Exam 4: Complex Financial Instruments

Exam 1: Non-Financial and Current Liabilities91 Questions

Exam 2: Long-Term Financial Liabilities92 Questions

Exam 3: Shareholders Equity161 Questions

Exam 4: Complex Financial Instruments99 Questions

Exam 5: Earnings Per Share73 Questions

Exam 6: Income Taxes74 Questions

Exam 7: Pensions and Other Post-Employment Benefits106 Questions

Exam 8: Leases127 Questions

Exam 9: Accounting Changes and Error Analysis65 Questions

Exam 10: Statement of Cash Flows82 Questions

Exam 11: Other Measurement and Disclosure Issues56 Questions

Select questions type

Use the following information for questions 36-37.

On January 2, 2020, Perseus Corp. issued 10-year convertible bonds at 105. During 2021, all the bonds were converted into common shares having a total value equal to the total face amount of the bonds. At conversion, the market price of Perseus's common shares was 50% above its average carrying value. Perseus adheres to IFRS.

-At issuance, the cash proceeds from the issuance of these bonds should be reported as

(Multiple Choice)

4.9/5  (40)

(40)

*Stock appreciation rights

On January 1, 2020, Hay Ltd. established a share appreciation rights (SAR) plan for its executives. They could receive cash at any time during the next four years equal to the difference between the market price of the common shares and a pre-established price of $ 16 for 180,000 SARs. The market prices are:

Dec 31, 2020-$ 21

Dec 31, 2021-$ 18

Dec 31, 2022-$ 19

Dec 31, 2023-$ 20

On December 31, 2022, 40,000 SARs are exercised, and the remaining SARs are exercised on December 31, 2023.

Instructions

a) Prepare a schedule that shows the amount of compensation expense for each of the four years, starting with 2020.

b) Prepare the journal entry at December 31, 2021 to record compensation expense.

c) Prepare the journal entry at December 31, 2023 to record the exercise of the remaining SARs.

(Essay)

4.8/5 (42)

*Hedging (forward contract)

On May 1, 2020, Bella Corp., a coffee wholesaler, placed an order with its supplier for six tons of coffee, to be delivered and paid for on September 30, 2020. At this time, the spot (current) price for one ton of coffee is $ 3,000, and the future (forward) price for September 30, 2020 delivery is $ 2,900. Thus, Bella decided to enter into a forward contract for six tons of coffee at $ 2,900 per ton for September 30, 2020 delivery. It designated the contract as a cash flow hedge. The contract further calls for a net cash settlement.

Bella's year end is June 30, 2020. At that date the spot price was $ 2,980, the future price for three-month delivery was $ 2,880, and the future price for five-month delivery was $ 2,850.

On September 30, 2020, when the spot price was $ 2,940 and the future price for five-month delivery was $ 2,980, the company took delivery of the coffee, paid its supplier and settled the forward contract.

On October 31, 2020, Bella sold three tons of coffee from this delivery to Java Unlimited for $ 3,400 per ton cash.

Assume all prices are in Canadian dollars (CAD).

Instructions

a) Given the information above, should Bella have hedged this transaction? Why? Would your answer be different if the future price were $ 3,100?

b) Prepare journal entries for the following dates in 2020: May 1, June 30, September 30 and October 31. Bella is a publicly traded corporation and follows IFRS requirements.

(Essay)

4.7/5 (22)

Use the following information for questions 47-49.

On July 2, 2020, Martineau Ltd. issued $ 6,000,000 (par value), 9%, ten-year convertible bonds at 98. The bonds were dated April 1, 2020 with interest payable quarterly on July 1, October 1, January 1 and April 1. If the bonds had NOT been convertible, they would have sold for 96.1. The bond discount is amortized on a straight-line basis. On April 1, 2021, $ 1,200,000 of these bonds were converted into 500 no par common shares. Accrued interest was paid in cash at the time of conversion.

-What is the debit to Interest Expense on Oct 1, 2020?

(Multiple Choice)

4.9/5 (34)

The payment to executives from a performance-type plan is NEVER based on the

(Multiple Choice)

4.9/5 (38)

Johannesburg Corp. has two issues of securities outstanding: no par value common shares and 8% convertible bonds with a par value of $ 8,000,000. Bond interest payment dates are June 30 and December 31. The conversion clause in the bond indenture entitles the bondholders to receive 40 common shares in exchange for each $ 1,000 bond. The value of the equity portion of the bond issue is $ 60,000. On June 30, 2020, the holders of $ 1,200,000 par value bonds exercise the conversion privilege. The market price of the bonds on that date is $ 1,100 per bond and the market price of the common shares is $ 35. The total unamortized bond discount at the date of conversion is $ 500,000. In applying the book value method, what amount should Johannesburg credit to Common Shares as a result of this conversion?

(Multiple Choice)

4.7/5 (40)

*Interest rate swap

On January 1, 2020, Miron Ltd. issues a floating rate bond for $ 500,000. At the same time, the corporation enters into an interest rate swap whereby it agrees to pay interest on $ 500,000 at 10% (the current interest rate) and to receive payments based on the floating rate. At December 31, 2020, the floating interest rate is 8%, and the value of the swap contract is $ 40,000 to the counterparty's benefit.

Instructions

Prepare any journal entries required related to the swap agreement and the interest payment on the bond.

(Essay)

4.8/5 (29)

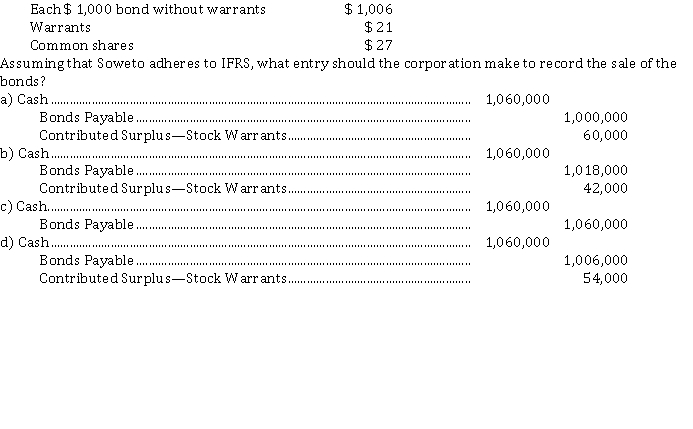

On April 7, 2020, Soweto Corp. sold a $ 1,000,000 (par value), 20 year, 8% bond issue for $ 1,060,000. Each $ 1,000 bond has two detachable warrants. Each warrant permits the purchase one of Soweto's no par value common shares for $ 30. At the time of the sale, Soweto's securities had the following market values:

(Short Answer)

4.8/5 (39)

Use the following information for questions 20-23.

On April 1, 2020, Gamma Corp. purchases a call option for $ 500, which gives Gamma the right to buy 1,000 shares of Delta Inc. for $ 30 each until December 1, 2020. Delta Inc. shares are currently trading for $ 30. At June 30, 2020, the options are trading at $ 4,800 and the shares at $ 32 each. At December 1, 2020, the options expire with no value.

-The intrinsic value of the option at April 1, 2020 is

(Multiple Choice)

4.9/5 (41)

Employee stock options

On November 1, 2018, London Corp. adopted a stock option plan allowing certain of their executives to purchase a total of 30,000 common shares. The options were granted on January 2, 2019, and were exercisable four years after the grant date (Jan 2, 2023), as long as the executives were still employees. The options expire eight years from the grant date. The exercise price was set at $ 46 and, using an option pricing model to value the options, the total compensation expense was estimated to be $ 510,000. At January 2, 2019, the market price of the shares was $ 50.

On January 1, 2020, 3,000 options were terminated (forfeited) when an employee left the company. The market value of the shares at that date was $ 32. All the remaining options were exercised during 2023: 17,000 on January 3 when the market price was $ 62, and 10,000 on May 1 when the market price was $ 77.

Instructions

a) Calculate the intrinsic value and the time value of the stock option.

b) Prepare journal entries relating to the stock option plan for the years 2019 through 2023. Assume that the employees perform services equally from 2019 through 2022. Year end is December 31.

c) Discuss the advantages and disadvantages of offering stock options to employees as a means of compensation.

(Essay)

4.7/5 (29)

Convertible bonds and warrants

For each of the unrelated situations described below, prepare the entries required to record the transactions.

1. On August 1, 2020, Alpha Corporation called its 10% convertible bonds for conversion. The $ 4,000,000 par value bonds were converted into 160,000 no par common shares. On August 1, there was $ 350,000 of unamortized premium applicable to the bonds. At the time of issuance, Contributed Surplus-Conversion Rights was credited for $ 150,000, which represented the equity portion of the convertible bonds, and the market value of the common shares was $ 20 per share. The company records the conversion using the book value method. Ignore all interest payments.

2. Beta Inc. issues 10% convertible bonds, par $ 1,000,000, at 97. The investment banker indicates that if the bonds had not been convertible they would have sold at 94. Use the residual method.

3. Gamma Ltd. issues $ 2,000,000 par value, 8% bonds. To help the sale, detachable stock warrants are issued at the rate of ten warrants for each $ 1,000 bond sold. It is estimated that the value of the bonds without the warrants is $ 1,974,000 and the value of the warrants is $ 126,000. The bonds with the warrants sold at 101. Use the residual method.

(Essay)

4.9/5 (38)

If a SAR is determined to be an equity instrument, it would be valued at

(Multiple Choice)

4.8/5 (34)

Compensation expense resulting from a compensatory stock option plan (CSOP) is generally recognized

(Multiple Choice)

4.9/5 (32)

ASPE requires that high/low (redeemable) preferred shares be presented as

(Multiple Choice)

4.9/5 (41)

In 2019, Algiers Inc. issued 10,000 no par value convertible preferred shares for $ 103 each. One preferred share can be converted into three shares of Algiers' no par value common shares at the option of the shareholder. In August 2020, all of the preferred shares were converted into common shares. The market value of the common shares at the date of the conversion was $ 30 per share. What amount should be credited to Common Shares as a result of this conversion?

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)