Exam 18: Standard Costing and Variance Analysis 2: Further Aspects

Exam 1: Introduction to Management Accounting35 Questions

Exam 2: An Introduction to Cost Terms and Concepts65 Questions

Exam 3: Cost Assignment52 Questions

Exam 4: Accounting Entries for a Job Costing System25 Questions

Exam 5: Process Costing56 Questions

Exam 6: Joint and By-Product Costing65 Questions

Exam 7: Income Effects of Alternative Cost Accumulation Systems42 Questions

Exam 8: Cost-Volume-Profit Analysis59 Questions

Exam 9: Measuring Relevant Costs and Revenues for Decision-Making77 Questions

Exam 10: Activity-Based Costing40 Questions

Exam 11: Activity-Based Costing56 Questions

Exam 12: Decision-Making Under Conditions of Risk and Uncertainty15 Questions

Exam 13: Capital Investment Decisions: Appraisal Methods60 Questions

Exam 14: Capital Investment Decisions: the Impact of Capital Rationing, Taxation, Inflation and Risk22 Questions

Exam 15: The Budgeting Process76 Questions

Exam 16: Management Control Systems60 Questions

Exam 17: Standard Costing and Variance Analysis 181 Questions

Exam 18: Standard Costing and Variance Analysis 2: Further Aspects12 Questions

Exam 19: Divisional Financial Performance Measures48 Questions

Exam 20: Transfer Pricing in Divisionalized Companies43 Questions

Exam 21: Strategic Cost Management101 Questions

Exam 22: Strategic Performance Management29 Questions

Exam 23: Cost Estimation and Cost Behaviour59 Questions

Exam 24: Quantitative Models for the Planning and Control of Inventories40 Questions

Exam 25: The Application of Linear Programming to Management Accounting30 Questions

Select questions type

Figure 18-4

Regis Ltd. uses two materials in the production of its product. The materials, X and Y, have the following standards: Material Standard Mix Standard Unit Price Standard Cost 3,500 units £1.00 per unit £3,500 1,500 units 3.00 per unit £4,500 Yield 4,000 units During April, the following actual production information was provided: Material Actual Mix 30,000 units 20,000 units Yield 36,000 units

-Refer to Figure 18-4. What is the materials usage variance?

Free

(Multiple Choice)

4.8/5  (28)

(28)

Correct Answer: Verified

Verified

D

Figure 18-2

Allende Company has developed capacity standards. Information is as follows for a value-added activity: Activity capacity acquired 60 Activity capacity used 50 Actual activity usage 30 Standard fixed activity rate £2,000

-Refer to Figure 18-2. The unused capacity variance is

Free

(Multiple Choice)

4.8/5 (36)

Correct Answer:Verified

C

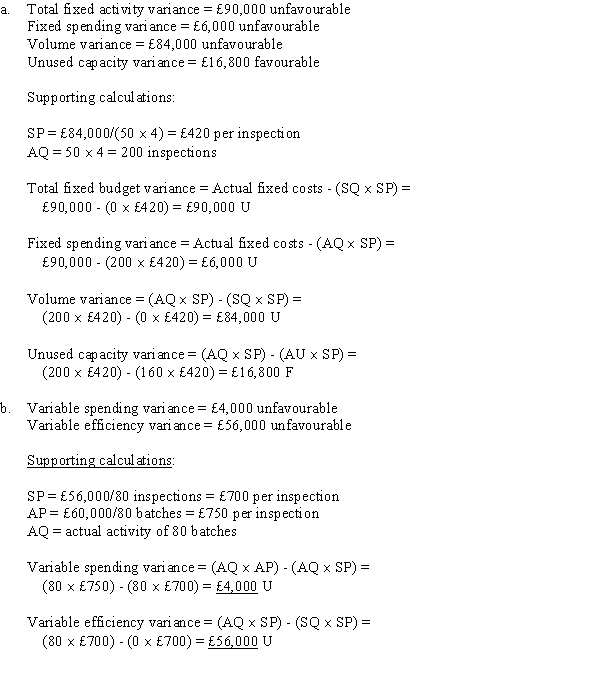

Davis Industries' activity-based performance report revealed that actual inspection costs totaled £225,000 at an actual activity level of 80 inspections. Further analysis of inspection costs revealed the following: Actual Cost Budgeted Cost Inspection costs: Fixed £90,000 £84,000 Variable 60,000 56,000 Fixed inspection costs consist of the salaries of four inspectors, paid £21,000 each. Each inspector is capable of efficiently conducting inspections of 50 batches. Variable inspection costs consist of materials used during the inspections.

a.Calculate the following fixed activity budget variances for inspection:Total fixed activity varianceFixed spending varianceVolume varianceUnused capacity variance

b.Calculate the following variable activity budget variances for inspection:Spending varianceEfficiency variance

Free

(Essay)

4.7/5 (38)

Correct Answer:Verified

Figure 18-4

Regis Ltd. uses two materials in the production of its product. The materials, X and Y, have the following standards: Material Standard Mix Standard Unit Price Standard Cost 3,500 units £1.00 per unit £3,500 1,500 units 3.00 per unit £4,500 Yield 4,000 units During April, the following actual production information was provided: Material Actual Mix 30,000 units 20,000 units Yield 36,000 units

-Refer to Figure 18-4. What is the materials yield variance?

(Multiple Choice)

4.9/5 (33)

Figure 18-4

Regis Ltd. uses two materials in the production of its product. The materials, X and Y, have the following standards: Material Standard Mix Standard Unit Price Standard Cost 3,500 units £1.00 per unit £3,500 1,500 units 3.00 per unit £4,500 Yield 4,000 units During April, the following actual production information was provided: Material Actual Mix 30,000 units 20,000 units Yield 36,000 units

-Refer to Figure 18-4. What is the materials mix variance?

(Multiple Choice)

4.8/5 (37)

Figure 18-3

Pippen Company's activity-based performance report revealed that actual inspection costs totaled £100,000 at an actual activity level of 50 inspections. Further analysis of inspection costs revealed the following: Actual Cost Budgeted Cost Inspection costs: Fixed £30,000 £28,500 Variable 20,000 17,500 Fixed inspection costs consist of the salaries of two inspectors, who are paid £14,250. Each inspector is capable of efficiently conducting inspections of 30 batches.

Variable inspection costs consist of materials used during the inspections.

-Refer to Figure 18-3. The volume variance is

(Multiple Choice)

4.9/5 (44)

Figure 18-1

Froelech Company has developed capacity standards. Information is as follows: Standard cost of the activity capacity acquired £150,000 Standard cost of the activity capacity used 100,000 Standard cost of the actual activity used 120,000

-Refer to Figure 18-1. The unused capacity variance is

(Multiple Choice)

4.8/5 (38)

Laune Co.'s standard cost is £200,000, and its allowable deviation is £20,000. Laune's upper and lower control limits are

(Multiple Choice)

4.9/5 (31)

Figure 18-3

Pippen Company's activity-based performance report revealed that actual inspection costs totaled £100,000 at an actual activity level of 50 inspections. Further analysis of inspection costs revealed the following: Actual Cost Budgeted Cost Inspection costs: Fixed £30,000 £28,500 Variable 20,000 17,500 Fixed inspection costs consist of the salaries of two inspectors, who are paid £14,250. Each inspector is capable of efficiently conducting inspections of 30 batches.

Variable inspection costs consist of materials used during the inspections.

-Refer to Figure 18-3. The fixed spending variance is

(Multiple Choice)

4.9/5 (30)

Figure 18-1

Froelech Company has developed capacity standards. Information is as follows: Standard cost of the activity capacity acquired £150,000 Standard cost of the activity capacity used 100,000 Standard cost of the actual activity used 120,000

-Refer to Figure 18-1. The volume variance is

(Multiple Choice)

4.8/5 (25)

Roberts Company uses a standard costing system. The following information pertains to direct materials for the month of July: Standard price per lb. £18.00 Actual purchase price per 1. £16.50 Quantity purchased 3,100. Quantity used 2,950 . Standard quantity allowed for actual output 3,000 . Actual output 1,000 units Roberts Company reports its material price variances at the time of purchase. What is the journal entry to record material purchases?

a.

Materials 55,800 Accounta Payable 55,800

b.

Accesunts Payable 55,800 Materials 55,800

c.

Materials 55,800 Materials price Variance 4,650 Accounta Payable 51,150

d.

Materials 51,150 Materials price Variance 4,650 Accounta Payable 55,800

(Short Answer)

4.7/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)