Exam 14: Reporting for Segments and for Interim Financial Periods

Exam 1: Introduction to Business Combinations and the Conceptual Framework35 Questions

Exam 2: Accounting for Business Combinations42 Questions

Exam 3: Consolidated Financial Statements-Date of Acquisition37 Questions

Exam 4: Consolidated Financial Statements After Acquisition42 Questions

Exam 5: Allocation and Depreciation of Differences Between Implied and Book Values36 Questions

Exam 6: Elimination of Unrealized Profit on Intercompany Sales of Inventory35 Questions

Exam 7: Elimination of Unrealized Gains or Losses on Intercompany Sales of Property and Equipment33 Questions

Exam 8: Changes in Ownership Interest32 Questions

Exam 9: Intercompany Bond Holdings and Miscellaneous Topicsconsolidated Financial Statements33 Questions

Exam 10: Insolvencyliquidation and Reorganization34 Questions

Exam 11: International Financial Reporting Standards28 Questions

Exam 12: Accounting for Foreign Currency Transactions and Hedging Foreign Exchange Risk35 Questions

Exam 13: Translation of Financial Statements of Foreign Affiliates29 Questions

Exam 14: Reporting for Segments and for Interim Financial Periods44 Questions

Exam 15: Partnerships: Formation, Operation, and Ownership Changes39 Questions

Exam 16: Partnerships: Formation, Operation, and Ownership Changes35 Questions

Exam 17: Introduction to Fund Accounting29 Questions

Exam 18: Introduction to Accounting for State and Local Governmental Units34 Questions

Exam 19: Accounting for Nongovernment Nonbusiness Organizations: Colleges and Universities, Hospitals and Other Health Care Organizations39 Questions

Select questions type

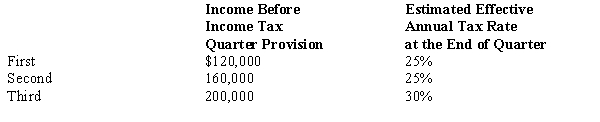

Bjork, a calendar year company, has the following income before income tax provision and estimated effective annual income tax rates for the first three quarters of 2017:  Bjork's income tax provision in its interim income statement for the third quarter should be

Bjork's income tax provision in its interim income statement for the third quarter should be

Free

(Multiple Choice)

4.8/5  (37)

(37)

Correct Answer: Verified

Verified

A

Which of the following is NOT required to be disclosed by SFAS No. 131?

Free

(Multiple Choice)

4.8/5 (33)

Correct Answer:Verified

C

For interim financial reporting, the effective tax rate should reflect:

Free

(Multiple Choice)

4.9/5 (46)

Correct Answer:Verified

B

A component of an enterprise that may earn revenues and incur expenses, and about which management evaluates separate financial information in deciding how to allocate resources and assess performance is a(n):

(Multiple Choice)

4.9/5 (32)

An enterprise determines that it must report segment data in annual reports for the year ended December 31, 2017. Which of the following would NOT be an acceptable way of reporting segment information?

(Multiple Choice)

4.8/5 (32)

Blink Company, which uses the FIFO inventory method, had 508,000 units in inventory at the beginning of the year at a FIFO cost per unit of $20. No purchases were made during the year. Quarterly sales information and end-of-quarter replacement cost figures follow:  The market decline in the first quarter was expected to be nontemporary. Declines in other quarters were expected to be permanent.

Required:

Determine cost of goods sold for the four quarters and verify the amounts by computing cost of goods sold using the lower-of-cost-or-market method applied on an annual basis.

The market decline in the first quarter was expected to be nontemporary. Declines in other quarters were expected to be permanent.

Required:

Determine cost of goods sold for the four quarters and verify the amounts by computing cost of goods sold using the lower-of-cost-or-market method applied on an annual basis.

(Essay)

4.8/5 (43)

The computation of a company's third quarter provision for income taxes should be based upon earnings:

(Multiple Choice)

4.8/5 (33)

Current authoritative pronouncements require the disclosure of segment information when certain criteria are met. Which of the following reflects the type of firm and type of financial statement for which this disclosure is required?

(Multiple Choice)

4.9/5 (40)

In SFAS No. 131, the FASB requires all public companies to report a variety of information for reportable segments. Define a reportable segment and identify the information to be reported for each reportable segment.

(Essay)

4.9/5 (42)

If annual major repairs made in the first quarter and paid for in the second quarter clearly benefit the entire year, when should they be expensed?

(Multiple Choice)

5.0/5 (40)

Which of the following statements most accurately describes interim period tax expense?

(Multiple Choice)

4.8/5 (37)

Inventory losses from market declines that are expected to be temporary:

(Multiple Choice)

4.8/5 (38)

Stein Corporation's operations involve three industry segments, X, Y, and Z. During 2017, the operating profit (loss) of each segment was:  Required:

Determine which of the segments are reportable segments.

Required:

Determine which of the segments are reportable segments.

(Essay)

4.7/5 (40)

An entity is permitted to aggregate operating segments if the segments are similar regarding the:

(Multiple Choice)

4.8/5 (45)

SFAS No. 131 requires the disclosure of information on an enterprise's operations in different industries for:

(Multiple Choice)

4.7/5 (37)

Pale Company has four manufacturing divisions, each of which has been determined to be a reportable segment. Common operating costs are appropriately allocated on the basis of each division's sales in relation to Pale's aggregate sales. Pale's Delta division accounted for 40% of Pale's total sales in 2017. For the year ended December 31, 2017, Delta had sales of $5,000,000 and traceable costs of $3,600,000. In 2017, Pale incurred operating costs of $350,000 that were not directly traceable to any of the divisions. In addition, Pale incurred interest expense of $360,000 in 2017. In reporting supplementary segment information, how much should be shown as Delta's operating profit for 2017?

(Multiple Choice)

4.8/5 (45)

Advertising costs may be accrued or deferred to provide an appropriate expense in each period for:

(Multiple Choice)

4.7/5 (37)

When a company issues interim financial statements, extraordinary items should be:

(Multiple Choice)

4.9/5 (37)

Which of the following reporting practices is permissible for interim financial reporting?

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)