Exam 4: Complex Financial Instruments

Exam 1: Non-Financial and Current Liabilities91 Questions

Exam 2: Long-Term Financial Liabilities92 Questions

Exam 3: Shareholders Equity161 Questions

Exam 4: Complex Financial Instruments99 Questions

Exam 5: Earnings Per Share73 Questions

Exam 6: Income Taxes74 Questions

Exam 7: Pensions and Other Post-Employment Benefits106 Questions

Exam 8: Leases127 Questions

Exam 9: Accounting Changes and Error Analysis65 Questions

Exam 10: Statement of Cash Flows82 Questions

Exam 11: Other Measurement and Disclosure Issues56 Questions

Select questions type

At June 30, 2020, Gamma's quarter end, the adjusting entry would be

A) No entry required.

(Short Answer)

4.9/5  (39)

(39)

On July 1, 2020, Juba Inc. issued 10,000, $ 7 non-cumulative, no par value preferred shares for $ 1,050,000. Attached to each share was one detachable warrant, giving the holder the right to purchase one of Juba's no par value common shares for $ 30. At this time, the shares without the warrants would normally sell for $ 1,025,000, while the market price of the warrants was $ 2.50 each. On October 31, 2020, when the market price of the common shares was $ 33.50 and the market value of the warrants was $ 3.00, 4,000 warrants were exercised. Juba adheres to IFRS. As a result of the exercise of the warrants and the issuance of the related common shares, what journal entry would Juba make?

(Short Answer)

4.8/5 (38)

On December 31, 2018, in order to retain certain key executives, Entebbe Corporation granted them stock options. 25,000 options were granted at an option price of $ 40 per share. Market prices of the shares were as follows: December 31, 2019 $ 35 per share

December 31, 2020 $ 39 per share

The options were granted as compensation for services to be rendered over a two-year period beginning January 1, 2019. The Black-Scholes option pricing model determined total compensation expense to be $ 500,000. The amount of compensation expense Entebbe should have recorded for calendar 2020 is

(Multiple Choice)

4.9/5 (45)

Stock options

Prepare the necessary entries from January 1, 2020 to February 1, 2022 for the following events. If no entry is needed, write "No entry necessary."

1. On January 1, 2020, the shareholders of Musetta Inc. adopted a stock option plan for its top executives, where each could receive rights to purchase up to 3,000 common shares at $ 40 per share. At this date, the shares were trading for $ 32 per share.

2. On February 1, 2020, options were granted to five executives to purchase 3,000 shares each. The options were non-transferable and the executive had to remain an employee of the company to exercise the option. The options expire on February 1, 2022. It is assumed that the options were for services performed equally in 2020 and 2021. The Black-Scholes option pricing model determined total compensation expense to be $ 390,000.

3. On February 1, 2022, four executives exercised their options. The fifth executive chose not to exercise her options, which therefore were forfeited.

(Essay)

4.9/5 (33)

For convertible securities, the portion relating to the option should be classified as a(n)

(Multiple Choice)

4.8/5 (41)

Which of the following is NOT a characteristic of a non-compensatory employee stock option plan (ESOP)?

(Multiple Choice)

4.7/5 (40)

Wang Inc. has $ 3,000,000 (par value), 8% convertible bonds outstanding. Each $ 1,000 bond is convertible into thirty no par value common shares. The bonds pay interest on January 31 and July 31. On July 31, 2020, the holders of $ 900,000 worth of bonds exercised the conversion privilege. On that date the market price of the bonds was 105, the market price of the common shares was $ 36, the carrying value of the common shares was $ 18 and the Contributed Surplus-Conversion Rights account balance was $ 450,000. The total unamortized bond premium at the date of conversion was $ 210,000. Using the book value method, Wang should record, as a result of this conversion,

(Multiple Choice)

5.0/5 (45)

Bissau Ltd. issued $ 4,000,000, 5-year, 8% convertible bonds at par. Bonds pay interest annually. Each $ 1,000 bond is convertible to 200 of Bissau's no par value common shares, which are currently trading at $ 25 each. The current market rate for similar non-convertible bonds is 10%. Assuming Bissau adheres to IFRS, the value to be recorded for the conversion option is

(Multiple Choice)

4.9/5 (33)

Use the following information for questions 55-56.

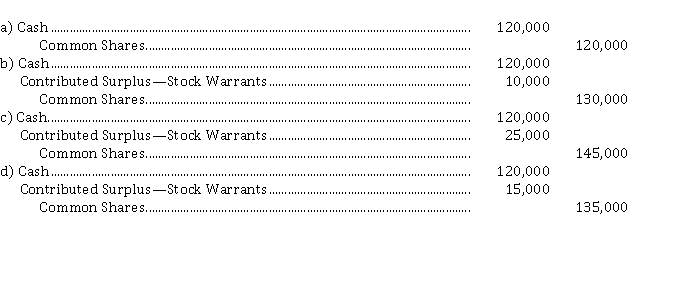

On May 1, 2020, Wong Ltd. issued $ 500,000, 10 year, 7% bonds at 103. Twenty detachable warrants were attached to each $ 1,000 bond, which entitled the holder to purchase one of Wong's no par value common shares for $ 40. At this time, similar bonds without warrants were selling at 96. It was determined that the fair value of Wong's common shares was $ 35, but the value of the warrants was NOT determinable. Wong is a private corporation that follows ASPE, but does NOT use the residual method.

-On May 1, 2020, Wong should credit Contributed Surplus-Stock Warrants for

(Multiple Choice)

4.8/5 (43)

Which of the following would be classified as a hybrid/compound financial instrument resulting in two elements being reported on the SFP?

(Multiple Choice)

4.9/5 (35)

Convertible bonds

On December 1, 2020, Dango Corp. issued $ 5,000,000 (par value), 12%, 5-year convertible bonds for $ 5,026,000 plus accrued interest. The bonds were dated April 1, 2020 with interest payable April 1 and October 1. If the bonds had NOT been convertible, they would have sold for $ 5,006,000. Bond premium/discount is amortized each interest period on a straight-line basis. Dango does NOT value the equity component at zero. Dango's fiscal year end is September 30.

On October 1, 2021, half of these bonds were converted into 35,000 no par common shares. Accrued interest was paid in cash at the time of conversion.

Instructions

a) Prepare the entry to record the interest expense at April 1, 2021. Assume that interest payable was credited when the bonds were issued (round to nearest dollar).

b) Prepare the entry to record the conversion on October 1, 2021. Use the book value method. Assume that the entry to record amortization of the bond premium/discount and interest payment has been made.

(Essay)

4.9/5 (28)

Compensation expense resulting from a performance-type plan is generally

(Multiple Choice)

4.9/5 (35)

Convertible bonds

Lachapelle Drilling Inc., which follows IFRS, offers ten-year, 6% convertible bonds (par $ 1,000). Interest is paid annually on the bonds. Each $ 1,000 bond may be converted into 50 common shares, which are currently trading at $ 17 per share. Similar straight bonds carry an interest rate of 8%. One thousand bonds are issued at 91.

Instructions

a) Assume Lachapelle Drilling Ltd. decides to use the residual method and measures the debt first. Calculate the amount to be allocated to the bond and to the option.

b) Prepare the journal entry at date of issuance of the bonds under IFRS.

c) Assume that after six years, when the carrying amount of the bonds was $ 933,757, the holders of the convertible debt decided to convert their convertible bonds before the bond maturity date. Prepare the journal entry to record the conversion.

d) How many shares were issued at the conversion?

(Essay)

4.9/5 (41)

Use the following information for questions 18-19.

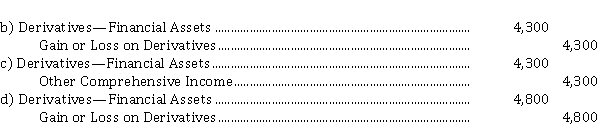

On August 25, 2020, Beta Inc. entered into a forward contract to buy 25,000 Krubles (KRB) for $ 3,800 Canadian (CAD) on September 5, 2020. On August 31, 2020, 25,000 KRB can be purchased for $ 3,500 CAD. On September 5, Beta settles the contract but does NOT take delivery of the KRB.

-On September 5, 2020, the KRB is trading at $ 0.15 CAD. The entry to record the settlement of the contract is

(Short Answer)

4.9/5 (29)

Lagos Inc. issued bonds with detachable warrants for $ 5,000,000 (par value). The bonds have a present value of $ 4,934,400. The fair value of the warrants is determined to be $ 220,000. Using the relative fair value method, how much of the issue price should be allocated to the warrants?

(Multiple Choice)

4.7/5 (41)

Options pricing models

There are numerous options pricing models. Identify the two models discussed in the text and identify and describe what inputs (at a minimum) go into these models.

(Essay)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)