately 1700 employees and reported sales of $72 million for the quarter ending March 31, 2000.

As of July 10, 2000, JDSU had a market value of $74 billion with 958 million shares outstanding. Annual 2000 revenues amounted to $1.43 billion. The firm had $800 million in cash and virtually no long-term debt. Including one-time merger-related charges, the firm recorded a loss of $905 million. With its price-to-earnings (excluding merger-related charges) ratio at a meteoric 440, the firm sought to use stock to acquire SDL, a strategy that it had used successfully in eleven previous acquisitions. JDSU believed that a merger with SDL would provide two major benefits. First, it would add a line of lasers to the JDSU product offering that strengthened signals beamed across fiber-optic networks. Second, it would bolster JDSU’s capacity to package multiple components into a single product line.

Regulators expressed concern that the combined entities could control the market for a specific type of pump laser used in a wide range of optical equipment. SDL is one of the largest suppliers of this type of laser, and JDS is one of the largest suppliers of the chips used to build them. Other manufacturers of pump lasers, such as Nortel Networks, Lucent Technologies, and Corning, complained to regulators that they would have to buy some of the chips necessary to manufacture pump lasers from a supplier (i.e., JDSU), which in combination with SDL, also would be a competitor.

As required by the Hart–Scott–Rodino (HSR) Antitrust Improvements Act of 1976, JDSU had filed with the DoJ seeking regulatory approval. On August 24 th, the firm received a request for additional information from the DoJ, which extended the HSR waiting period. On February 6, JDSU agreed as part of a consent decree to sell a Swiss subsidiary, which manufactures pump laser chips, to Nortel Networks Corporation, a JDSU customer, to satisfy DoJ concerns about the proposed merger. The divestiture of this operation set up an alternative supplier of such chips, thereby alleviating concerns expressed by other manufacturers of pump lasers that they would have to buy such components from a competitor.

On July 9, 2000, the boards of both JDSU and SDL unanimously approved an agreement to merge SDL with a newly formed, wholly owned subsidiary of JDS Uniphase, K2 Acquisition, Inc. K2 Acquisition, Inc. was created by JDSU as the acquisition vehicle to complete the merger. In a reverse triangular merger, K2 Acquisition Inc. was merged into SDL, with SDL as the surviving entity. The post-closing organization consisted of SDL as a wholly owned subsidiary of JDS Uniphase. The form of payment consisted of exchanging JDSU common stock for SDL common shares. The share exchange ratio was 3.8 shares of JDSU stock for each SDL common share outstanding. Instead of a fraction of a share, each SDL stockholder received cash, without interest, equal to dollar value of the fractional share at the average of the closing prices for a share of JDSU common stock for the 5 trading days before the completion of the merger.

Under the rules of the NASDAQ National Market, on which JDSU’s shares are traded, JDSU is required to seek stockholder approval for any issuance of common stock to acquire another firm. This requirement is triggered if the amount issued exceeds 20% of its issued and outstanding shares of common stock and of its voting power. In connection with the merger, both SDL and JDSU received fairness opinions from advisors employed by the firms.

The merger agreement specified that the merger could be consummated when all of the conditions stipulated in the agreement were either satisfied or waived by the parties to the agreement. Both JDSU and SDL were subject to certain closing conditions. Such conditions were specified in the September 7, 2000 S4 filing with the SEC by JDSU, which is required whenever a firm intends to issue securities to the public. The consummation of the merger was to be subject to approval by the shareholders of both companies, the approval of the regulatory authorities as specified under the HSR, and any other foreign antitrust law that applied. For both parties, representations and warranties (statements believed to be factual) must have been found to be accurate and both parties must have complied with all of the agreements and covenants (promises) in all material ways.

The following are just a few examples of the 18 closing conditions found in the merger agreement. The merger is structured so that JDSU and SDL’s shareholders will not recognize a gain or loss for U.S. federal income tax purposes in the merger, except for taxes payable because of cash received by SDL shareholders for fractional shares. Both JDSU and SDL must receive opinions of tax counsel that the merger will qualify as a tax-free reorganization (tax structure). This also is stipulated as a closing condition. If the merger agreement is terminated as a result of an acquisition of SDL by another firm within 12 months of the termination, SDL may be required to pay JDSU a termination fee of $1 billion. Such a fee is intended to cover JDSU’s expenses incurred as a result of the transaction and to discourage any third parties from making a bid for the target firm.

Despite dramatic cost-cutting efforts, the company reported a loss of $7.9 billion for the quarter ending June 31, 2001 and $50.6 billion for the 12 months ending June 31, 2001. This compares to the projected pro forma loss reported in the September 9, 2000 S4 filing of $12.1 billion. The actual loss was the largest annual loss ever reported by a U.S. firm up to that time. The fiscal year 2000 loss included a reduction in the value of goodwill carried on the balance sheet of $38.7 billion to reflect the declining market value of net assets acquired during a series of previous transactions. Most of this reduction was related to goodwill arising from the merger of JDS FITEL and Uniphase and the subsequent acquisitions of SDL, E-TEK, and OCLI..

The stock continued to tumble in line with the declining fortunes of the telecommunications industry such that it was trading as low as $7.5 per share by mid-2001, about 6% of its value the day the merger with SDL was announced. Thus, the JDS Uniphase–SDL merger was marked by two firsts—the largest purchase price paid for a pure technology company and the largest write-off (at that time) in history. Both of these infamous “firsts” occurred within 12 months.

-Why do boards of directors of both acquiring and target companies often obtain so-called "fairness opinions" from outside investment advisors or accounting firms? What valuation methodologies might be employed in constructing these opinions? Should stockholders have confidence in such opinions? Why/why not?

(Essay)

4.9/5 (40)

Which of the following are required for an acquisition to be considered tax-free?

(Multiple Choice)

4.9/5 (29)

For tax purposes, goodwill created after July 1993 may be amortized up to 15 years and is tax deductible. Goodwill booked before July 1993 is also tax deductible.

(True/False)

4.8/5 (44)

From the viewpoint of the seller or target company shareholder, transactions may be tax-free or entirely or partially taxable.

(True/False)

4.8/5 (48)

Johnson & Johnson Uses Financial Engineering to Acquire Synthes Corporation

While tax considerations rarely are the primary motivation for takeovers, they make transactions more attractive.

Tax considerations may impact where and when investments such as M&As are made.

Foreign cash balances give multinational corporations flexibility in financing M&As.

_____________________________________________________________________________________

United States–based Johnson & Johnson (J&J), the world’s largest healthcare products company, employed creative tax strategies in undertaking the biggest takeover in its history. When J&J first announced that it would acquire Swiss medical device maker Synthes for $19.7 million in stock and cash, the firm indicated that the deal would dilute its current shareholders due to the issuance of 204 million new shares. Investors expressed their dismay by pushing the firm’s share price down immediately following the announcement. J&J looked for a way to make the deal more attractive to investors while preserving the composition of the purchase price paid to Synthes’ shareholders (two-thirds stock and the remainder in cash). They could defer the payment of taxes on that portion of the purchase price received in J&J shares until such shares were sold; however, they would incur an immediate tax liability on any cash received.

Having found a loophole in the IRS’s guidelines for utilizing funds held in foreign subsidiaries, J&J was able to make the deal’s financing structure accretive to earnings following closing. In 2011, the IRS had ruled that cash held in foreign operations repatriated to the United States would be considered a dividend paid by the subsidiary to the parent, subject to the appropriate tax rate. Because the United States has the highest corporate tax rate among developed countries, U.S. multinational firms have an incentive to reinvest earnings of their foreign subsidiaries abroad.

With this in mind, J&J used the foreign earnings held by its Irish subsidiary to buy 204 million of its own shares, valued at $12.9 billion, held by Goldman Sachs and JPMorgan, which had previously acquired J&J shares in the open market. The buyback of J&J shares held by these investment banks increased the consolidated firm’s earnings per share. These shares, along with cash, were exchanged for outstanding Synthes’ shares to fund the transaction. J&J also avoided a hefty tax payment by not repatriating these earnings to the United States, where they would have been taxed at a 35% corporate rate rather than the 12% rate in Ireland. Investors reacted favorably, boosting J&J’s share price by more than 2% in mid-2012, when the firm announced the deal would be accretive rather than dilutive. Presumably, the IRS will move to prevent future deals from being financed in a similar manner.

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company (“Merck”) and Schering-Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering-Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms. Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent, respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs under development at Schering-Plough. Furthermore, the deal increases Merck’s international presence, since 70 percent of Schering-Plough’s revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new firm has a product offering that is much more diversified than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it was the acquirer in this transaction. The importance of the latter point is explained in the following section.

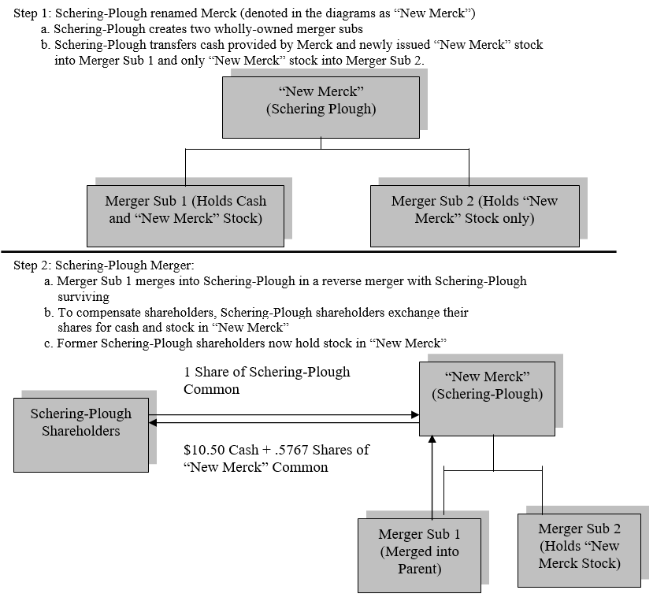

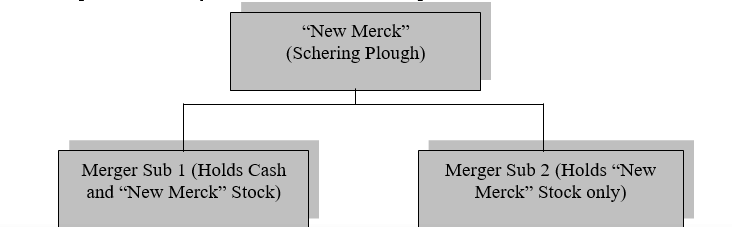

To implement the transaction, Schering-Plough created two merger subsidiaries (i.e., Merger Subs 1 and 2) and moved $10 billion in cash provided by Merck and 1.5 billion new shares (i.e., so-called “New Merck” shares approved by Schering-Plough shareholders) in the combined Schering-Plough and Merck companies into the subsidiaries. Merger Sub 1 was merged into Schering-Plough, with Schering-Plough the surviving firm. Merger Sub 2 was merged with Merck, with Merck surviving as a wholly-owned subsidiary of Schering-Plough. The end result is the appearance that Schering-Plough (renamed Merck) acquired Merck through its wholly-owned subsidiary (Merger Sub 2). In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The “New Merck” is simply Schering-Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering-Plough’s 2008 revenues and about 70 percent of the firm’s international revenues. Consequently, retaining these revenues following the merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these actions occur concurrently.

Step 1: Schering-Plough renamed Merck (denoted in the diagrams as "New Merck")

a. Schering-Plough creates two wholly-owned merger subs

b. Schering-Plough transfers cash provided by Merck and newly issued "New Merck" stock into Merger Sub 1 and only "New Merck" stock into Merger Sub 2.

Step 1: Schering-Plough renamed Merck (denoted in the diagrams as "New Merck")

a. Schering-Plough creates two wholly-owned merger subs

b. Schering-Plough transfers cash provided by Merck and newly issued "New Merck" stock into Merger Sub 1 and only "New Merck" stock into Merger Sub 2.

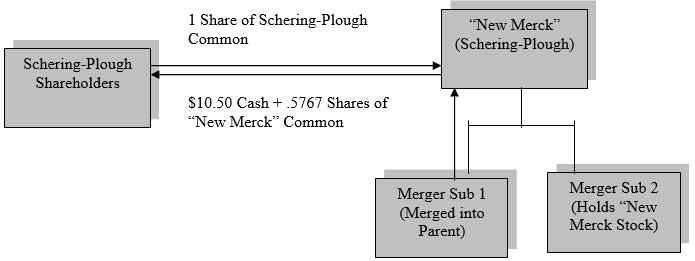

Step 2: Schering-Plough Merger:

a. Merger Sub 1 merges into Schering-Plough in a reverse merger with Schering-Plough surviving

b. To compensate shareholders, Schering-Plough shareholders exchange their shares for cash and stock in "New Merck"

c. Former Schering-Plough shareholders now hold stock in "New Merck"

Step 2: Schering-Plough Merger:

a. Merger Sub 1 merges into Schering-Plough in a reverse merger with Schering-Plough surviving

b. To compensate shareholders, Schering-Plough shareholders exchange their shares for cash and stock in "New Merck"

c. Former Schering-Plough shareholders now hold stock in "New Merck"

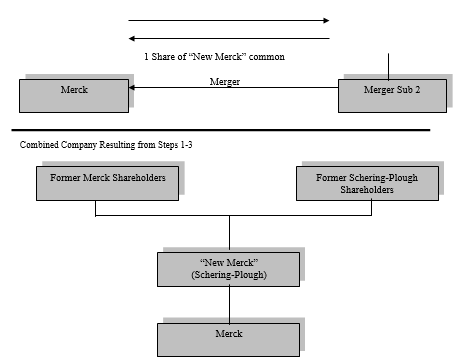

Step 3: Merck Merger:

a. Merger Sub 2 merges into Merck with Merck surviving

b. To compensate shareholders, Merck shareholders exchange their shares for shares in "New Merck"

c. Former shareholders in Merck now hold shares in "New Merck" (i.e., a renamed Schering-Plough)

d, Merger Sub 2, a subsidiary of "New Merck," now owns Merck.

Step 3: Merck Merger:

a. Merger Sub 2 merges into Merck with Merck surviving

b. To compensate shareholders, Merck shareholders exchange their shares for shares in "New Merck"

c. Former shareholders in Merck now hold shares in "New Merck" (i.e., a renamed Schering-Plough)

d, Merger Sub 2, a subsidiary of "New Merck," now owns Merck.

In reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck’s chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough’s CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm’s board consists of former Merck directors, with the remainder coming from Schering-Plough’s board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.

-Doy you agree with the argument that the courts should focus on the form or structure of an agreement and not try to interpret the actual intent of the parties to the transaction? Explain your answer.

In reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck’s chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough’s CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm’s board consists of former Merck directors, with the remainder coming from Schering-Plough’s board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.

-Doy you agree with the argument that the courts should focus on the form or structure of an agreement and not try to interpret the actual intent of the parties to the transaction? Explain your answer.

(Essay)

4.7/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)